- BNP Paribas Real Estate estimates that the year will close with an investment volume of 9.5 billion Euro

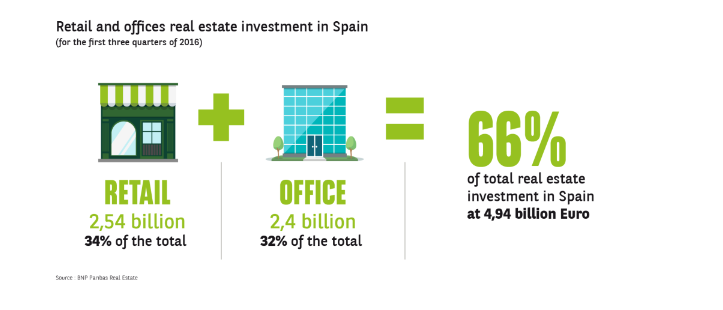

- Retail and offices will corner 66% of investment, at 4.94 billion Euro

- The quarter has closed with a 490 million Euro deal for the Cepsa Tower on the part of Pontegadea

The aggregate real estate investment volume for the first three quarters of 2016 has reached 7.4 billion Euro. Although total investment for the same period in 2015 amounted to 9.3 billion Euro, direct investment in the first nine months of 2016 has reached a volume similar to that of the corresponding period in 2015 (7.09 billion Euro as compared with 7.4 billion for the current year). The volume achieved is particularly noteworthy given the fact that there have been no relevant corporate deals since the beginning of the year.

The current climate in capital markets, with abundant liquidity and low interest rates, is turning the real estate market into an attractive investment option. The foregoing sits within a context in which German bonds are in negative territory and the returns on Spanish bonds are meagre. This is leading to the maintenance of downward pressure on yields.

Retail cornered 2.54 billion and offices 2.4 billion Euro of the market share.

As per last year, the retail sector has garnered the greatest share of total investment (34%) during the year to date, at a figure of 2.54 billion Euro. Given that the main drivers of economic activity are domestic spending and the constant increases in retail sales, it is reasonable for investors to be interested in these types of assets.

Investment in office buildings amounted to 2.4 billion Euro, some 32% of of the total. The office sector has taken second place in terms of interest on the part of investors, drawn to reductions in vacancy rates and the upward trend in rental prices for new contracts.

Investment in the hotel market continues to climb and, during the third quarter of 2016, reached 1 billion Euro. This follows record investment in this sector last year. This trend is based on the improvement on tourism indicators (visits, occupancy, overnight stays, increased expenditure per visitor) and on hotel performance (average daily rate and revenue per available room).

Funds represent the main investors.

Turning to investor profile, with 50% of the total invested the most active players consist of funds. A significant part of these funds are North American, positioning themselves within the retail sector.

The main players during 2015 - the SOCIMIs (Spanish REITs), have slackened off in terms of activity and have been responsible for 13% of the total invested since the beginning of the year. The large acquisitions made in the past will not come onto the market within the short term. Although it is possible that they may dispose of the odd asset, these will not be any of the strategic ones. Although currently in an asset management phase, they will continue to be the main buyers in the coming years. They will however be somewhat more selective due to the lack of product.

The better outlook for the Spanish economy following the third quarter of 2016 and the abundant liquidity in capital markets lead us to believe that the figure for total investment for 2016 will reach 9.5 billion Euro.

- Amira TAHIROVIC