Retail premises in Europe in Q1 2025 : surge in investment and bright consumption outlook

Investors showing renewed interest in retail premises

With investment in commercial real estate on the rise again in Europe, retail premises continue to recover. They showed the strongest growth of all real estate asset categories, with investment up 31% year-on-year, ahead of hotels (+3%), offices (+13%) and logistics (+19%).

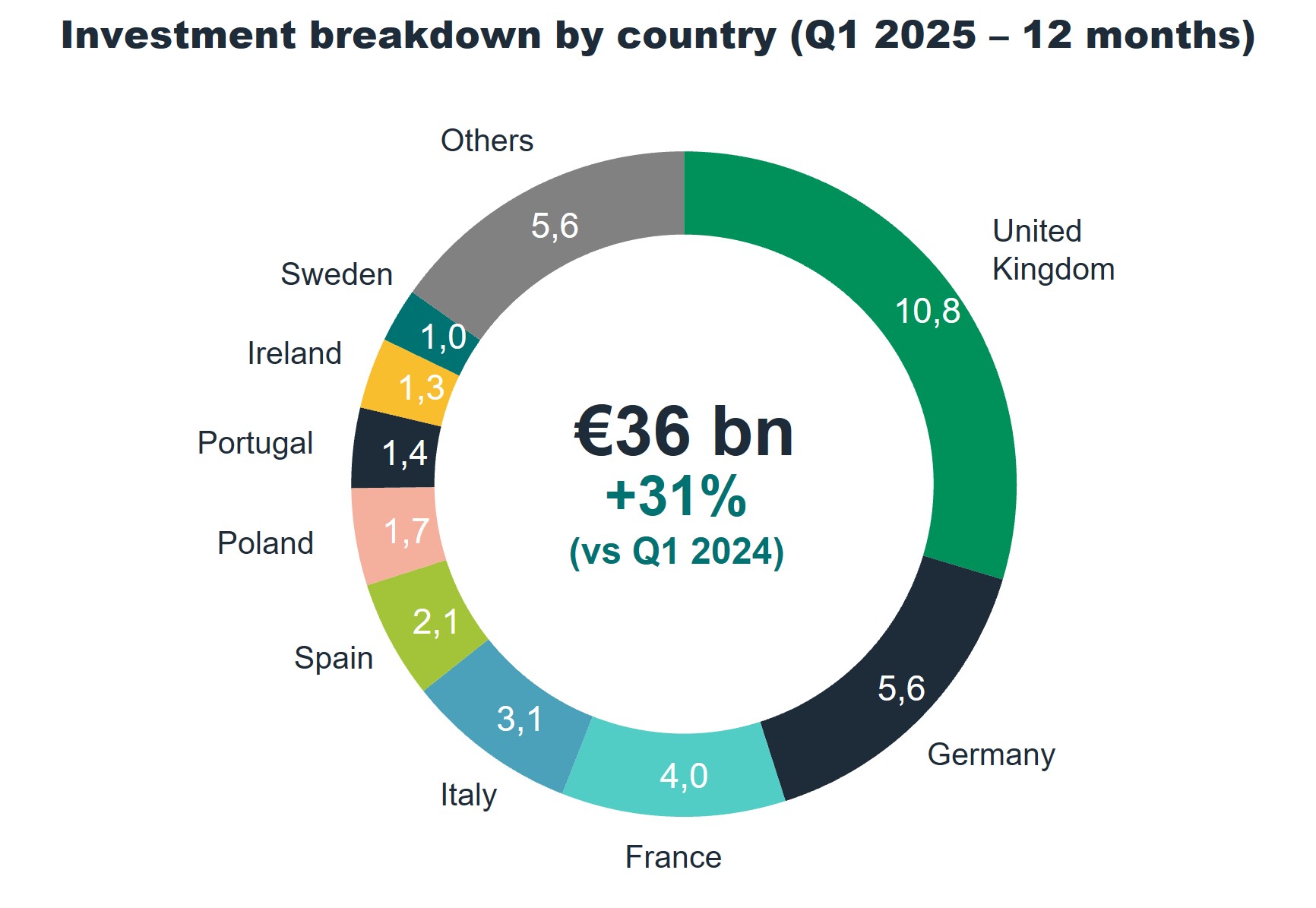

With € 36bn invested over the last 12 months, retail remains in third place in terms of amounts, accounting for 22% of investment (vs. 15% at end 2021 in the depths of the Covid crisis), drawing close to offices (27%) and logistics (26%). Hotels continue to perform well, up 13% (vs. a 10-year average of 8%).

The three largest European markets, i.e. the UK, Germany and France, still account for the lion’s share of investment in retail, but Spain, Italy and Poland also performed strongly, with year-on-year increases of 25%, 311% and 382% respectively.

“Retail’s current healthy trend applied to all segments. As such, investment in out-of-town retail in the main European cities came in at € 10.4bn over the last 12 months, up 12% year-on-year. This segment has the advantage of investment opportunities across a wide range of unit sizes, with lower entry prices than other retail assets. It was also particularly resilient during the Covid crisis and the recent inflationary period”, remarks Patrick Delcol, Head of European Coverage of Retail, Logistics and Hospitality for BNP Paribas Real Estate.

High street deals are also up sharply (+33%) compared with last year, with € 9.4bn invested in the main European countries. Luxury sector contributed significantly to this growth, although this niche market of investor-occupiers is expected to slow somewhat.

Lastly, shopping centres showed the strongest growth (+81%) with € 7.2bn invested over the last 12 months, showing investors’ growing interest in this retail segment. There were some big shopping centre deals in Iberia in Q1 2025, where the asset category has represented 54% of retail investment over the last 12 months.

Appealing risk premium for out-of-town retail and shopping centres

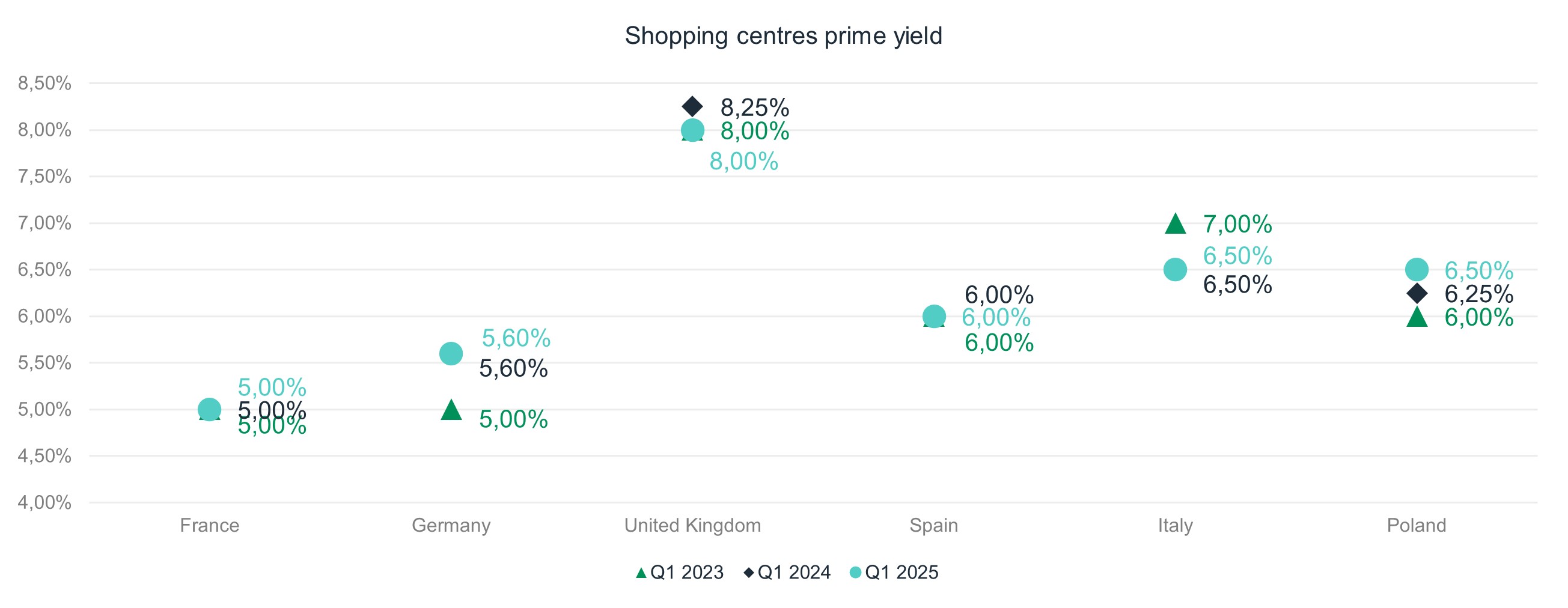

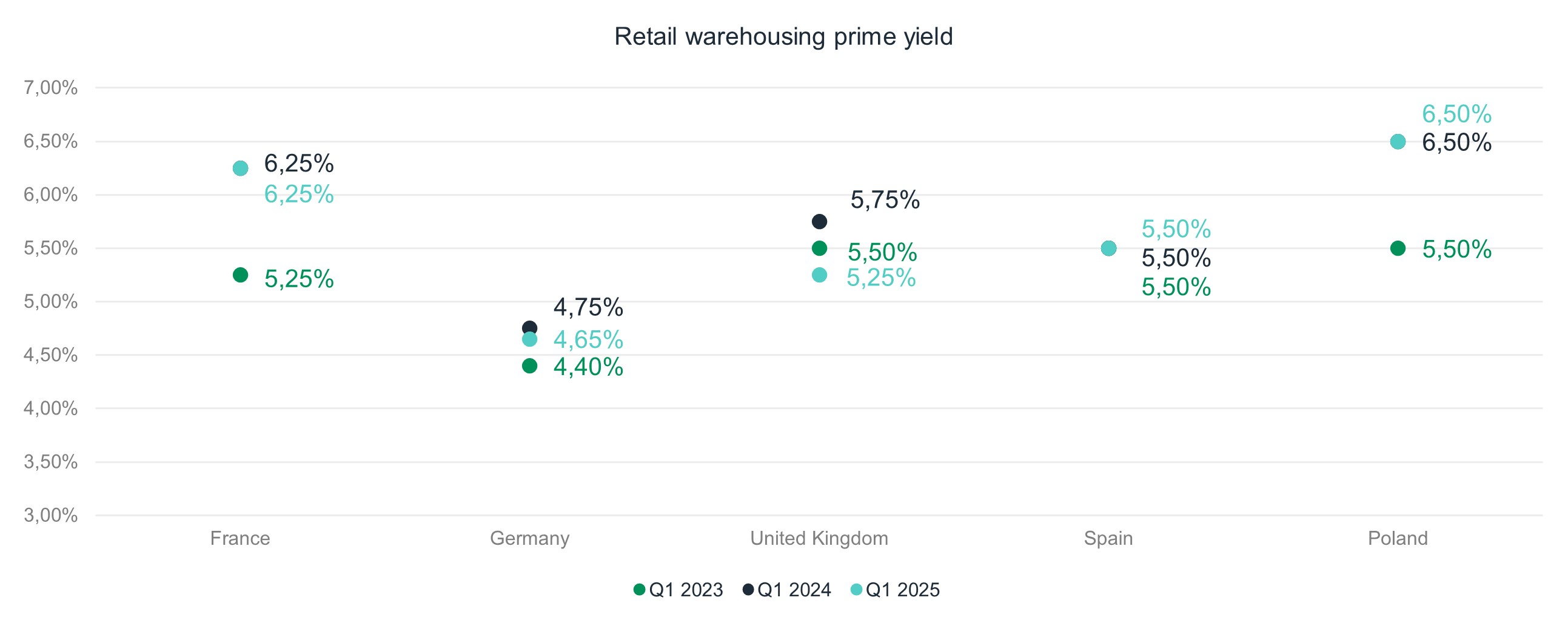

Investors’ renewed interest in out-of-town retail and shopping centres is thanks to the highly appealing risk premiums throughout Europe. These segments have the best risk premium of all real estate asset classes.

Some markets are already seeing year-on-year yield contractions, such as out-of-town retail in Germany (-10 bp) and the UK (-50 bp).

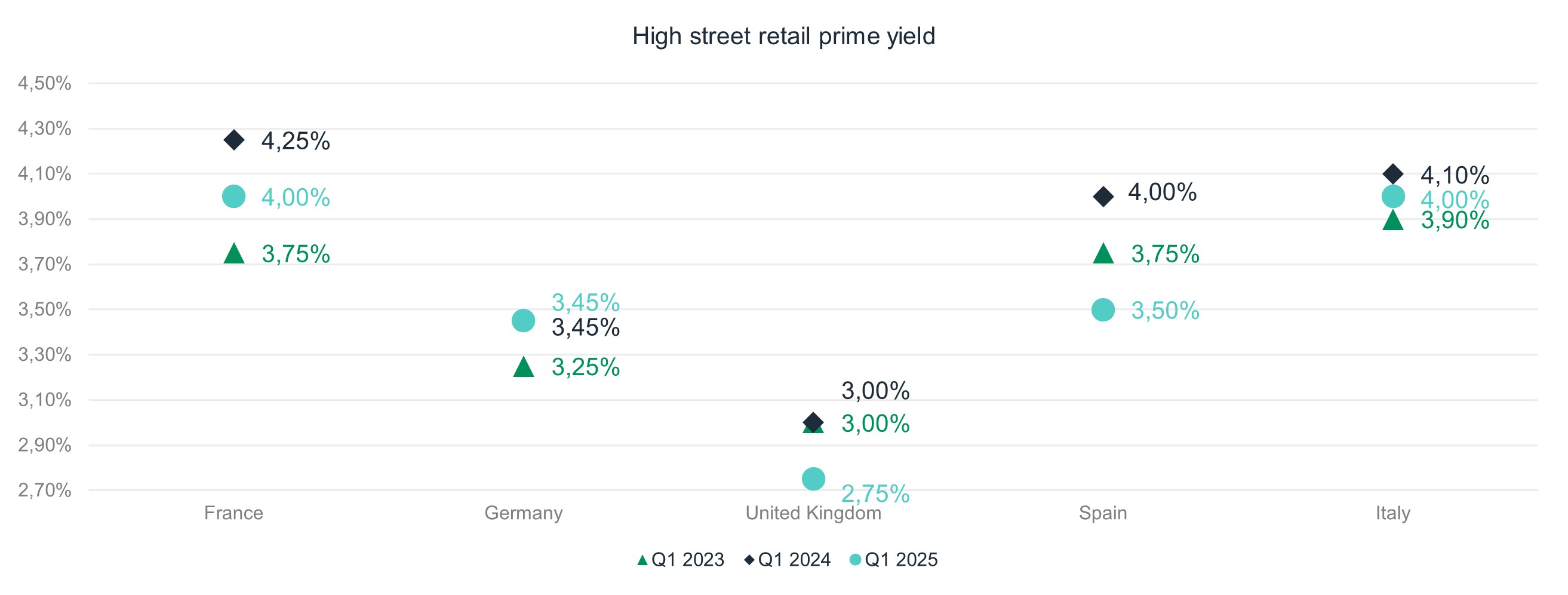

Yields for high street locations showed the first signs of contraction in Q1 2025, particularly in Spain (-50 bp), France (-25 pb) and Italy (-10 pb). These levels are thanks to the transactional trend in the luxury sector but are not reflective of mass-market streets.

Bright outlook for the retail sector

Tourism has been growing for five years. According to the World Tourism Organisation, Europe enjoyed further growth in international arrivals, up an estimated +6% in 2024 compared to 2023. Visitor levels are now higher than they were in 2019, underpinned by a strong Iberian performance and American tourist arrivals in Europe boosted by favourable exchange rates. This is particularly good news for the city centre stores in major European cities. Tourist flows should grow by a further 3% to 5% in 2025 providing further support to retail sales. That said, American consumption may be more moderate in the coming months, held back by the price hikes expected in the US. Moreover, tourist arrivals from Asia, especially China, are likely to continue contracting due to weaker economic growth than forecast. The delayed return of tourists could put a dent in luxury sales.

Retail sales in Europe are also expected to rise by an average of 2% over the next two years, helped by inflation that has now stabilised at just over 2% (2.2% in the eurozone at end April). The confidence of European consumers also recovered in May according to Eurostat thanks to a brighter perception of the overall economic situation. Consumers’ opinions of their future financial situation as well as their purchasing intentions have also improved. There are still some clouds on the horizon that could dampen household confidence and prices, such as the impact of financial market volatility and geopolitical risks.

“The main indicators we track — such as investment volumes, rental trends and economic data — suggest a positive trend. The signs are all pointing towards a gradual recovery, giving us reason to be fairly confident about the outlook for retail in Europe in 2025” concludes Patrick Delcol.

- Amira TAHIROVIC