Although the office sector saw the steepest fall in investment of any asset category in 2023, the market is gradually recovering, underpinned by a consolidation in take-up, a stable vacancy rate and rising prime rents.

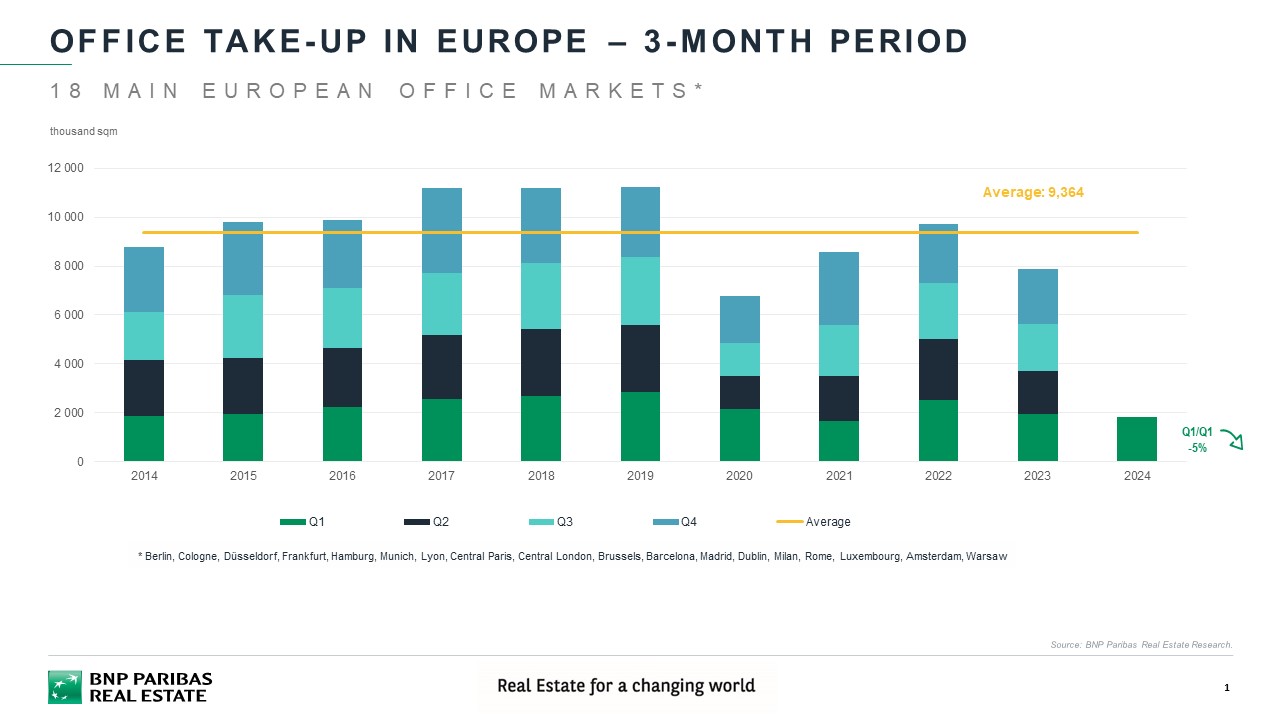

Slow start to the year for letting activity

The slowdown experienced in 2023 has continued into early 2024, with take-up still weak, mainly due to ongoing economic and geopolitical uncertainties. Consequently, volumes for the 18 leading markets* came to 1.82 million sqm at the end of Q1 2024, down 5% vs Q1 2023.

Volumes fell further in several European markets, including Rome (-64%), Dublin (-39%), Amsterdam (-38%), Hamburg (-21%) and London (-17%), in contrast to Barcelona, Frankfurt, Munich, Lyon and Paris, which all saw an upturn in letting activity.

A widespread trend across Europe

The trend remains the same when the analysis is extended to 29 European countries. With total take-up of 2.15 million sqm, the figure was 5% lower than for Q1 2023, with patterns varying greatly in different markets. While take-up fell further in some cities, it has started to climb again in others. Nevertheless, the upturn in letting activity cannot compensate for the downturn: volumes are still below their long-term averages, except in Southern Europe (Barcelona, Madrid and Milan), where stronger economic growth is underpinning the real estate market.

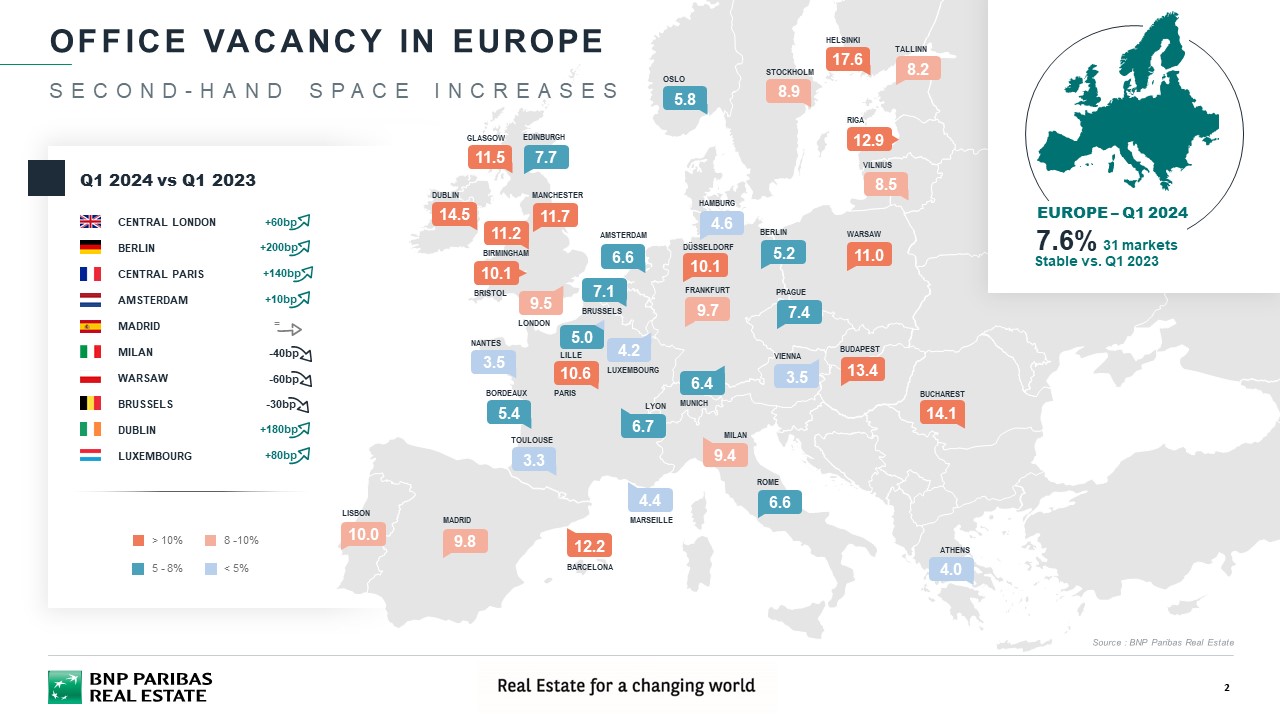

Stable vacancy rate

Compared with Q1 2023, the overall vacancy rate in Europe remains stable at 7.6%. The rise in some markets reflects a growing mismatch between supply and demand, particularly in terms of location. Availability is scarce in central districts, particularly those with modern buildings, while vacancy rates are much higher in the suburbs and for second-hand assets.

The trend varies by market, but Munich, Frankfurt, Paris CBD and Berlin stand out for their significant increases (+100 bp or more), while Milan and Warsaw have seen their rates fall.

Growing gap between prime and standard rents

Occupiers continue to demand recent buildings with low energy consumption and high-quality services, located in sought-after neighbourhoods. Compounded by the lack of these assets, this trend is pushing up prime rents. The greatest increases over the last 12 months have been in Madrid (+12%), Warsaw (11%), Amsterdam (+10%), Paris CBD and Central London (+7%).

Continued growth in prime rents over the last 10 years has resulted in an average increase of 61% since 2013 in the main European markets. The scarcity of supply, particularly in European business districts, is driving fierce competition between occupiers for the best assets, causing prices to soar.

For example, in 2015, the prime rent in Berlin was € 121 higher than the average. Today, the difference is € 206. The same may be said of Frankfurt and Hamburg. In Madrid, over the same period, it rose by 43%. In Barcelona it has increased by 51%, in Milan by 44% and in Rome by 33%. Brussels and Amsterdam have seen increases of +32% and +46% respectively.

In France, Parisian, prime rents have been rising steadily since 2015 (+33%). They are now higher than they were before the crisis (€ 880/sqm/year in 2019). The same goes for Lyon (+12%, € 325/sqm/year in 2019).

To make their buildings more attractive to prospective tenants, landlords of underperforming assets tend to offer incentives rather than a general reduction in rent. These measures are more common and significant for second-hand assets or those located in the suburbs. This trend is likely to spread in Europe over the coming months for the least attractive properties. Consequently, the gap between prime and standard rents is set to widen further.

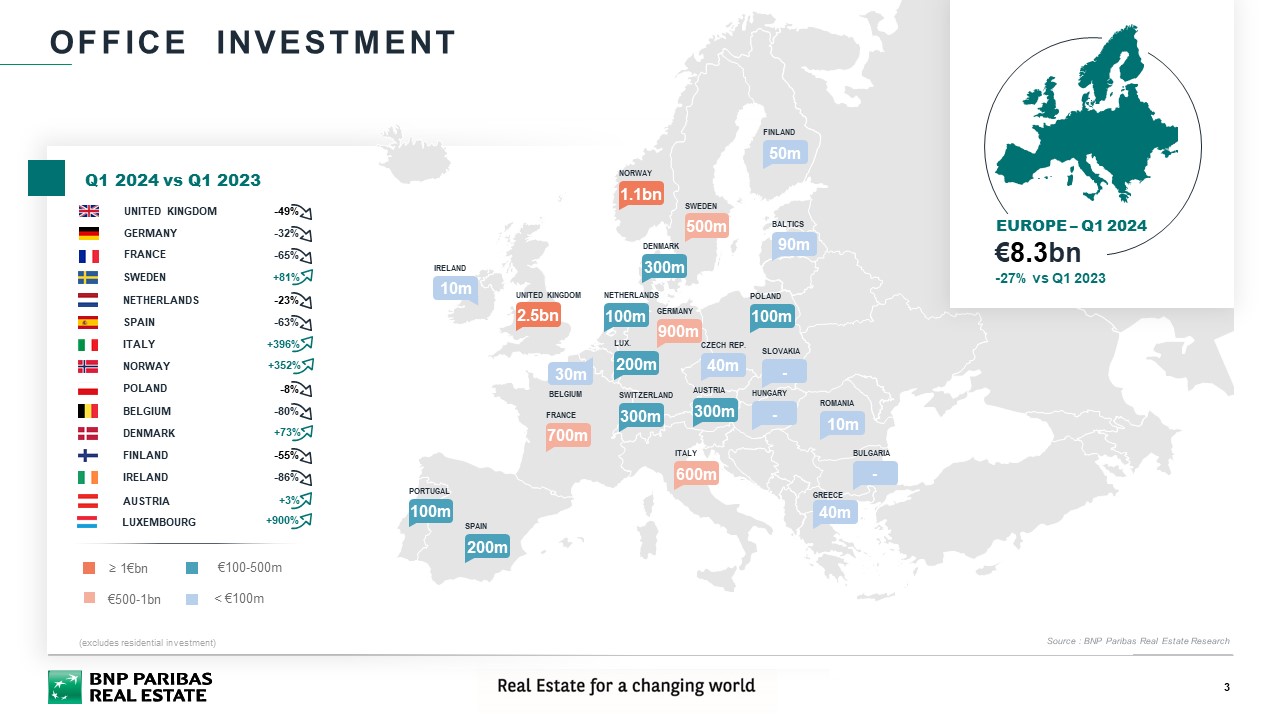

Investment showing first signs of stabilising in Q1 2024

Although investment figures are still lower than in Q1 2023 (-27%), the decline appears to be slowing: on a rolling 12-month basis, the shortfall is only -8% compared with Q4 2023, which is the smallest it has been since the end of 2022.

“Investors are beginning to mobilise with the expectation of falling interest rates and the clear trends of flight to quality by occupiers in prime locations. Investment activity to expected to continue building momentum through this year and into next year. We could be at the start of the next office cycle in Europe which is an optimum time to be investing." observes Argie Taylor, Head of International Investment Group (IIG) de BNP Paribas Real Estate.

Several countries have already recorded positive numbers for Q1 2024, including Luxembourg (+900% vs Q1 2023), Italy (+396%), Norway (+352%), Sweden (+81%) and Denmark (+73%). Other markets are still waiting for a recovery, and have seen further falls in investment, such as Ireland (-86% vs Q1 2023), Belgium (-80%), France (-65%), the UK (-49%) and Germany (-32%).

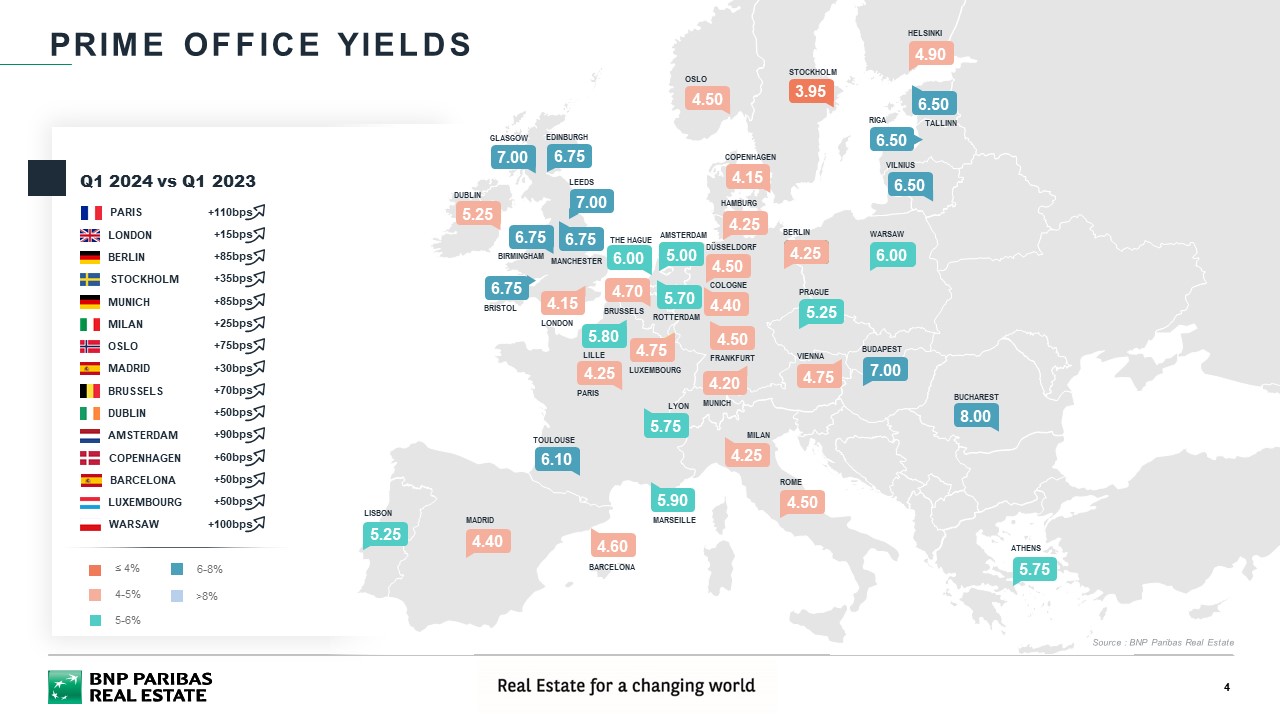

Prime office yields are stabilising

The rise in bond yields following the central banks' tightening policy has put downward pressure on prices since H2 2022, with a knock-on effect for European markets. Prime yields are stabilising for assets located in the central districts of major European cities, such as Paris CBD and London's West End. Indeed, the upward pressure on rents is helping investors to achieve better returns. Conversely, outlying districts with high vacancy rates continued to see yield expansion in Q1 2024.

- Amira TAHIROVIC