Slowing economic growth in Europe and rock-bottom interest rates

Economic growth in Europe has slowed more than expected in 2019, mainly due to the rising trade tensions between the US and China. All told, growth in the Eurozone could come in at around 1.1% in 2019, compared to 1.9% in 2018. “The main feature to watch within Europe will be the geopolitical situation in countries like the UK and Italy. Yet apart from these uncertainties, European growth remains underpinned by solid fundamentals, notably the employment trend, healthy household revenues, strong corporate profits and favourable interest rates”, notes Richard Malle, head of International Research for BNP Paribas Real Estate.

In this uncertain environment, 10-year bond yields have reached new floor levels, dipping below zero in Germany (-0.7%), France (-0.4%) and Netherlands (-0.6%). “Since 2014, economic news, whether good or bad, has driven interest rates down. The risk of a sharp increase in long-term interest rates in the coming years is receding. An inflexion in yields therefore looks unlikely in the medium term for the main European real estate markets”, adds Richard Malle.

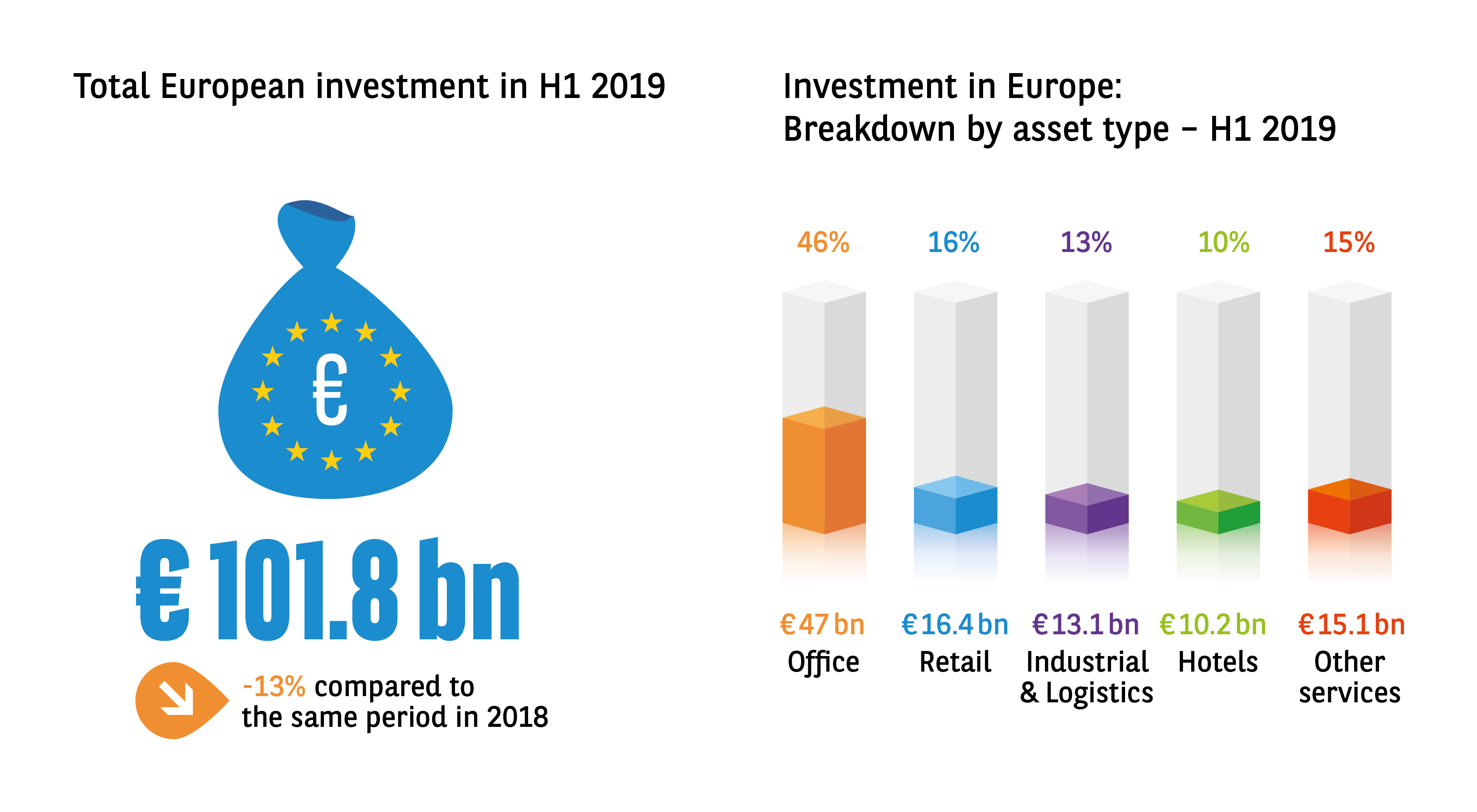

After the record level of 2018, investment in Europe remains high

Investment in commercial real estate in Europe in H1 2019 came in at € 101.8bn, i.e. 13% less than the record level of 2018. The decline applies to all asset categories apart from hotels, which were up 26% to € 10.2bn, close to the 2015 record (€ 10.7bn). This was thanks to several major deals including portfolios in Italy, France and the Czech Republic in particular. The office segment (€ 47bn) slipped just 6% thanks to two transactions of over € 1bn in Paris and numerous huge deals in the leading German markets. Logistics fell 16% with investment of € 13.1bn; which remains 30% above the long-term average. The retail segment saw the biggest decline (-31%) with investment of € 16.4bn, well below the long-term average, suggesting dwindling enthusiasm among investors for this asset category.

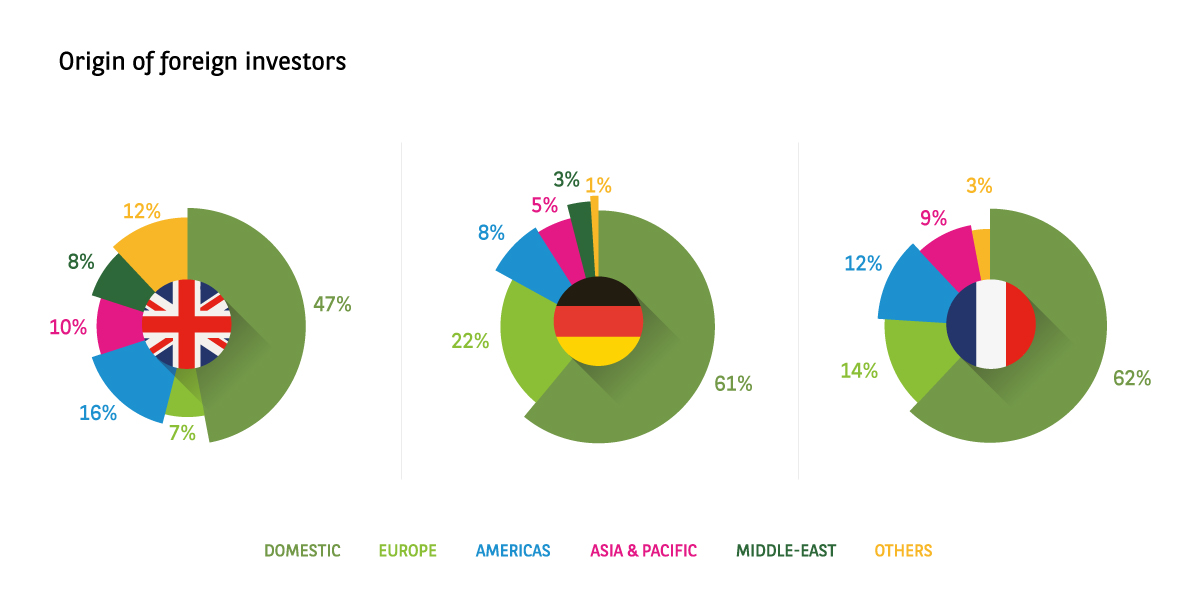

With investment of € 24.4bn, Germany (-6%) ranked first among European countries. Despite the slight fall, investment in the country was in line with the five-year average. In the biggest cities (apart from Berlin which saw record figures), the fall was due to a lack of assets rather than weaker demand. Usually in pole position, the UK was in second place with investment of € 22.1bn, a steep fall compared to H1 2018 (-33%), but also well below the long-term average. Amid the uncertainty of Brexit, many investors have put their strategies on hold until the situation becomes clearer. After the record figure of € 34bn in 2018, France started 2019 with the same impetus (+0%) with € 13.7bn invested. The market was driven by offices, which accounted for 70% of the total. Most other European countries enjoyed an upward trend, such as Belgium (+105%), Italy (+96%), Spain (+88%), Poland (+57%) the Czech Republic (+31%) and Ireland (+6%). Only Holland (-55%), Luxembourg (-22%) and Romania (-65%) saw a decline.

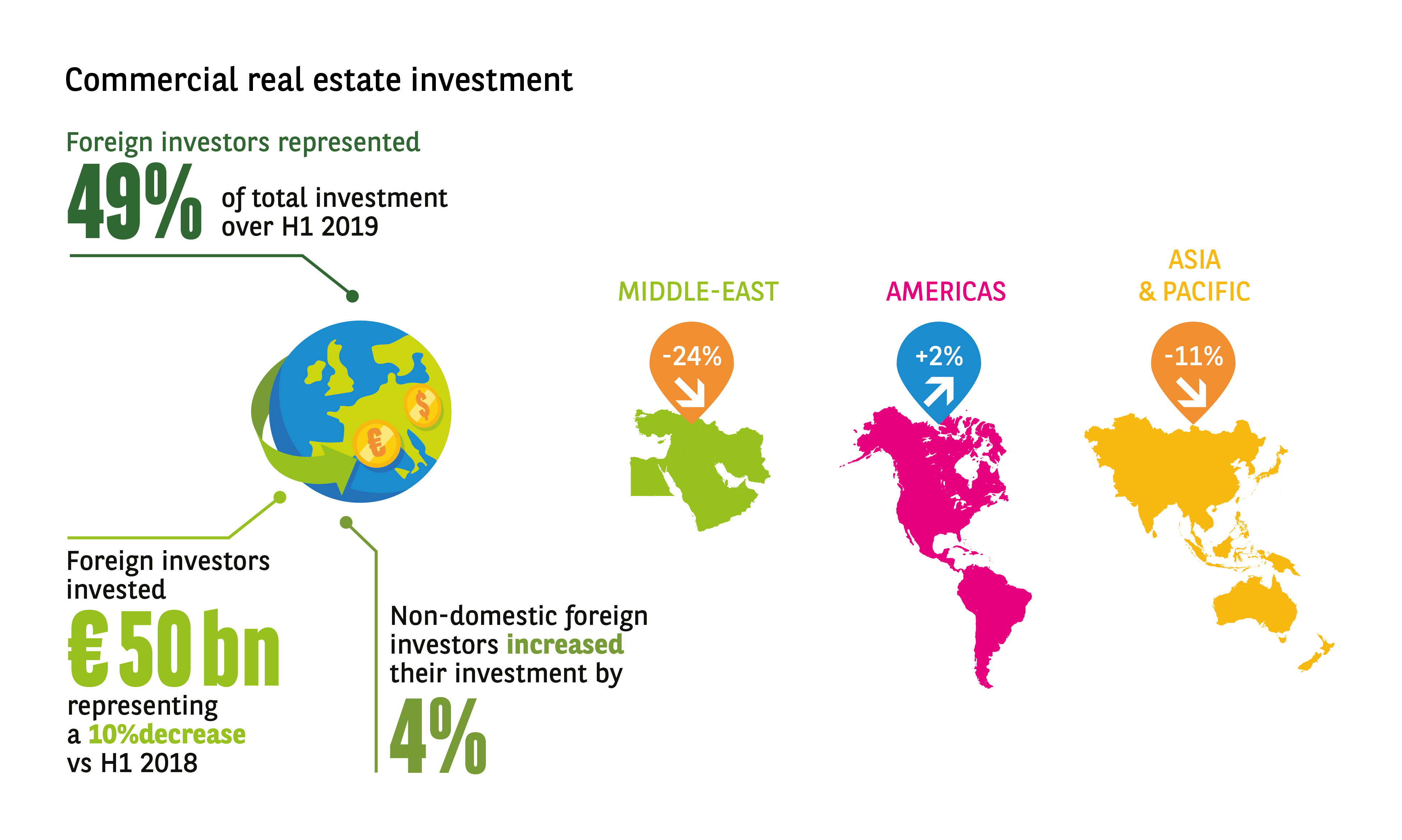

Slowdown for foreign investment in European commercial real estate

In H1 2019, foreign investment in the European commercial real estate market fell by 10% compared to the year-earlier period. “European investors stood out once again, even seeing an increase in their market share since the beginning of the year (45%). US investors, after a peak in activity followed by a withdrawal from the market in 2016, have since been oscillating around € 25bn annually. They invested commensurately in early 2019. Asian investors were less keen (-11%) but have clearly established their presence in Europe in recent years. Middle Eastern investors have been less present in 2019 (-24%) with investment coming in well below the long-term average”. said Larry Young, head of the group’s International Investment division.

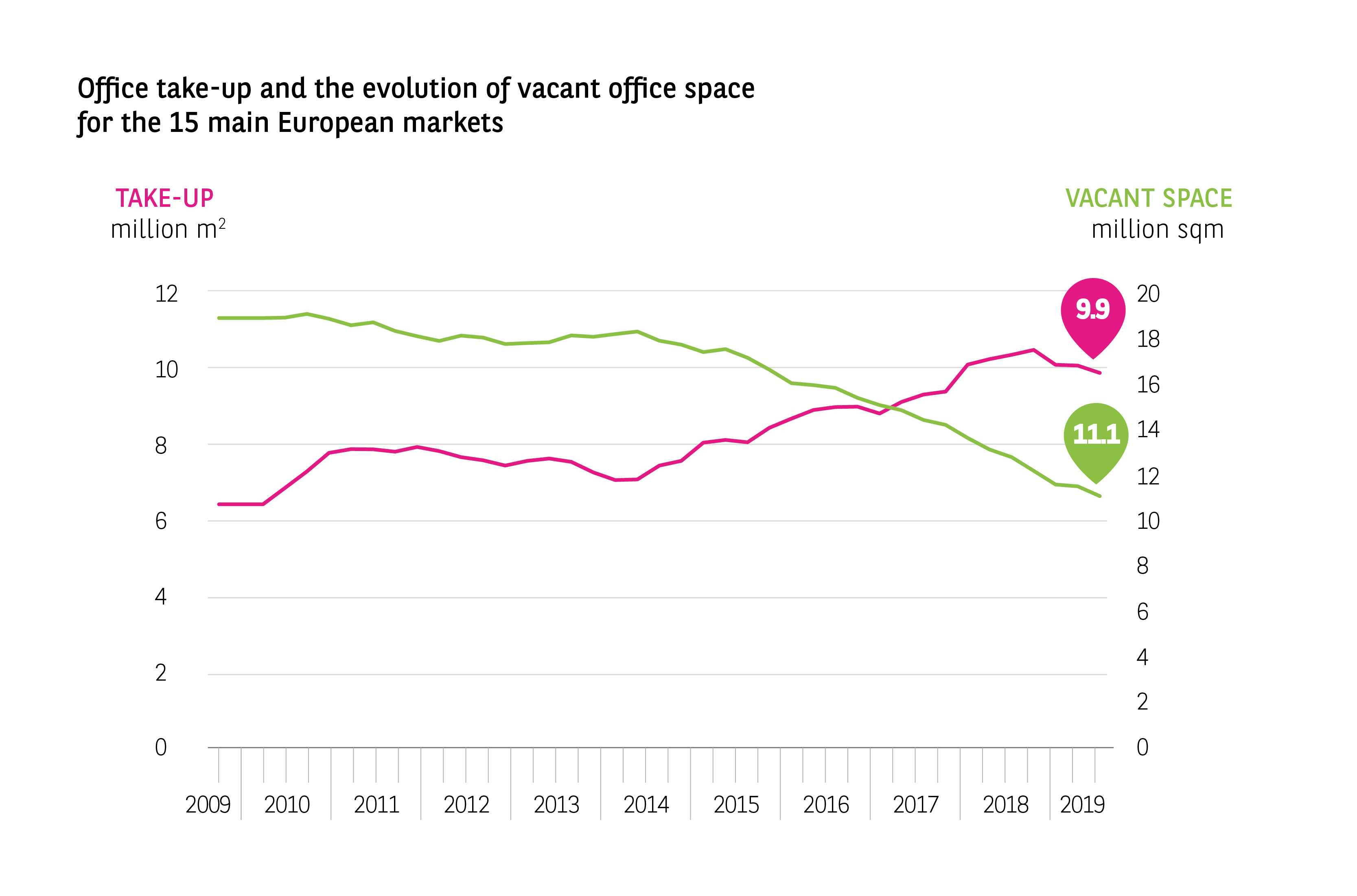

Demand for offices remains high in the 15 main European markets

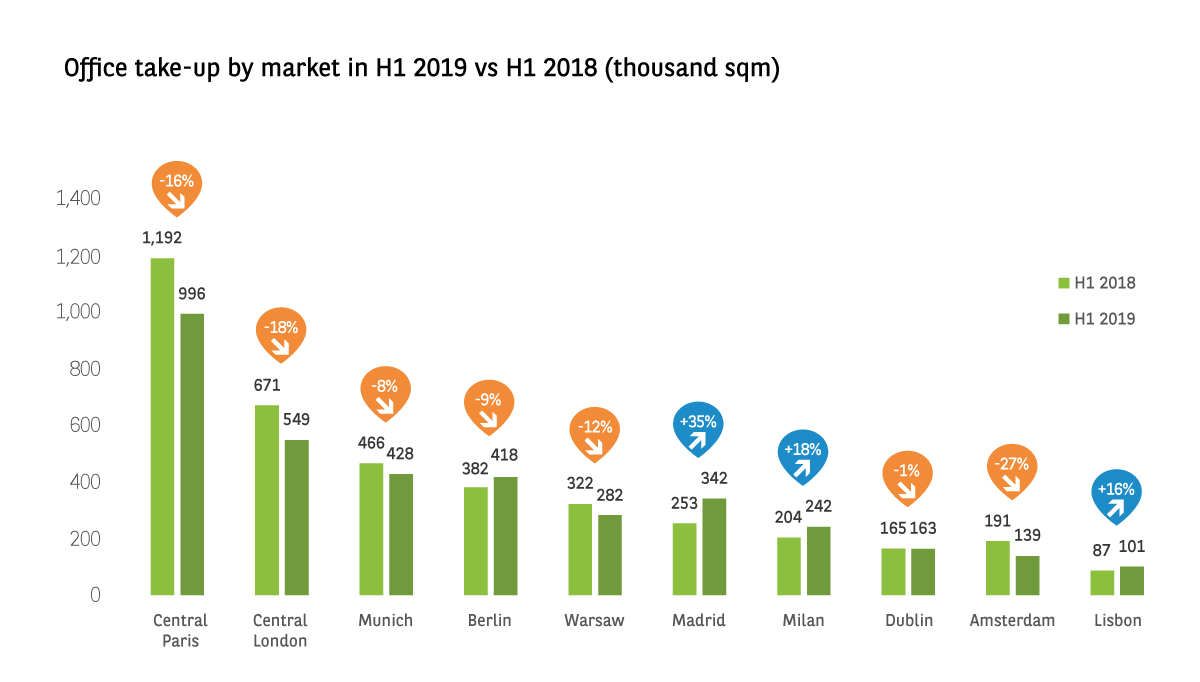

Take-up in the leading 15 European office markets remained very high in H1 2019, with 4.75 million m² changing hands over the first 6 months of the year. Despite a 2% fall vs. 2018, the figure for H1 was at its second highest in 10 years. Yet the overall figure conceals major disparities, with some markets showing a distinct slowdown while others continue to break records.

As such, Warsaw (-12%), Central Paris” (-16%), Central London (-18%) and Amsterdam (-27%) dipped, but remain in line with their long-term averages. The outlook for the rest of the year is still bright for Paris, with several major transactions expected in H2, while London is faring better than expected even though the Brexit deadline set by the EU is looming.

The four main German markets meanwhile appear to be unaffected by the slowdown in France, with Berlin and Hamburg breaking their all-time records. Records were also beaten in Brussels, with investment more than doubling vs. 2018 (+125%), as well as Milan (+18%) and Madrid (best H1 performance since 2007, up 35% over a year).

Aymeric Le Roux, the executive head of International Advisory & Alliances, says: “Thanks to a healthy take-up trend for several years now, European office markets currently boast very low vacancy rates. This means that immediate supply is historically low in most major European cities and competition between occupiers for high-quality assets in the main business districts is as fierce as ever. Prime rents naturally reflect this trend and remain high throughout Europe”. Consequently, the vacancy rate in Europe has contracted further, standing at 6.2% on average, with the lowest rates in Berlin (1.7%) and Munich (2.2%). The biggest falls in the vacancy rate have been in Warsaw (-260bp), Lisbon (-210bp) and Amsterdam (-190bp). Prime rents have meanwhile remained stable or increased in all the main European markets, apart from Central London (-2 % vs. H1 2018) where they stand at £ 1,211/m²/yr. Hamburg (+11%, € 360/m²/yr) meanwhile enjoyed the strongest rental growth. The other substantial increases were in Warsaw, Berlin (+9%) and Milan (+5%).

- Amira TAHIROVIC