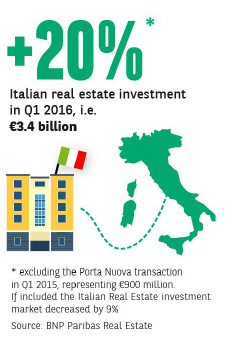

The Italian real estate market is continuing to benefit from strong momentum. Despite significant volatility factors, H1 2016 performance benefitted from the completion of a number of transactions initiated in H2 2015. Excluding the non-typical sale of Porta Nuova, concluded in Q1 2015 for €900 million, investment volume between January and June 2016 on the Italian peninsula increased 20% to €3.4 billion. There is high polarisation between core investors, with very low returns, and opportunistic and distressed funds, which aim to close transactions to widen the gap between the bid and ask prices. Market growth will depend on whether the market can open up to new types of investors whose target unlevered internal rate of return is between 8% and 12%.

The Italian real estate market is continuing to benefit from strong momentum. Despite significant volatility factors, H1 2016 performance benefitted from the completion of a number of transactions initiated in H2 2015. Excluding the non-typical sale of Porta Nuova, concluded in Q1 2015 for €900 million, investment volume between January and June 2016 on the Italian peninsula increased 20% to €3.4 billion. There is high polarisation between core investors, with very low returns, and opportunistic and distressed funds, which aim to close transactions to widen the gap between the bid and ask prices. Market growth will depend on whether the market can open up to new types of investors whose target unlevered internal rate of return is between 8% and 12%.

At the start of the year, large transactions—such as the sale of the Great Beauty portfolio in Rome and the building on via Monte Napoleone in Milan—helped support investor activity. These are prime examples of the type of deals undertaken by core investors in high-quality products located in the historic centre of the two largest cities in Italy.

In addition to prestigious assets, the market saw some transactions concerning core products that were not located in historic centres but that attracted investors' attention thanks to the quality of the tenants. The real estate arm of Banque de Montreal acquired the Coin building on Rome's via Cola di Rienzo with an aggressive yield. In Milan, Vodafone Village on via Lorenteggio and L'Oréal's Italian headquarters on via Primaticcio changed hands.

"Investors find themselves in an environment of negative interest rates, which is pushing returns down to historic lows. There are, however, several uncertainties which may affect the market over the next few months, such as the restructuring of the banking system, the referendum on the Italian constitution and, more generally, the development of the geopolitical context," says Simone Roberti, Director of Research at BNP Paribas Real Estate in Italy.

The diversity of risk profiles for investors interested in Italian real estate is reflected in the diversity of investments currently being made on the market. In addition to conventional office real estate, these include asset classes such as town-centre shop premises and sectors such as hospitality (especially in Rome) and logistics. Investment in hospitality and logistics attracted greater interest from investors compared with H1 2015.

Transactions for hospitality sector premises rose 18% in value versus H1 2015, and logistics saw a 122% increase. The office segment also entered a prosperous period, as it continued to attract investors and accounted for 55% of total transaction volume, up 58% year-on-year. It was a different story, though, for the commercial real estate sector, which saw a 23% drop in transaction volume during the first half of the year.

Transactions for hospitality sector premises rose 18% in value versus H1 2015, and logistics saw a 122% increase. The office segment also entered a prosperous period, as it continued to attract investors and accounted for 55% of total transaction volume, up 58% year-on-year. It was a different story, though, for the commercial real estate sector, which saw a 23% drop in transaction volume during the first half of the year.

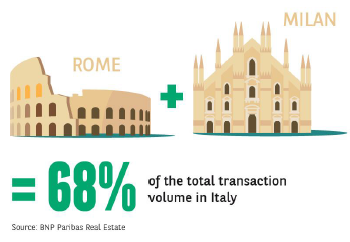

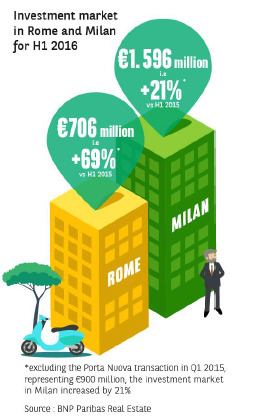

Milan and Rome—the two main markets—accounted for 68% of the transaction volume in Italy during the period. A number of large deals carried out during the first six months of the year helped the investment market in Rome achieve a transaction volume of €706 million, up 69% year-on-year. But total investments in Rome represented just 44% of those in Milan.

Milan and Rome—the two main markets—accounted for 68% of the transaction volume in Italy during the period. A number of large deals carried out during the first six months of the year helped the investment market in Rome achieve a transaction volume of €706 million, up 69% year-on-year. But total investments in Rome represented just 44% of those in Milan.

Rome

The sound level of investment in 2015 was thanks to the return of certain large transactions to the capital city. However, apart from a few large deals which could give the impression of a lively market, the real estate market in Rome remains fairly sluggish with relatively small transactions. On the one hand, private companies are unable to find the product that suits their needs and prefer to remain in their current offices. On the other hand, the public sector remains relatively inactive in terms of its policy concerning reorganisation and the construction of efficient, modern office space (such as SDO and Campidoglio 2), which would free up valuable space in the historic centre of the city for reclassification or conversion. With the market picking up, investors are also assessing the transformation and conversion of vacant office buildings in the business quarter into hotels or shops. This type of operation will not be possible for the buildings on the outskirts (with these buildings representing a large proportion of the total offer), as they are in poor locations and do not provide sufficient repositioning potential.

The sale of part of the Scarpellini portfolio, two buildings in the historic centre which will be repositioned after undergoing significant reclassification work, falls into this category.. This is a typical example of exactly what the market in Rome needs, namely collaboration between investors with the aim of creating new, high-quality products.

The sale of part of the Scarpellini portfolio, two buildings in the historic centre which will be repositioned after undergoing significant reclassification work, falls into this category.. This is a typical example of exactly what the market in Rome needs, namely collaboration between investors with the aim of creating new, high-quality products.

MILAN

Following a prosperous period, Milan's office market experienced a slightly less dynamic first quarter, but this remains in line with the average for the sector in the long term. This slowdown is not a cause for concern as the potential demand remains high.

In fact, during Q2 2016 certain significant transactions increased the demand to 100,000 sq. m, with a total of 151,000 sq. m in H1, i.e. an 18% increase in comparison to the same period in 2015. The volume of vacant office space has stabilised. The space sold does not appear to have been the most adapted to the requirements of the demand and a restructuring and rehabilitation process was put in place in order to recapture the interest of investors. As a result, prime rents have remained stable in H1 although we have started to notice upward pressure on prices in both business districts. In fact, the Porta Nuova quarter is currently the only balanced submarket in Milan, with a progressively declining offer.

- Amira TAHIROVIC