According to BNP Paribas, growth assumptions for the economy remain at a high level in 2018, even if a slowdown should appear in the Euro area.

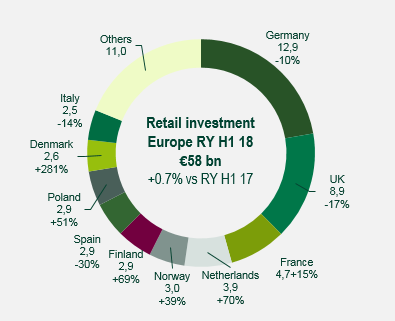

- Retail investment, the 2nd largest sector (€58 bn) remained stable over the last 12 months

- Lower volumes were recorded in Germany and in the UK while retail investment in France was up

- Retail prime yields are under pressure in most European markets

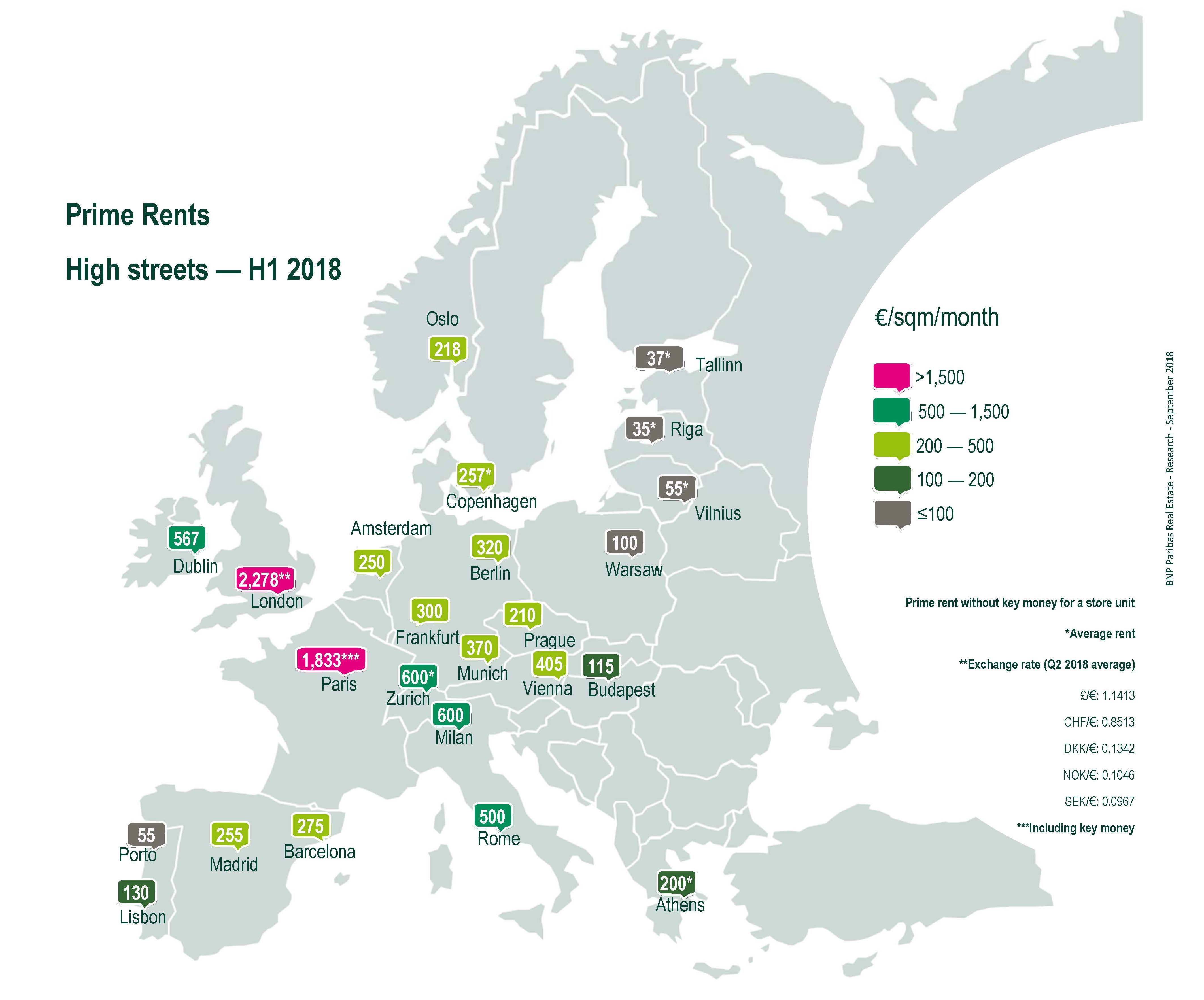

- In H1 2018, London’s Old Bond Street followed by Paris’s Avenue des Champs Elysées have kept their top position as the two most expensive store locations

European retail trade still increasing

In the Eurozone, retail trade will stand at +1.7% in 2018 and should reach +2.1% in 2019. In the major markets, compared to 2017 weaker growth is expected for this year: Germany +1.2% (vs 3.0% in 2017), France +2.8% (vs 3.0%) and the UK +1.7% (vs +2.1%), in domestic currency and at constant exchange rates. As observed over the last few years, thanks to dynamic economy, retail sales growth in CEE countries remain strong in 2018: Poland (+6.0%), Czech Republic (+5.3%).

Patrick Delcol, Head of Pan-European Retail, said: “Retail is facing structural changes. Physical stores stay under pressure from the online players and consumers’ expectations adjusted to their store experience to the new omni-channeling shopping habits.” European online sales are still increasing (+13.6% in 2017, source: E-commerce Foundation), but at a lower pace compared to 2016 (+15.4%) and previous years. Internet penetration is growing at a faster pace than average in Southern and Eastern countries.

European retail investment remains stable in H1 2018

Retail investment volume

Europe – Rolling year – H1 2018

Retail investment, the 2nd largest sector (€58 bn) after offices remained stable over the last 12 months. On half-year, even though its share of total investment slightly declined (22% vs 23% in H1 17), retail property volumes remained higher than the 10-year average. Among the major markets, in H1 18, lower investment in Germany (-16%), can be linked to an inadequate supply of larger portfolios. Decreasing volume was also recorded in the UK (-10%), but especially in Q1 18. Several large transactions have occurred in Q2 18. Retail property investments were up in France (+57%) mainly thanks to the Apple Store transaction on the Champs Élysées. Portfolio retail deals boosted the Polish market. In Italy, big deals brought H1 2018 in line with results registered in 2017, a record year. In Spain, retail assets still represent the major part of total investment (42%).

Retail prime yields have been under pressure in most European markets. In Paris, the prime high street yield fell to 2.50%. Prime shopping centre yields were stable in major countries except in the UK where they have been increasing over the last few quarters.

Occupier Market: prime rents in luxury high streets remain high

Patrick Delcol, Head of Pan-European Retail, said: “Prime rents in the luxury high street segment remain high. In H1 2018, London’s Old Bond Street followed by Paris’s Avenue des Champs Elysées kept their top positions from that perspective”.

Because of a lack of available products, rents in Milan are increasing especially in via Montenapoleone (€600/sqm/month, +20% vs H1 17). Other places such as Prague’s Pařížská (€210/sqm/ month, stable vs H1 17) continue to attract prestigious brands (Furla, Elisabetta Franchi) as first stores in the Czech Republic. End of 2018, Cartier is due to enter the Nordics market through a store located in Stockholm’s Smålandsgatan.

In mixed streets such as Madrid’s Calle Serrano (€248/sqm/ month, +3% vs H1 17), Bottega Venetta, Yves Saint Laurent and Maisons du Monde opened stores last spring.

In the mass-market segment, Kalverstraat’s Amsterdam (€250/sqm/month, stable vs H1 17) is a sought-after high street location for international retailers. After Under Armour opened at the end of 2017, Uniqlo is set to enter the Dutch market in autumn.

Click here to download the full report

- Amira TAHIROVIC