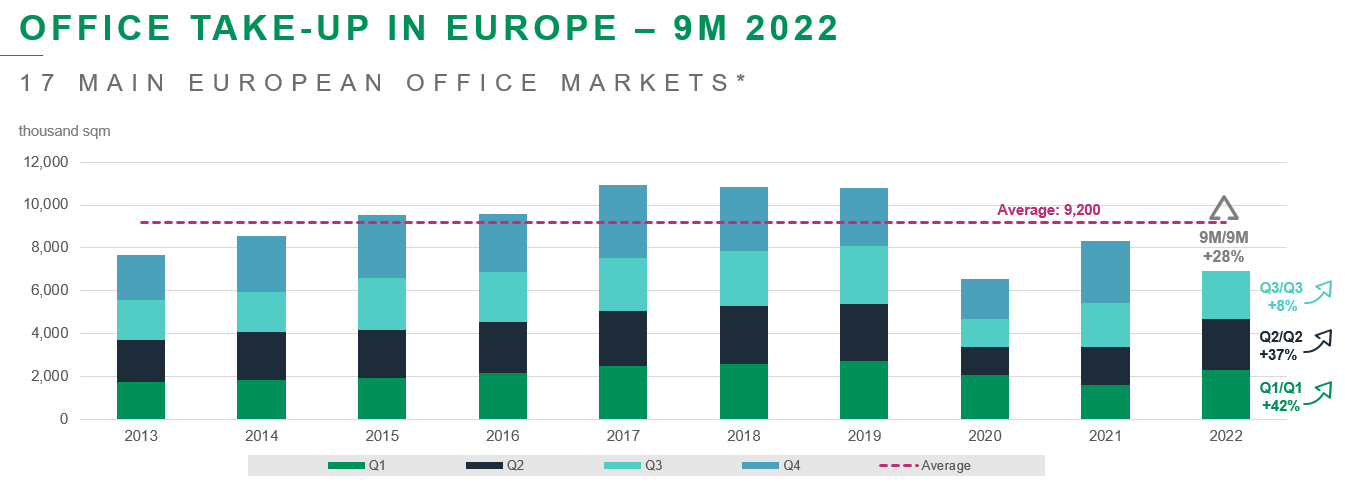

Significant increase in office take-up in 2022

Following a very encouraging end to 2021, the recovery of European office markets was confirmed in 2022, driven by the quest for high-quality, flexible spaces, better suited to new hybrid working styles. Take-up in the 17 main markets* came in at 6.924 million sqm after 9 months, up by some 30% vs the same period in 2021, largely thanks to a particularly buoyant H1.

Take-up to end September 2022 back to historical levels

Take-up across 25 European cities was up +29% to end September 2022 compared to the year-earlier period. The growth was such that take-up matched or even exceeded its long-term average in many markets.

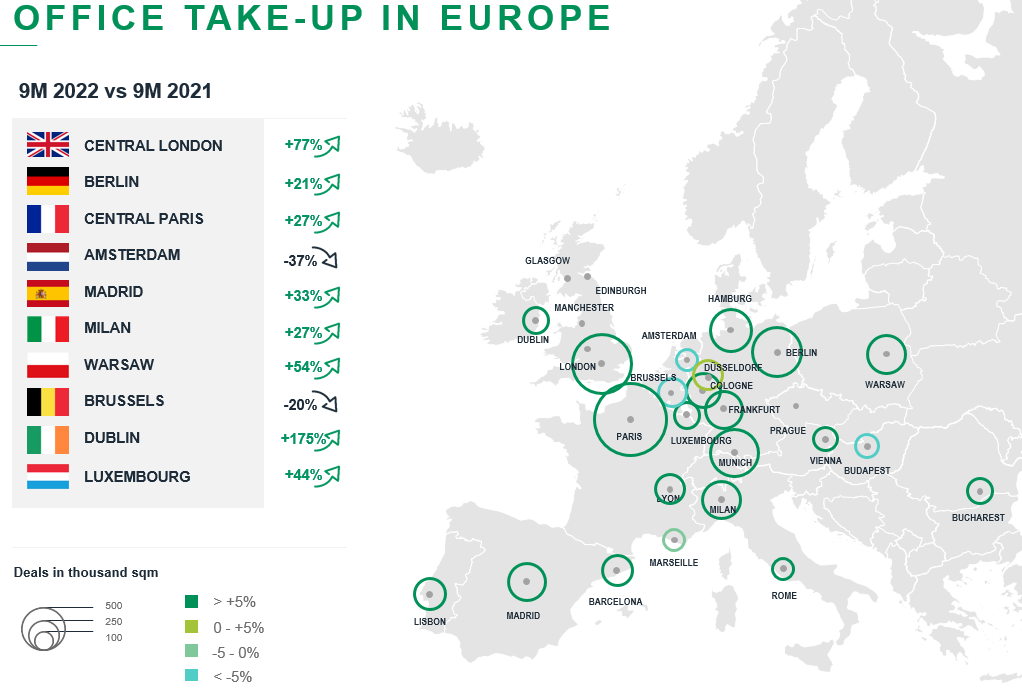

The recovery in rental activity was particularly noticeable in Dublin (+175% vs 9M 2021), Central London (+77%), Warsaw (+54%), Luxembourg (+44%) and in the six main German markets (+22%).

“2022 should end on this positive momentum and annual volumes should be in line with their long-term average in most European markets”, says Laurent Boucher, President of BNP Paribas Real Estate Advisory.

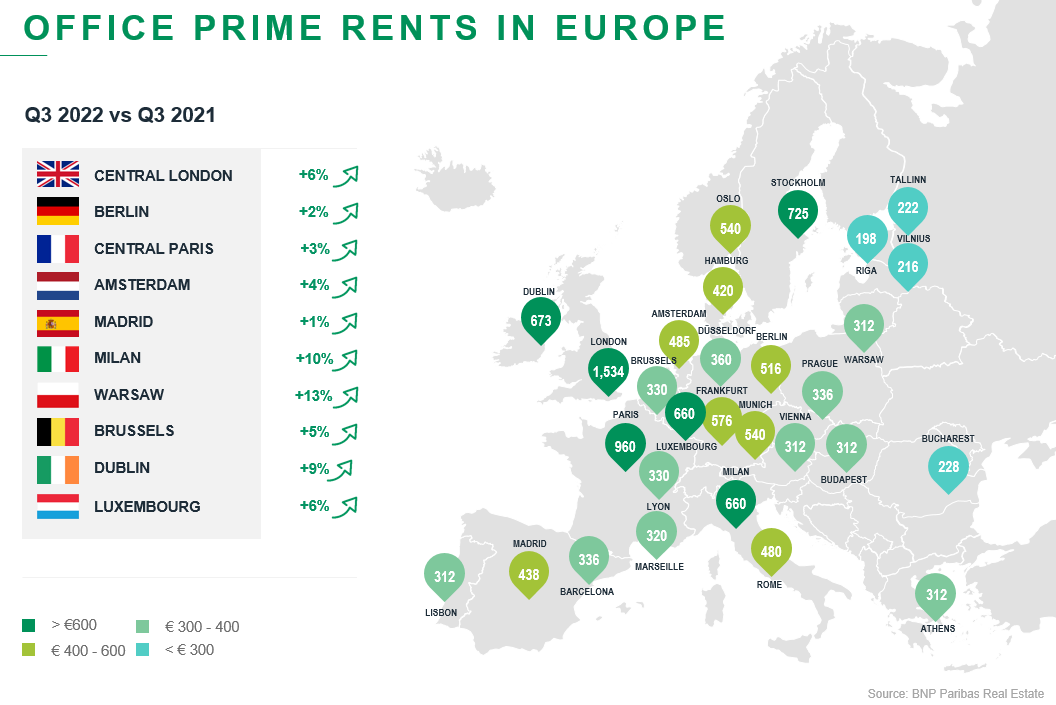

Prime rents continue to climb with the desire for central, high-quality locations

Alongside the spread of teleworking, the office is reasserting itself as a vital destination, strengthening its role as a catalyst for integration, collaboration and setting a collective example. It has become a competitive advantage in recruiting and retaining talent.

This is reflected in the growing popularity among occupiers of central locations, fuelling the growth of prime rents in almost all markets.

The biggest increases over the past 12 months have been in Warsaw (+13%), Milan (+10%) and Dublin (+9%).

However, there seems to be a widening gap between new assets in the most sought-after districts, where rents are rising steadily, and those in secondary areas, which are likely to fall out of favour with occupiers.

Vacancy rates still under control

After rising sharply over 2020 and early 2021, office vacancy rates have stabilised or even fallen in some markets since Q2 2022. The overall vacancy rate in Europe stood at 7.4% at the end of Q3 2022, up slightly by 10 basis points compared to Q3 2021.

As with rents, vacancy rates vary greatly between the most sought-after business districts and out-of-town areas.

Investment remains high

€ 304bn was invested over the rolling year to Q3 2022. There was a decline in activity compared to Q2 2022 (-3%), but growth remained positive when considering investment for the first 9 months of the year, which almost matched the record level of 2019. “Historically, the fourth quarter is the busiest of the year for investment, which could mean an overall rise for 2022. The trend applied to all asset categories, but offices (+3%) were in line with their five-year average, largely underpinned by high activity in the business districts”, says Laurent Boucher.

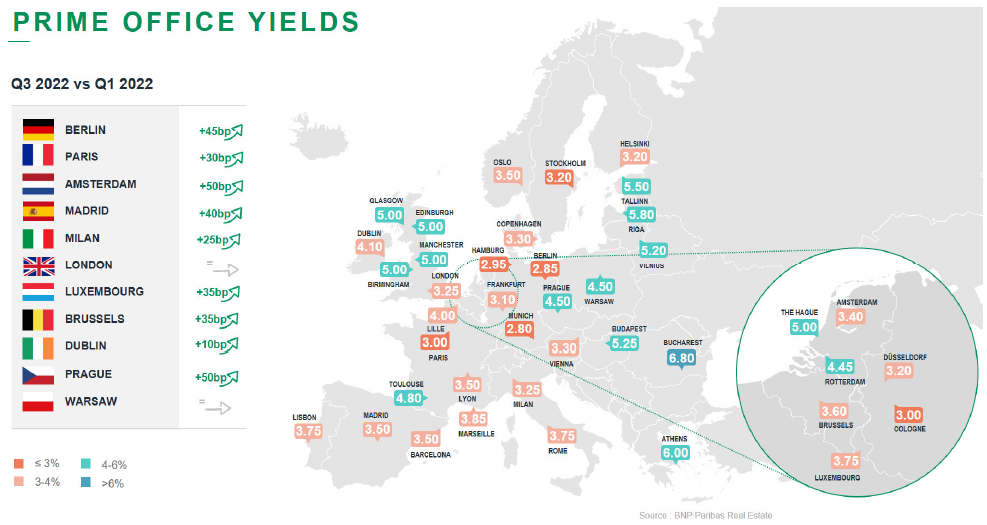

Prime office yields have started a decompression cycle, driven by the general rise in financial rates, while being cushioned by inflation and differentiated according to the quality and size of the assets.

The main cause is the structural change in the macro financial environment. Stubborn inflation is prompting a stronger response from central banks to normalise their monetary policy. As a result, key interest rates are rising fast, narrowing the spread with yields and causing participants to review how much real estate assets are costing, particularly offices.

*17 main European markets: Amsterdam, Barcelona, Berlin, Brussels, Dublin, Cologne, Düsseldorf, Frankfurt, Hamburg, Central London, Luxembourg, Madrid, Milan, Munich, Central Paris, Rome, Warsaw.

- Amira TAHIROVIC