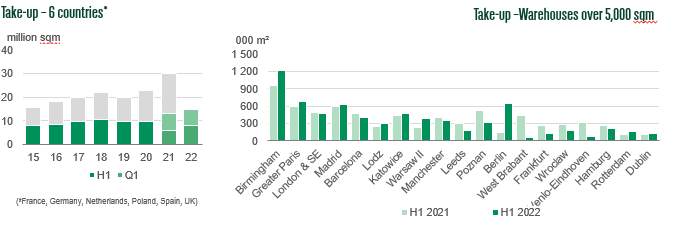

- The occupier market proved resilient with TAKE-UP IN THE six LEADING COUNTRIES rising BY 13% TO 14.9 MILLION SQM

- ANOTHER half-year historical record level of investment in Industrial and logistics with €30 bn invested

The occupier market proved resilient in H1 2022 even though the first signs of slowdown were recorded in Q2

The occupier market has shown good resilience during H1 2022, despite a difficult political and economic environment. Take-up in the 6 leading countries rose by 13% to 14.9 million sqm.

Poland and Germany achieved a record volume of transactions at mid-year, however other markets including France, the Netherlands and the UK, started to show signs of slowdown in Q2.

Demand is robust, driven by e-commerce. The strong changes in consumer behaviour triggered by the Covid-19 crisis supported on-line shopping supported continued growth of e-commerce in most markets.

“The shortage of new space has an impact on demand. Specifically it affects the choice of building in the between location and availability”. The vacancy rate is at its lowest ever, below 4% on average in Europe, whilst rising inflation is impacting construction and material costs. This in turn is exerting further rental growth, comments Craig Maguire, Head of European Logistics at BNP Paribas Real Estate.

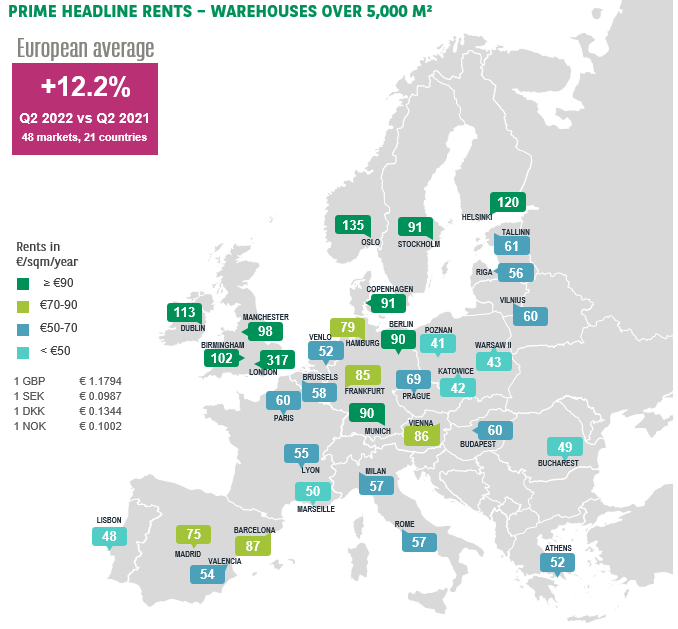

In this context, prime rents continued to increase, +12.2% (y-o-y) in H1 2022 based on 21 countries including 48 markets. The UK recorded the strongest change with over 25% growth over one year in Birmingham and London.

In Germany, the logistics market ran at full speed to reach a new record volume of transactions in H1 2022 boosted by large transactions from manufacturing companies. Pressure on rents is still strong as supply remains limited, particularly for modern space. The prime rent increased by 7% in Germany during Q2 2022.

In Germany, the logistics market ran at full speed to reach a new record volume of transactions in H1 2022 boosted by large transactions from manufacturing companies. Pressure on rents is still strong as supply remains limited, particularly for modern space. The prime rent increased by 7% in Germany during Q2 2022.

The UK occupier market maintained solid dynamics after the exceptional volumes recorded last year. Take-up in Q1 reached 1.8 million sqm fuelled by the structural growth of e-commerce and supply chains. While activity was reduced in Q2, it nonetheless remained strong with nearly 1.2 million sqm taken up. There is an acute shortage of new units supporting strong rental growth in the UK.

In Poland, the market is still thriving despite growing uncertainties in the region. The vacancy rate dropped to its lowest at 3.1%. Prime rents increased significantly stepping up in the main logistics hubs from €41 to €44 in Q1 to €47 €52 in Q2.

In France, after a strong start to the year boosted by demand for large warehouses, the market slowed down with 710 000 sqm taken up in Q2. Overall, supply remains scarce in most submarkets. The vacancy rate is still low, at around 3%. Competition between occupiers for high quality buildings remains sharp, implying some prospects for rental increases in prime locations.

In the Netherlands, the market is still recording strong activity despite a decrease in H1 2022 compared to the record volume reached last year. Due to low availability in the main logistics hotspots, take-up continued to shift towards less established locations. Robust demand and low availability are still putting pressure upward on rents, as seen in Rotterdam in Q1, and then Amsterdam and Venlo in Q2.

In Spain, the market achieved yet again a historic record volume of transactions in H1 2022. Activity was stimulated by e-commerce and food retailers. Vacancy rates are still low, particularly in Barcelona at around 2.5% and 6% in Madrid. Low vacancy rate is creating the conditions for rental growth. Yet prime rents have been stable over the past 3 quarters.

H1 set another half-year historical record level of investment, even with a slower Q2

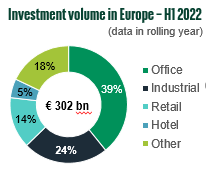

Industrial and logistics Investment volumes in Europe reached over 30bn in H1 2022, another record for a first half.

The sector maintained a strong market share over other asset classes in most countries, accounting for 24% of total commercial real estate in Europe.

The positive sentiment in the occupational market is continuing to encourage capital deployment in the sector. Occupation is being driven by the ongoing surge of online retail and 3PL occupiers, and their structural growth to meet changing consumer habits.

“In Q2, the market dropped by 16% compared to the previous quarter. Investor demand remains strong even though the volumes may be challenged by increasing scarcity of stock, geopolitical risk in Central and Eastern Europe and the suppression effect of inflation on consumer demand”, analyses Craig Maguire.

“In Q2, the market dropped by 16% compared to the previous quarter. Investor demand remains strong even though the volumes may be challenged by increasing scarcity of stock, geopolitical risk in Central and Eastern Europe and the suppression effect of inflation on consumer demand”, analyses Craig Maguire.

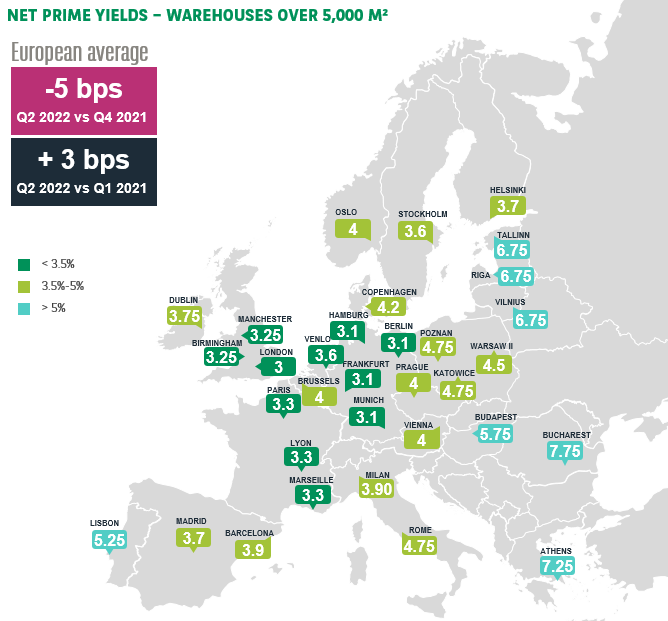

Prime yields started to decompress in some of the leading European markets including France, Germany, Spain and the Netherlands. Rising long-term government bond yields and inflationary pressure are impacting logistics prime yields. Further decompression of logistics prime yields is expected throughout Europe.

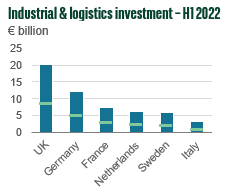

In the UK, the industrial and logistics investment market showed some signs of slowing down, challenged by increased scarcity of stock and economic uncertainties. Unlike other European markets, prime yields remained stable but signs of decompression are expected in Q3.

In Germany, the market recorded a historic volume of transactions but the dynamics of the market slowed down in Q2. Given the financial context with rising interest rate, prime yields decompressed by 10 bps in Q2 to 3.10% in the main markets.

In France, the market kept a strong dynamics in H1. As a result of the steep increase in government bond yields, logistics prime yields shifted by 10 bps in Q2. Further decompression is expected by the end of the year.

In the Netherlands, the investment market in industrial and logistics maintained good momentum despite a scarcity of products available. The prime yield started to decompress at 3.15% in the Netherlands and stabilized at 3.6% in Venlo and 4% in Rotterdam.

In Poland, following a record volume last year, activity slowed down in H1 2022. Prime yields remained stable at 4.5% for standard assets but decompression is expected in the forthcoming months given the geopolitical risk in the region and the economic and financial context in Europe.

In Spain, the volume of investment decreased sharply in H1 compared to the outstanding year 2021. Activity remained steady, returning to the average volume of investment in industrial and logistics in a first half. The prime yield for big boxes decompressed by 20bps in Q2 2022 to reach 3.9%.

- Amira TAHIROVIC