The logistics market is in one of its strongest positions for decades but adjusted down due to the exceptional volumes achieved in 2017

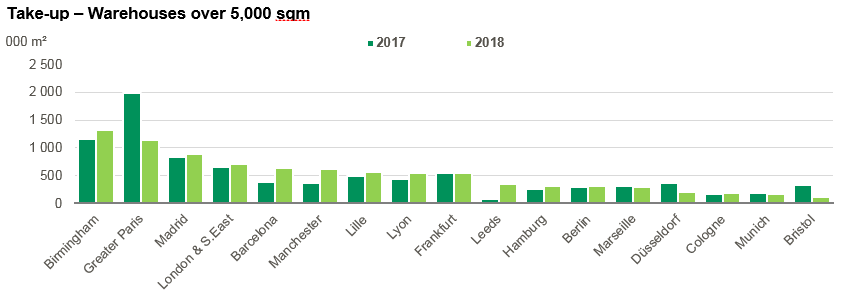

- Logistics take-up for warehouses over 5,000 sqm in 21 cities: +1% in 2018 vs 2017

Following the record volumes achieved in 2017, the market remained strong, fuelled by e-commerce and constrained by short supply plus low vacancy rates across Europe. Demand is strong, take-up levels are 15% above the 5-year average. Some countries like Germany, Spain and the Netherlands hit a new record volume of transactions in 2018.

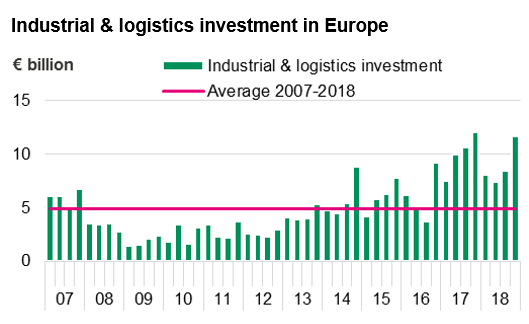

- Industrial and Logistics investment in Europe: -11% in 2018 vs 2017

The investment market adjusted down as expected after the exceptional volumes recorded in 2017. Prime yields compressed further in Europe to bottom at 4.0% in the UK and 4.05% in Germany. Logistics prime yields are still set to decline in numerous European markets over 2019.

Take-up: the European logistics market is in its strongest positions for decades

The occupational fundamentals are probably the strongest we have seen for the past 15-20 years. 2018 confirms this trend with exceptional volumes of transactions in the UK, Germany, Spain and the Netherlands. Demand is fuelled by ecommerce and tempered by low supply, which is exacerbated by limited speculative development. On-line sales continue to grow by 12 to 14% per year. This is the main driver for the logistics market in Europe. Supply remains insufficient overall to meet end-user requirements; it is particularly lacking for XXL warehouses. This has resulted in low vacancy of around 5% as a European average.

Rents are rising slightly, +4% in 2018 in a panel of 38 cities across Europe. This reflected strong demand and low levels of supply, especially for grade A warehouses.

Germany hit another record year. The volume of transactions increased by 21% over the year to reach nearly 6.7 million sqm in 2018. Due to inadequate supply of large-scale modern space occupiers continue to turn to tailor-made solutions. Demand has been particularly strong outside the main hubs in locations where rents are lower and where it is easier to develop new programmes.

In France the volume of transactions decreased by 14% in 2018. This compares with an exceptional year in 2017, particularly in Greater Paris where take-up doubled, boosted by XXL deals. In 2018, the market came off its peak moving down to a level that is still over 20% above the 10-year average. It is the second time the volume reached 4 million sqm of transactions. The strength of demand means that building starts and speculative development picked up this year to its highest level since 2009.

The UK warehousing market has been particularly robust over the past 18 months despite the Brexit vote in June 2016. In 2018, take-up increased by 27% year-on-year to 3.7 million sqm.

In Spain, the market is particularly dynamic boosted by all-time record take-up in Madrid and Barcelona. Take-up rose by 21% to break a new record of 1.6 million sqm in the three main Spanish markets in 2018.

Industrial and logistics investment: demand is wide and attracting new entrants in 2018

Industrial and logistics investment is steady and strong. Yet, product supply is inadequate to meet intense demand from all risk profiles. Investment volumes have doubled in 5 years. Logistics and industrial investment represents 13% of the total commercial real estate market in Europe. 2017 was a record year especially for platform transactions such as Logicor and Gazeley, but if we exclude these, the results in 2018 are higher than 2017.

Anita Simaza, Director for European Logistics Investment said "The depth of investor demand is very good from core to opportunistic. The origin of capital is wide and global. Indeed, Asian investors are in the process of acquiring logistics across Europe and a few newcomers with no exposure to logistics are still entering the market. We could expect great investment for 2019, reflecting still attracting logistics prime yields compared to other assets”.

The UK and Germany confirmed their leading position in the logistics and industrial investment market in Europe. Following the all-time record high in 2017, unsurprisingly, both markets dipped down by 24% to €9.3bn in the UK and 22% to €7.2bn in Germany and still at the second highest levels ever recorded.

The Netherlands hit a new record volume of investment in 2018. Indeed, industrial and logistics recorded its highest level of investment ever, representing 26% of total Dutch commercial real estate investment in 2018.

In France, the market remained strong even though the volume dropped by 31% in 2018 to reach the €3.1bn. The prime yield is at its lowest level at 4.75%. Given the high demand for logistics and competitive pricing against other asset classes, yields will decline again to 4.5% in 2019.

In Poland, the market soared in 2018 to €1.9bn. It is attracting capital from the US, Germany and the UK and more recently Asian investors.

In Spain, the market is buoyant boosted by the strength of the economy. Industrial and logistics investment reached a new record with €1.3bn in 2018. The scarcity of products resulted in significant yield compression to 5.3%.

- Amira TAHIROVIC