European Economic Growth: Slow and steady

The strong global growth rates of late 2017 slowed slightly in early 2018, reflecting tighter monetary conditions and emerging capacity constraints. Growth assumptions for the world economy remain at a high level for 2018 underpinned by a powerful combination of job creation, rising company profits and easy access to financing. The slowdown in Eurozone growth mirrors Global economic trend. Consequently, the ECB has already announced that it does not intend to raise interest rates before summer 2019. The attainment of inflation with the central bank’s target still requires a high level of monetary support.

Ongoing momentum for investment

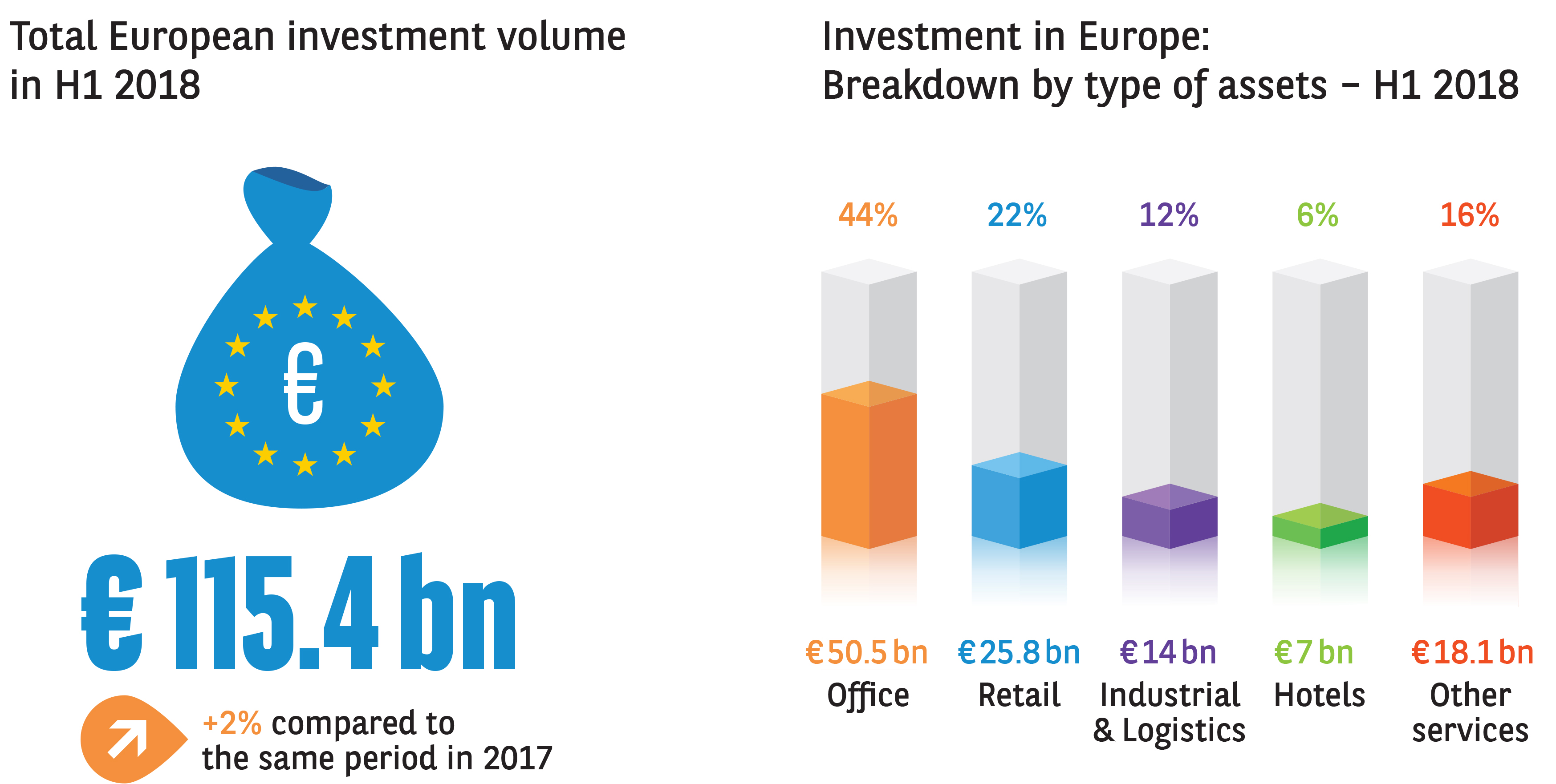

Commercial real estate investment in Europe advanced again during H1 2018 to reach €115.4bn, 2% above the same period in 2017. “2017 was the record year for investment volumes in Europe and 2018 began strongly, notably with some very large office deals. Global investors believe in the positive economic environment and the healthy occupier markets in Europe”, says Larry Young, head of International Investment Group at BNP Paribas Real Estate. This confidence benefited the office sector (+9%), reflected in a share of 44% of total investment volume. The retail investment volume stabilized while industrial & logistics sector fell (-16%) to 12% market share, however this was from a very high level in 2017.

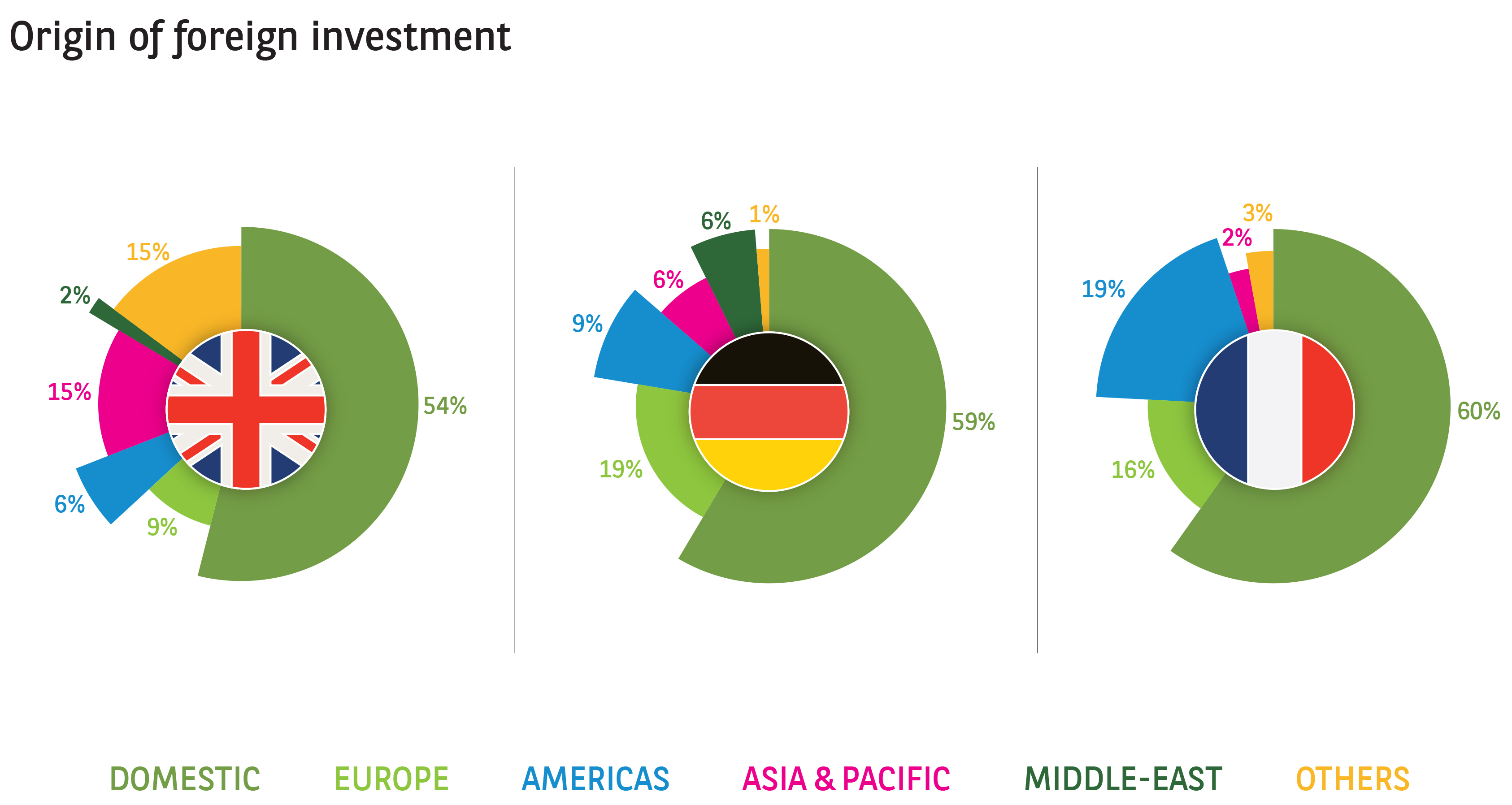

Germany contributed greatly to this performance by exceeding the previous year’s result (+0.1%) and recording the second-best H1 turnover of all time (€26.1bn). The United Kingdom (€30bn) remains the leading European market despite a -6% reduction versus H1 2017. The French investment market experienced an exceptional first half (+48% vs 2017) with volumes of €12.5bn. Most of other European countries experienced an upturn such as Ireland (+224%), Poland (+110%) or Belgium (+81%). Only Czech Republic (-57%), Italy (-35%) and Spain (-22%) saw reductions compared to 2017.

Foreign commercial real estate investment in Europe

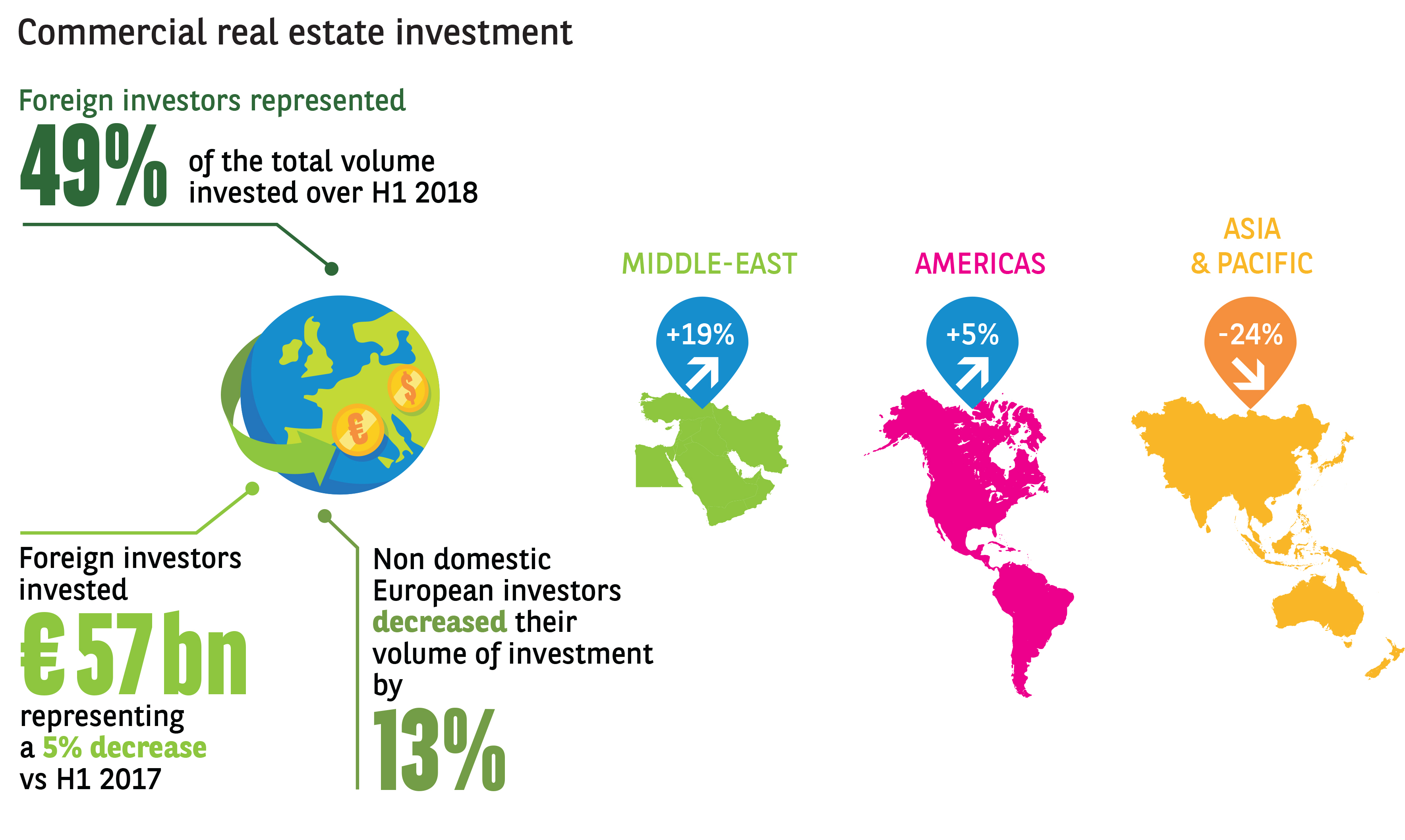

Foreign investor presence in the investment market declined. With almost € 57bn invested during H1 2018, foreign investment volume decreased by 5% versus H1 2017 and now represents a share of 49%. The change reflects shifts in investor composition. After a year dominated by Asian activity, investment from this region slowed in H1 2018 (-24%). However, there are large deals ongoing, notably in the United Kingdom. European cross border investors were also less active (-13%). Middle East and North American investors were more present in the market with 19% and 5% increases.

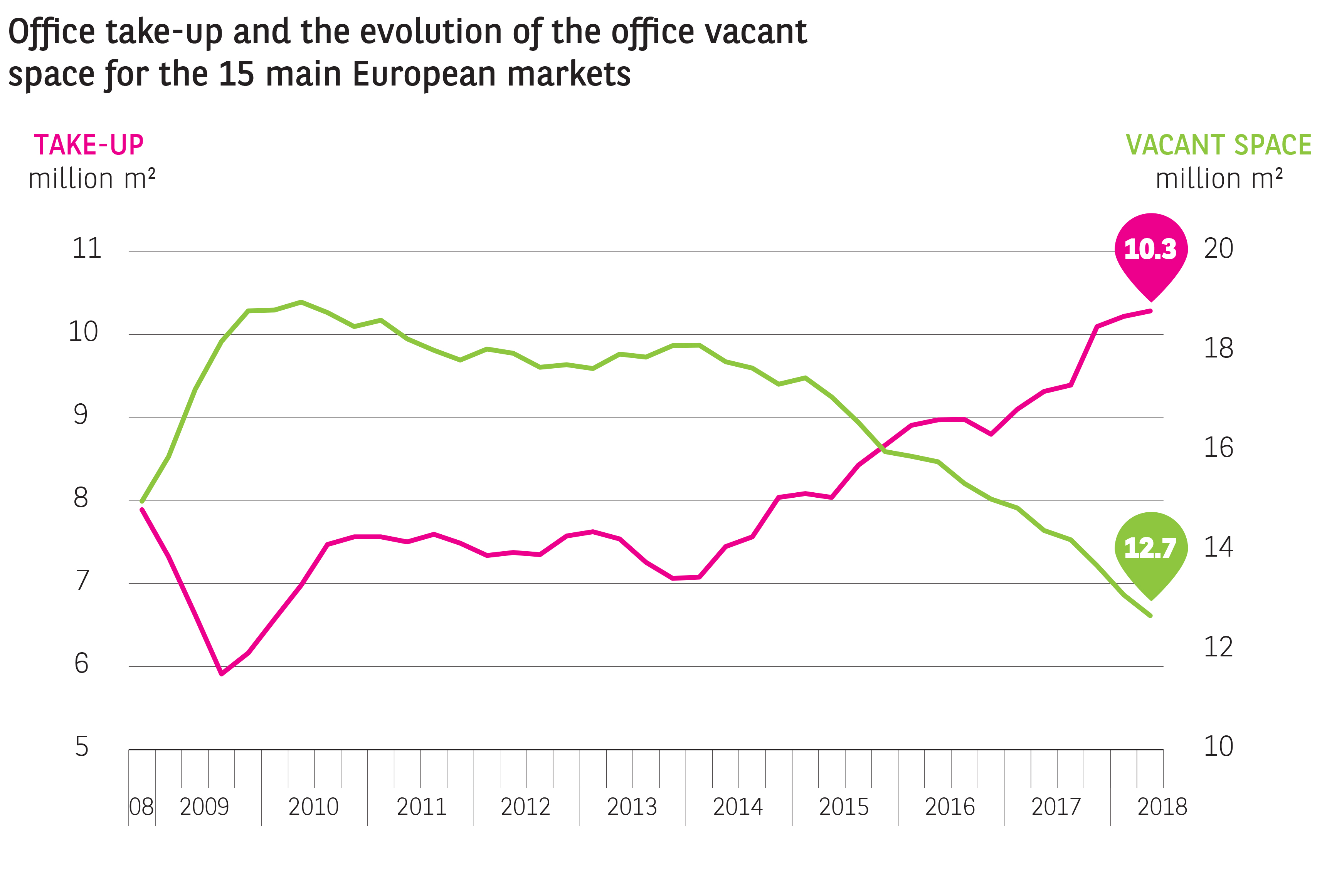

Occupier markets still rising

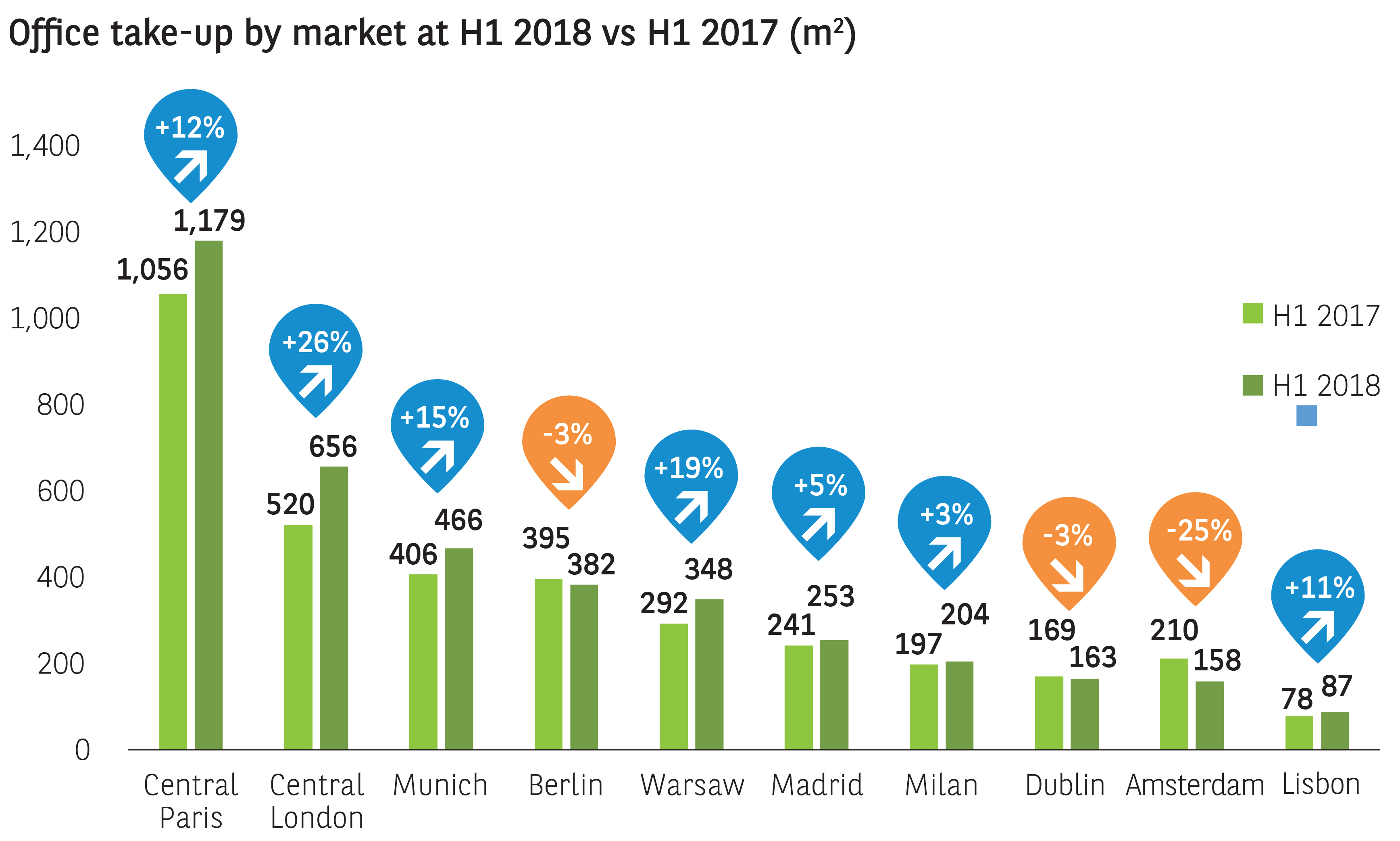

The dynamism of the European office letting market did not wane in Q2. Transactions amounted to 4.79 million m² since January - a rise in take-up of 4% compared to H1 2017. The market in Central London rallied to finish 26% up vs H1 2017. Deals for large units continued to drive the volumes in Central Paris, where they increased by 12% compared to the same period in 2017. Despite a very slight dip (- 2%) due to exceptional results in H1 2017, the attractiveness of the 4 main German cities remained unchanged while outstanding results in H1 were also observed in Lisbon, Warsaw and in Dublin.

Aymeric Le Roux, executive director of International Advisory & Alliances at BNP Paribas Real Estate comments: “After reaching exceptional results in 2017, the office markets across Europe are still thriving in 2018. The appeal of grade A office to occupiers remains undisputed, pushing up the rents in most European cities. Demand is also more and more driven by coworking companies, which are progressively becoming major actors on the letting market in most European markets”. Vacancy plunged across Europe with the share of empty offices dropping the most in Warsaw (-420 bps vs last year), Amsterdam (-290 bps), Lisbon (-240 bps), Prague and Milan (-220 bps). In the meantime, prime rental values remained steady or increased in all main European markets, except in Central London (-10% vs. H1 2017). The most important changes over the last 12 months were in Berlin (+13%, €408/m²/year), Frankfurt (+12%, €516/m²/year), Madrid (+11%, €408/m²/year), Milan (+10%, €570/m²/year) and Lisbon (+8%, €246/m²/year).

- Amira TAHIROVIC