European Economic Growth: a global slowdown

Since 2018 began, Eurozone growth has been slowing. The slowdown can be explained by several factors: a mechanical effect after a buoyant 2017, political uncertainties and the emerging supply constraints. The unemployment rate is close to its structural level (where there is mismatch between jobs and skills) as opposed to its cyclic level (driven by business cycle). International trade was responsible for a substantial share of this disappointing performance. Forecast inflation in Europe led the ECB to announce the end of quantitative easing in December 2018. However, interest rates are set to be constant to support the economy. The probability of a refinancing rate increase in 2019 is low and remains dependent on the sustainable convergence of inflation towards its target of 2%.

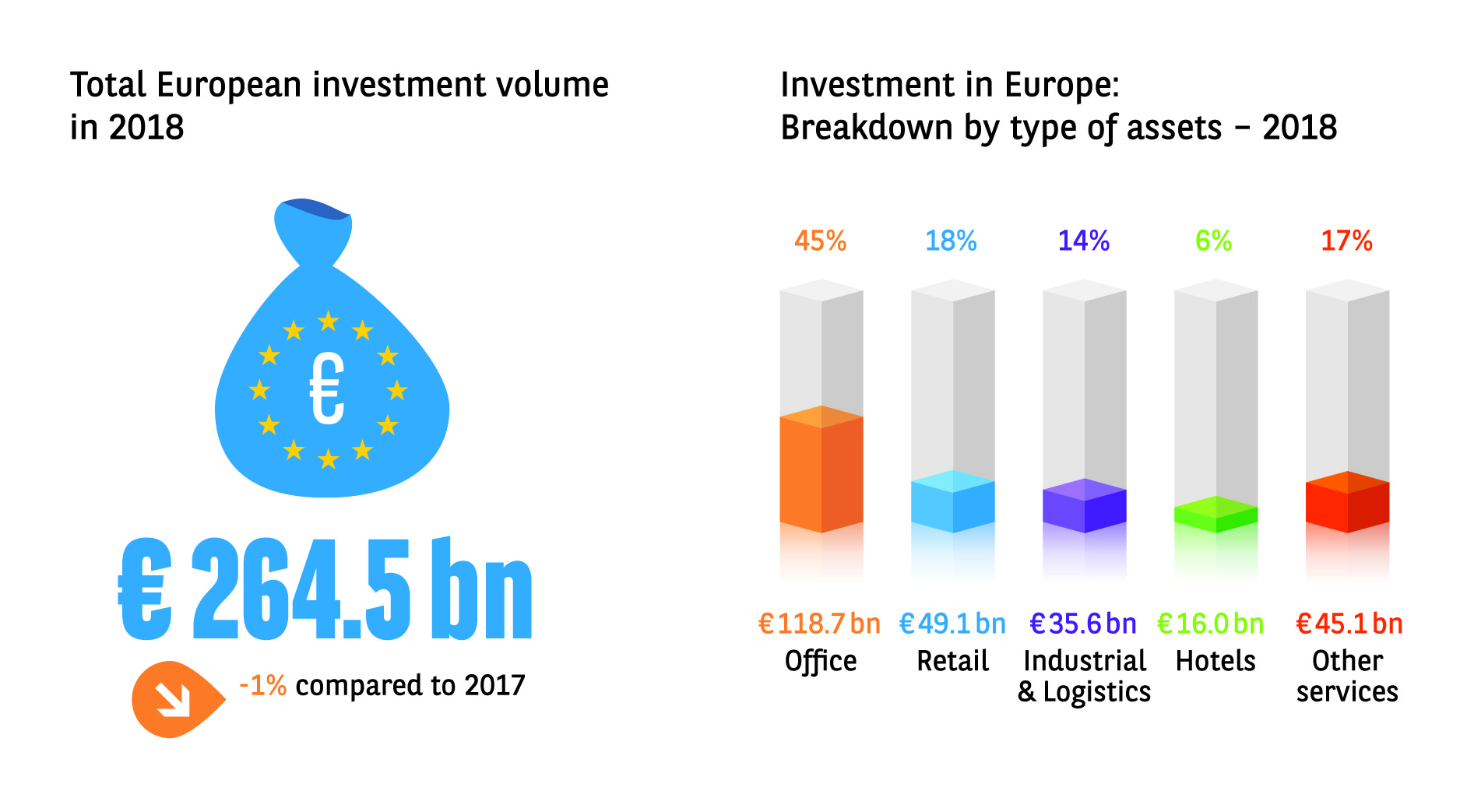

2018 Europe investment turnover in continuity with record year 2017

Commercial real estate investment in Europe stabilized in 2018 to reach €264.5bn, 1% below the all-time record of 2017. “If 2017 was the year of  logistics, 2018 was definitely the year of offices. Compared to the other main asset types, offices showed resilience and reached a 10 year high, thanks to a large number of mega deals”, said Larry Young, head of International Investment Group. Except for offices (+4%) and others (+18%), all the sectors saw a decrease. Retail (-16%) has been following a downward trend for the last three years, while industrial & logistics investment (-7%) remains very close to 2017 record level of €38.2 bn

logistics, 2018 was definitely the year of offices. Compared to the other main asset types, offices showed resilience and reached a 10 year high, thanks to a large number of mega deals”, said Larry Young, head of International Investment Group. Except for offices (+4%) and others (+18%), all the sectors saw a decrease. Retail (-16%) has been following a downward trend for the last three years, while industrial & logistics investment (-7%) remains very close to 2017 record level of €38.2 bn

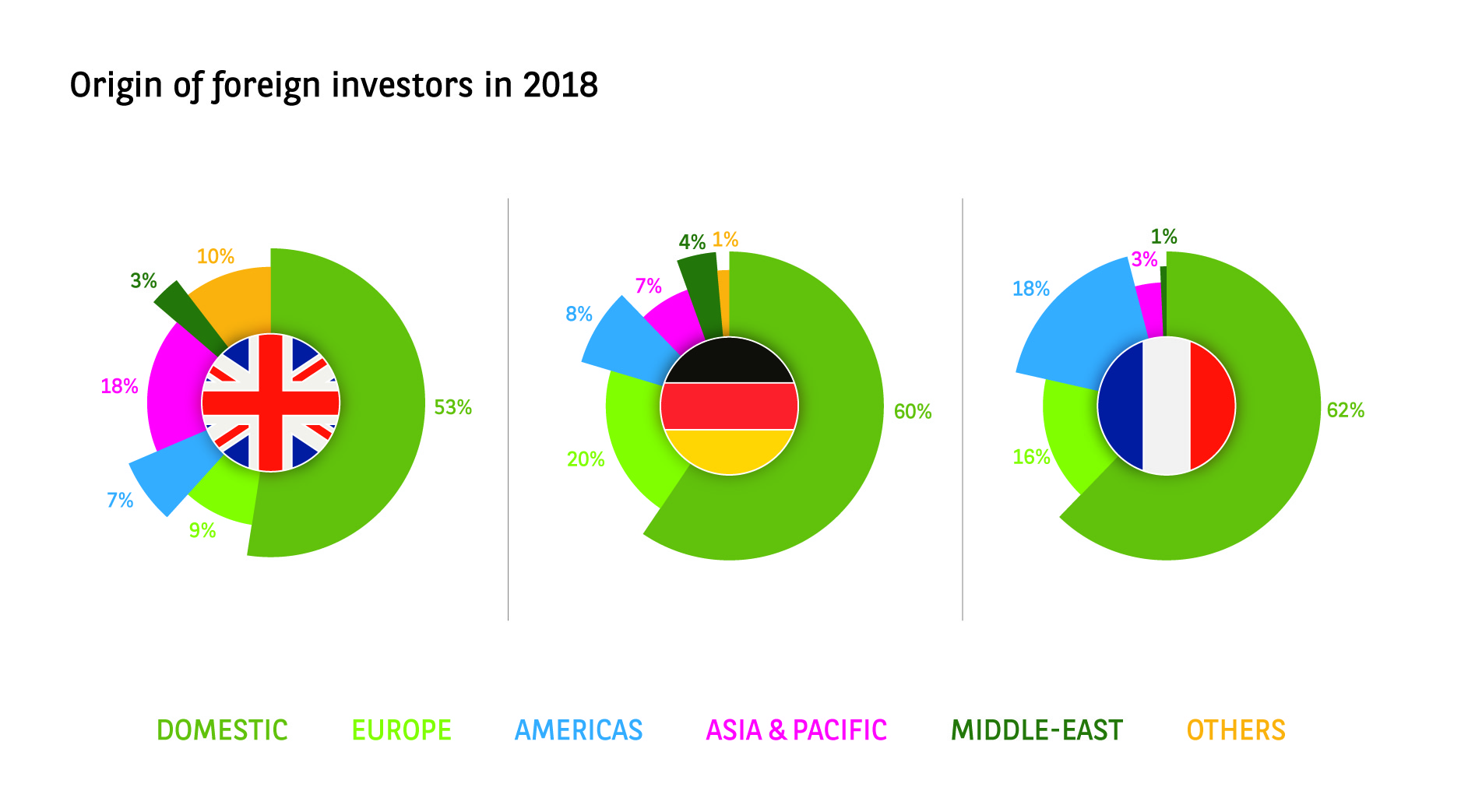

With an investment volume of €66.5bn, the United Kingdom is still the leading European market despite a 10% decline that impacted the European average. This result is mainly attributable to the withdrawal of foreign investors (-21% vs 2017) in conjunction with the current political and economic backdrop. Investment activity in Germany was very dynamic in 2018; it reached an amount of €61.5bn, which represents an all-time high for the market. A record level was achieved in France as well with a turnover of €32.8bn. The trend was also positive in most European countries, such as Netherlands (+3%), Spain (+9%), Poland (+42%), Belgium (+36%) or Ireland (+43%). Only a few countries such as Italy (-22%), Czech Republic (-32%) experienced a decline.

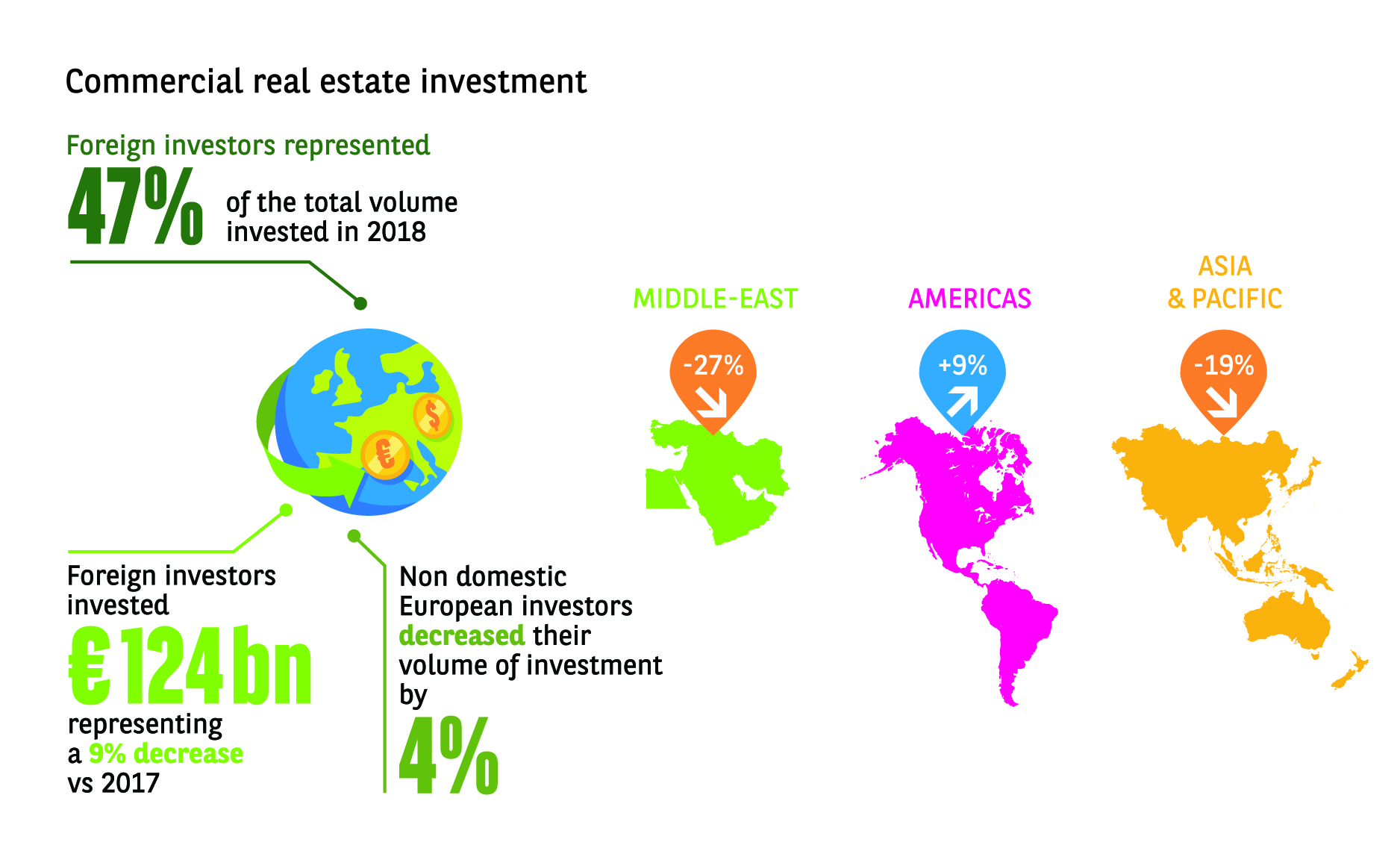

Foreign commercial real estate investment in Europe is still strong

In 2018, foreign investors presence in the European commercial real estate investment market faded (-9% vs 2017). With a total amount of €124bn invested, they still represented 47% of the market, a share in line with the 5-year average. Americans investors, after strong activity in 2014 and 2015, withdrew from Europe in 2016 (-40%) and slow to return since and slow to return since (+7% in 2018). Asian investment, after reaching a record level in 2017, decreased in 2018 (-19%) but remains exceptional compared to long term. Middle East (-27%) and European cross border investments (-4%) lightened their presence in the market.

In 2018, foreign investors presence in the European commercial real estate investment market faded (-9% vs 2017). With a total amount of €124bn invested, they still represented 47% of the market, a share in line with the 5-year average. Americans investors, after strong activity in 2014 and 2015, withdrew from Europe in 2016 (-40%) and slow to return since and slow to return since (+7% in 2018). Asian investment, after reaching a record level in 2017, decreased in 2018 (-19%) but remains exceptional compared to long term. Middle East (-27%) and European cross border investments (-4%) lightened their presence in the market.

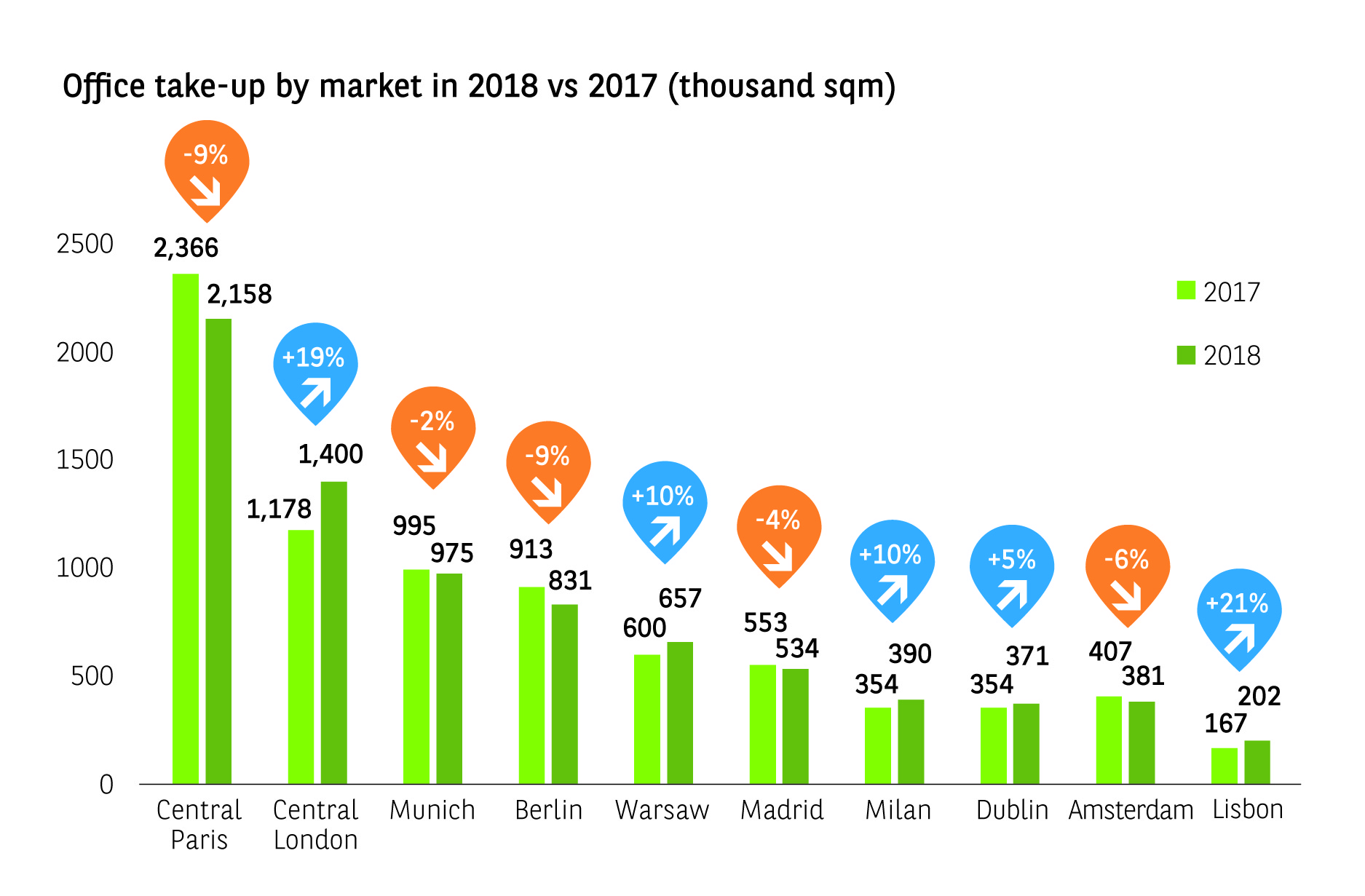

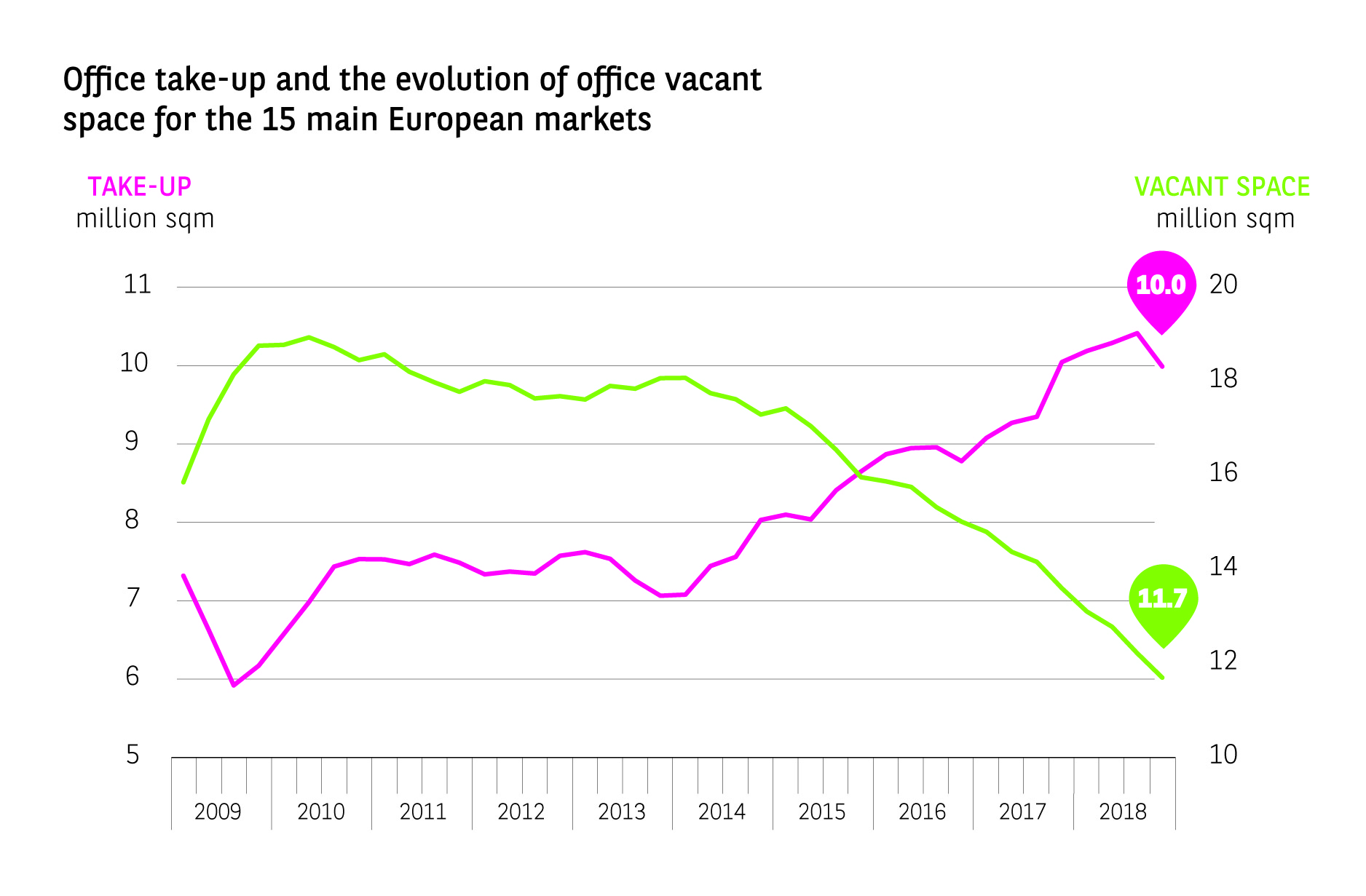

Strong occupier take-up performance continued in 2018

Occupational activity stayed particularly lively in the main 15 European markets in 2018, even though volumes of take-up in Q4 2018 were 13% down compared to the exceptional Q4 2017. As such, 10.02 million sqm was transacted last year, only 1% behind 2017, by far the most active year of the decade. The Central London market increased for the 3rd year in a row and reached 1.4 million sqm, while the 4 main German markets remained well above their long term average with 3.04 million sqm transacted, despite a 8% drop. Volumes in Central Paris diminished by 9%, due to the lack of very large deals. Very high results were achieved in Vienna (+54%), Luxembourg, Lisbon (+21%), Milan and Warsaw (+10%).

Aymeric Le Roux, executive director of International Advisory & Alliances comments: “The office markets in Europe continued on their healthy trend in 2018. Vacancy is at its lowest in most markets, especially in the CBDs, while the appeal of grade A office buildings remains undisputed. As a consequence, prime rental values experienced significant increases in Europe”. Indeed, vacancy in Europe contracted again, with only 6.4% of empty premises in Europe on average. Vacancy dropped the most in Amsterdam (-310 bps) and Warsaw (-340 bps) but the German markets still display the absolute lowest vacancy rates, such as in Berlin (1.7%). In the meantime, prime rental values remained steady or increased in all main European markets, except in Central London (-2% vs. the end of 2018) where prime rents reached £1,211/m²/year. Madrid (+13%, €432/m²/year) saw the most significant growth in rental values. Other big increases were in Hamburg, Berlin (+9%), Milan and Frankfurt (+7%).

- Amira TAHIROVIC