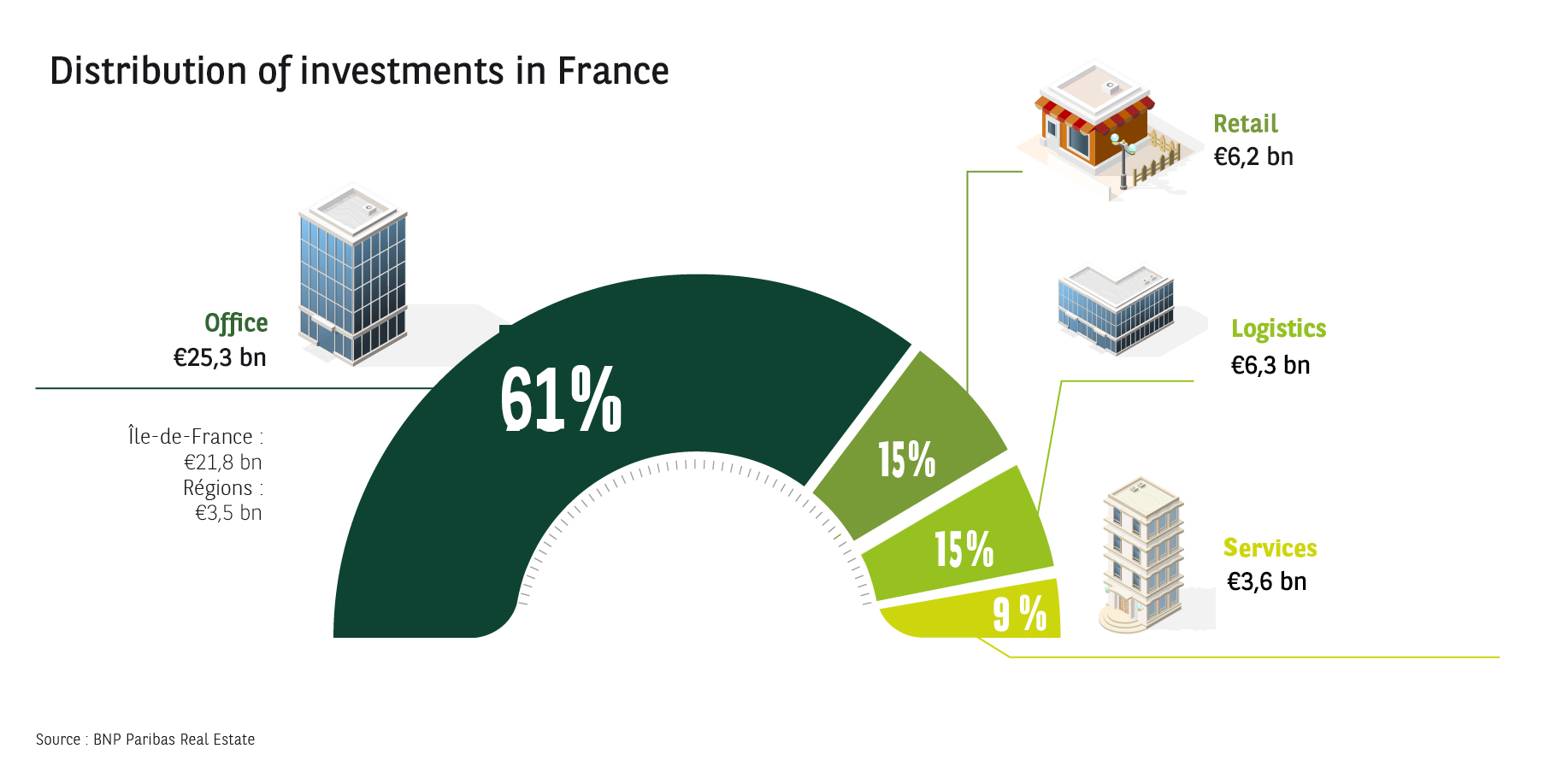

Over € 25bn invested in Offices

Paris overtakes London in terms of foreign capital invested

Investment of around € 35bn expected in France in 2020

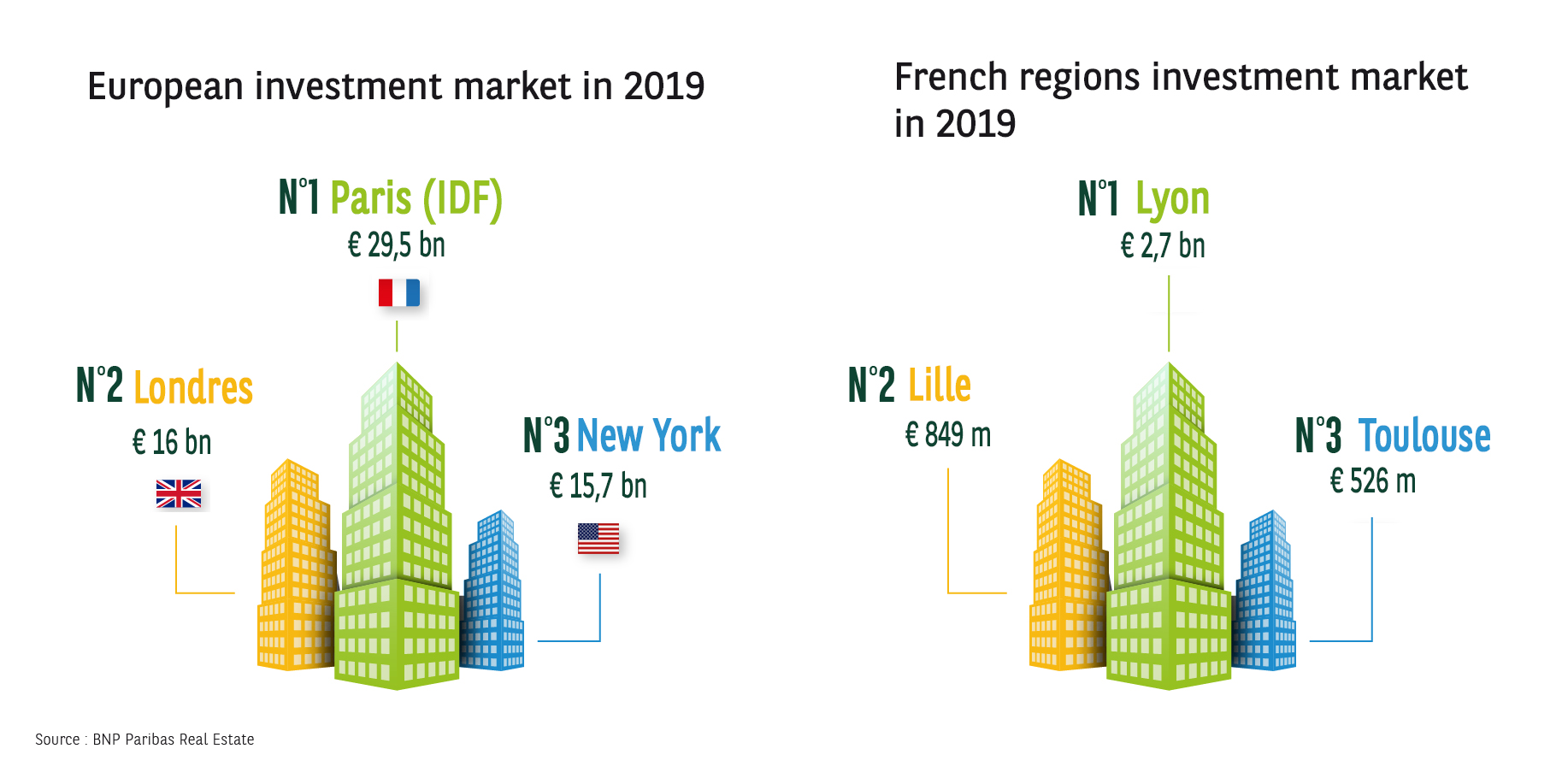

Paris becomes the top European market for foreign investors

Investment in French commercial real estate reached a record level of over € 41bn over the full year 2019, i.e. growth of +19% over one year. Asia has clearly stepped up its involvement in France with € 5bn investment in “core” assets while North Americans also continue to invest in the country.

Paris remains very appealing to investors. In 2019, it was the top market targeted by international investors as a percentage of total flows. Paris beat London for the first time and came just behind New York in terms of foreign capital invested.

Offices the preferred asset in France: new record with over € 25bn invested

Offices remained very comfortably in the majority in France and attracted a record € 25bn investment over 2019. With the overall total up 8% over one year, investment in the Ile-de-France office market was almost € 22bn.

Investment in the regions remained stable at € 3.5bn, still with excellent fundamentals.

There were more off-plan sales in the regions than in 2018 at over € 1.2bn, i.e. over 40% of the market. Lille, Lyon and Bordeaux were first, second and third respectively in terms of off-plan sales and in 2019 cities like Nantes, Strasbourg, Toulouse, Rennes and Montpellier also shared this flourishing market.

Capital values are rising sharply with a very strong scissor effect: falling interest rates and rising rents, prompting investors to increasingly take a value approach according to the efficiency and quality of the unit.

In Île-de-France, major deals for over € 100m accounted for 70% of overall investment across a total of 57 transactions in 2019.

Investment in Retail premises in France came in second at € 6.2bn

This market is thriving with growth of 38% vs. 2018. This record increase stems from a particularly buoyant fourth quarter. All types of retail premises combined now account for 15% of investment in commercial real estate in France.

It is still the high street transactions that are really driving this market, with € 3bn invested. Inner city shopping centres and food store premises also contributed to these near-record levels of investment.

Investment in Logistics sets a new record at € 5bn.

Logistics has performed better than ever in terms of both amounts invested and yields, with French investors making a comeback. A record was already set in 2018 with € 2.8bn invested. This almost doubled in 2019 to a total of € 5bn. This corresponds to almost 6 million m² sold, i.e. 50% more than in 2018.

This amount was generated by around 50 investors across about 100 transactions (vs. just 65 in 2018). Of these 100 transactions there were 11 deals for over € 100m and a sharp increase in individual transactions: 72 in 2019 vs. 47 in 2018.

Investment in hotels rose sharply to € 2.6bn

Investment in hotels rose dramatically, up to € 2.6bn in 2019 vs.€ 1.7bn in 2018. The hotel sector benefited from a very favourable events calendar, such as the Women's World Cup, the 75th anniversary of the D-Day landings and the G7 in Biarritz.

In 2019, the average RevPar was € 65, up 1.8% compared to last year, despite the social unrest that prevailed. The average price per room now stands at € 94, stable compared to last year, all categories combined.

The geographical distribution was more balanced in 2019 with 49% of investment in the Regions, whereas in 2018, most investment was in Ile-de-France. Meanwhile, there was a sharp increase in portfolio transfers, which accounted for 46% of investment.

Serviced accommodation: high development potential

Investors have a growing appetite for this asset category, as illustrated by the increase in lump investments. Retirement and student accommodation offer the greatest potential for development and investment.

Major advantages include resilience, long-term visibility, growing demand, security, durability and ease of management, added to which are yields that are higher than other asset classes; 4% to 5% on average according to the category, location and quality of the operator. Lastly, the reversibility potential of these residences makes various exit options possible.

Investment funds are fairly active and have bought about half of housing sold in batches over the past two years.

These residential assets have the advantages and security of the office sector while also representing a community investment. As such, to cope with the growing need for suitable housing and increasing demand for serviced properties, the experience and business models of serviced accommodation operators makes them best equipped to accompany profound societal changes.

Outlook: high level of investment expected in 2020

The investment market has reached a new scale, in terms of volume and diversification, and several factors argue for a high level of investment:

- a resilient economy that allows rental markets to maintain momentum, with relatively low vacancy rates and rising rents in the main markets;

- the abundance of global liquidity and institutional and private investor portfolios that are expected to boost allocations to real estate according to all market surveys;

- appeal of the French market

- still a very positive outlook for capital gains.

The current environment and outlook make us optimistic for 2020. Although the € 40bn threshold exceeded last year may seem exceptional for now, the coming years should see an average of € 35bn. We are also likely to see further yield compression for all assets” anticipates Olivier Ambrosiali, Deputy Head of the Sales and Investment division for BNP Paribas Real Estate Transaction France.

- Amira TAHIROVIC