European office prospects: further yield compression expected in 2018

BNP Paribas Real Estate Research said that European growth will strengthen over the next years, driven by a considerably improved domestic demand. This development is to the great benefit of the occupational markets that have lagged in Europe as well as supporting those that are already healthy.

Demand for office space across Europe has been robust with an average growth of 7% in each of the past three years. 2017 has been no different and BNP Paribas Real Estate anticipates that the year as a whole will record a similar level of growth. Of course at city level the volatility will differ because of the different stage of the property cycle.

Cost of space mirrors vacancy patterns and economic growth. The largest cities will remain the most expensive in terms of prime rents; London and Paris. Supported by a fall in the vacancy rate and a stable economic environment, the German cities will post some of the fastest rental growth; Berlin (7%, pa), Frankfurt (4.2%, pa) Hamburg (2.2%) and Munich (2.0%).

Thomas Glup, senior economist at BNP Paribas Real Estate said “German cities are likely to see a strong rental growth over the next years, particularly in Berlin with the fastest growth due to the bottleneck of space and the catch up effect, followed by Frankfurt which could benefit from the Brexit.”

As the CEE nations will see substantial deliveries occurring, their prime rental growth is likely to remain low at best and the effect of the increased supply will be felt most in average rents.

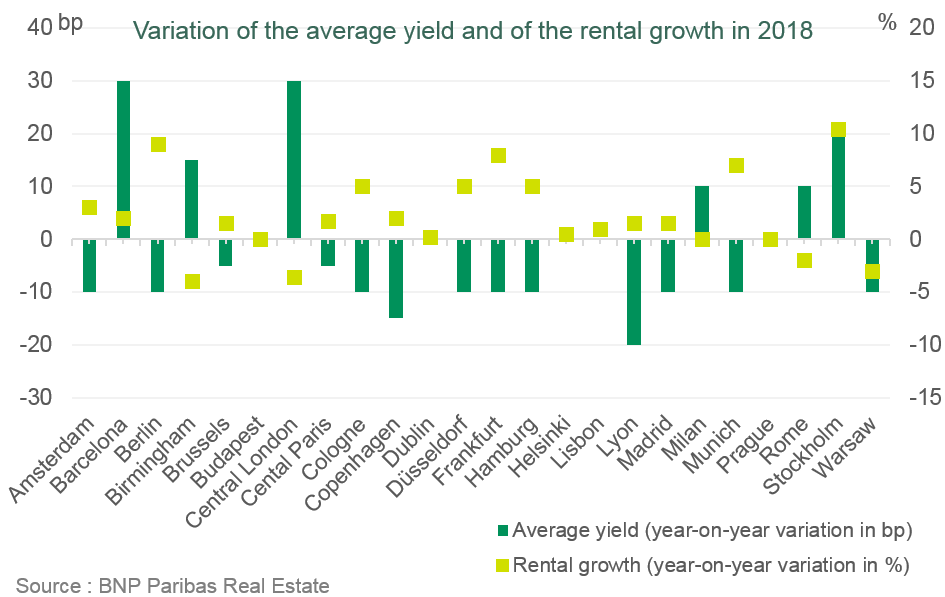

The story of European investment since 2013 has been one of continued yield compression and accelerated capital growth, supported by record transaction volumes. BNP Paribas Real Estate Research said that as we move into 2018, the cycle in Europe broadly is likely to be at a point of inflexion. Similar to the occupational market, cities across Europe are all at different stages in the cycle and the rapidity and magnitude of change will differ. UK cities, even without Brexit, are expected to see capital growth fall back and yield expansion over the next year. Initially, further yield compressions are expected in most of the European markets and a stable income will be enough to ensure that total returns do not turn negative for most cities.

In 2018, there are some key economic drivers to watch out for in real estate market. First of all the global monetary policy has reached a juncture in 2017 with central banks aiming to normalize policy. However, central bank policies will still remain supportive of the economy and we do not believe that this is significant enough to make an impact on property yields. Then, the political disagreement between the Spanish Central government and Catalonia will inject some uncertainty into investor perception of Barcelona. However, with the actions that the Spanish government has taken so far, the uncertainty will most likely be short lived.

Telecharger

- Amira TAHIROVIC