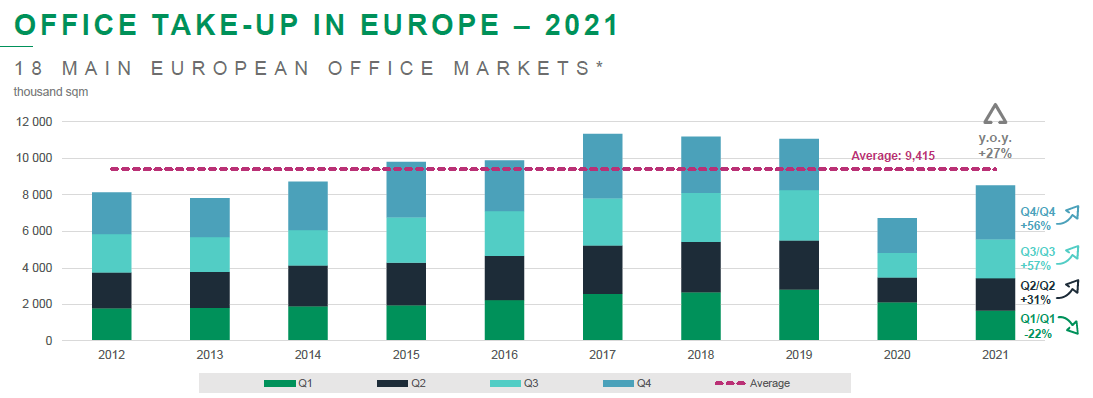

Office take-up in Europe saw a significant increase in 2021

With 8.5 million sqm of office space taken-up in Europe’s 18 main markets over 2021, the sector saw a significant increase compared to 2020 (+27%). The start of the year was quieter than expected due to recurring waves of Covid-19 infections, office take-up started to recover in the second quarter of 2021 and showed continuous improvement throughout the rest of the year, showing signs of normalization in the third and fourth quarters.

“Even though the pre-covid levels have not been reached over the whole year 2021 (-8%), take-up reached 2.95 million sqm during the fourth quarter of the year, which is in line with pre-covid usual volumes for Q4. The office market is on the road to recovery led by companies, which want to move to adapt their space to the new ways of working. That’s why values are set to rise in the most sought-after locations in Europe,” comments Richard Malle, Deputy Head of Business Services in charge of Research, Innovation and Data at BNP Paribas Real Estate.

Most markets showed strong rebound in volumes, such as in Barcelona (+85% compared to 2020), Central London and Brussels (+46% each), Central Paris (+36%), Milan (+34%) or in the 6 main German cities* (+27%). A few European cities still recorded decreases: Amsterdam, Luxembourg, Warsaw and Dublin.

Further improvements in the letting activity are expected for 2022 as 2021 was the first step towards the recovery of the office market. Take-up should accelerate in the coming months over all markets, without reaching pre-crisis levels yet. What is anticipated for the year to come:

- 3.5 million sqm in the 6 main German markets (+12% vs. 2021)

- 2.1 million sqm in the Paris Region (+13%)

- 0.94 million sqm in Central London (+18%)

- 3 million sqm in the Advisory 8 cities**

*6 main German markets: Berlin, Cologne, Dusseldorf, Frankfurt, Hamburg, Munich

**Advisory 8 (10 cities): Amsterdam, Barcelona, Brussels, Dublin, Luxembourg, Madrid, Milan, Rome, Warsaw, Prague

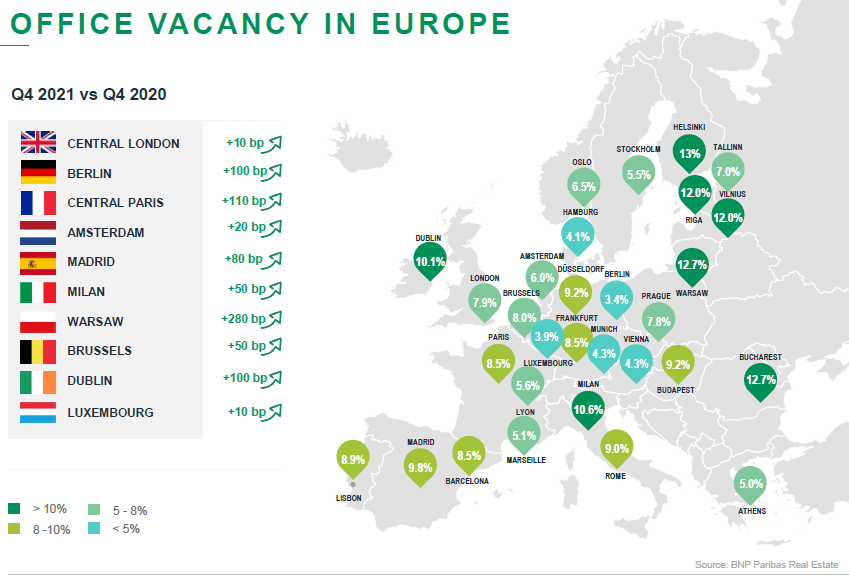

The vacancy rates seem to be stabilizing

After a strong increase in 2020 and in the first half of 2021, the vacancy rates in the office market have stabilized since the end of the second quarter of 2021, thanks to the progressive recovery of take-up. Most markets are still experiencing two-speed dynamics, with low availability in central areas and in new buildings on one side, and much higher vacancy rates in peripheral office districts on the other side, as companies still prefer to invest in prime buildings and prime locations.

The overall vacancy rate in Europe was at 7.3% at the end of 2021, which represents an increase of 50 bps from the end of 2020.

The biggest changes between 2020 and 2021 were recorded in Warsaw (+280 bp), Central Paris (+110 bp), Berlin and Dublin (+100 bp each).

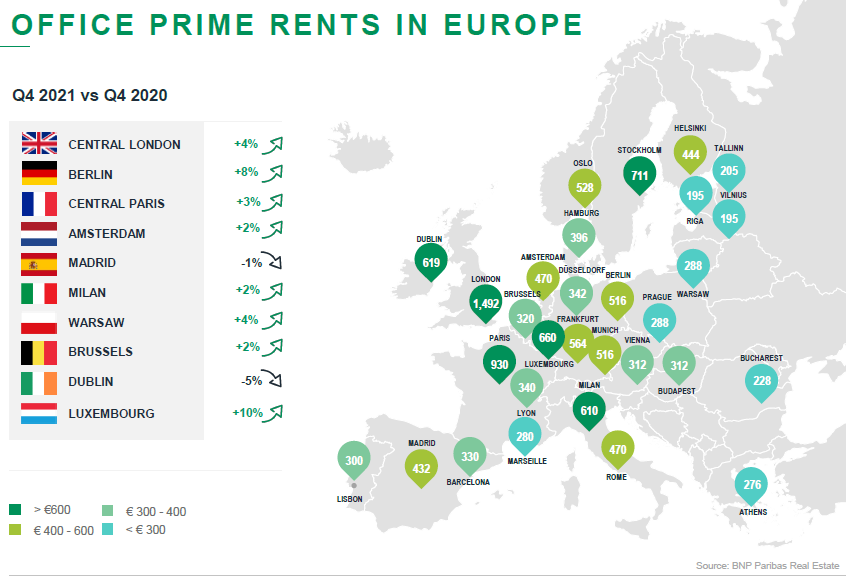

The prime office market segment did not suffer from the Covid-19 crisis

The rents of offices considered as “prime offices” were mostly unaffected by the crisis and did not suffer from the slowdown in take-up. Indeed, in most markets, prime rental values never decreased during the pandemic and many of them are even higher than their pre-crisis level. The offer is struggling to match the demand and the very low availability of prime assets and the appeal of high quality buildings located in the most sought-after districts drove the values up.

The most significant increases in rental values were in Luxembourg (+10%) and Berlin (+8%). Next there are Central London and Warsaw (+4%), Central Paris (+3%), Amsterdam, Milan and Brussels (+2% each).

A 10% increase in investments made in the office market compared to 2020

Investment levels were restored in 2021 and are back to pre-Covid-19 levels, with €272.7 billion invested in Europe across all asset classes over the year, which represents a 15% increase from 2020. This improvement was seen in European countries as they gradually took control of the Covid-19 outbreak, mainly through vaccination and the decrease of the virus transmission over the summer. On the other hand, with the reopening of the markets after 2020, most European cities are now back to prime office yield compression, with the exception of Paris, Amsterdam and Dublin where yields remained stable and Warsaw where it is expanding.

“Most countries benefited from this recovery in the market, with the UK, Germany, Spain and the Nordics; whereas other countries such as France, Belgium or The Netherlands are still below the 2020 investment levels. Offices are still the most popular asset class amongst investors, especially in France and Germany. With €106 billion invested in 2021, an increase of +10% compared to 2020, investment in the office market is on the road to recovery after the pandemic,” comments Larry Young, Head of International Investment Group at BNP Paribas Real Estate.

- Amira TAHIROVIC