“Q3 was encouraging for European offices. Yet although demand is growing for the best locations, increasing the pressure on rents and yields, the market is still waiting for a real recovery. There could be an improvement in 2026 if the economic and financial situation becomes clearer. Meanwhile, investment has started to rise again,” observes Etienne Prongué, Head of International Investment Group de BNP Paribas Real Estate.

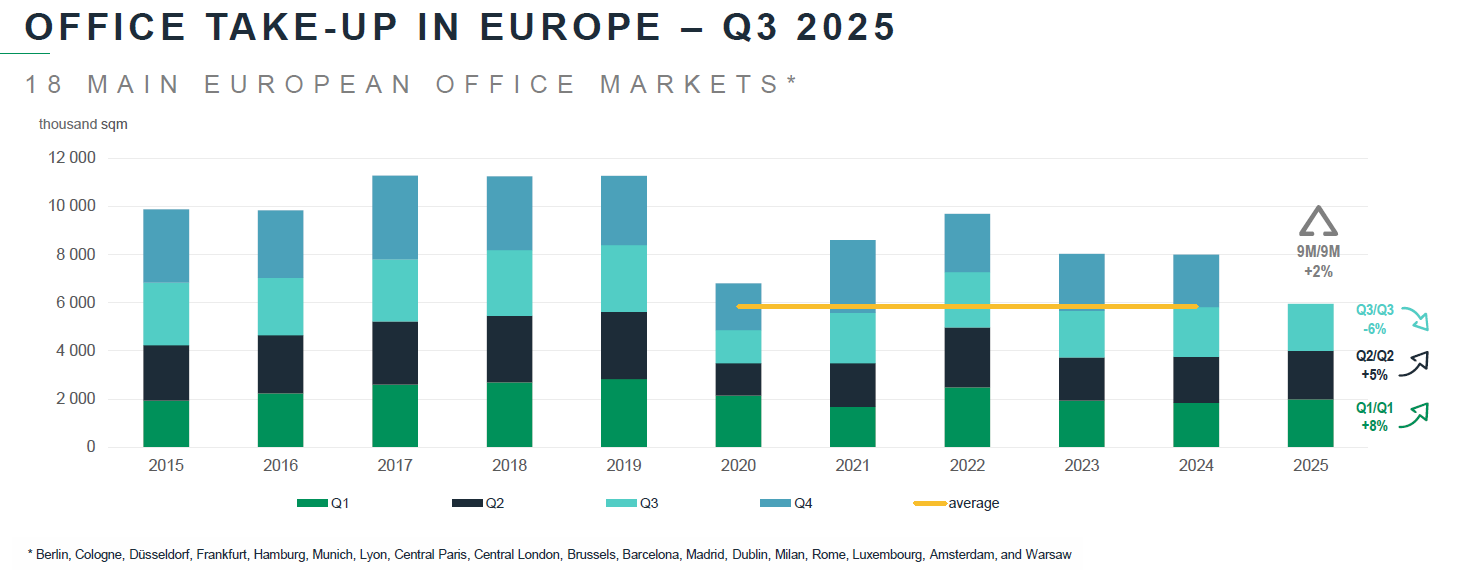

Take-up struggling to make a convincing recovery

After two very encouraging quarters, momentum faltered in Q3. With growth of just 2% and take-up in line with its 5-year average, there were mixed trends in the third quarter. Some more resilient markets are still attracting occupiers, such as Frankfurt and London. Total take-up in Q3 2025 was 5.95 million sqm across the 18 leading European markets*.

Certain cities stand out, such as Frankfurt, which hit a 20-year high (+63% vs Q3 2024), with an upturn in large-scale transactions by occupiers mainly from the financial/banking sector, such as Commerzbank (73,000 sqm in Q1), KPMG (33,400 sqm in Q2) and ING-DiBa (32,400 sqm in Q1). London also enjoyed a positive trend (+24% vs Q3 2024), driven by renewed confidence in several key sectors, although most deals were in the small to medium segment. Take-up in Barcelona (+18% vs Q3 2024) and Dublin (+14% vs Q3 2024) was also above the 5-year average.

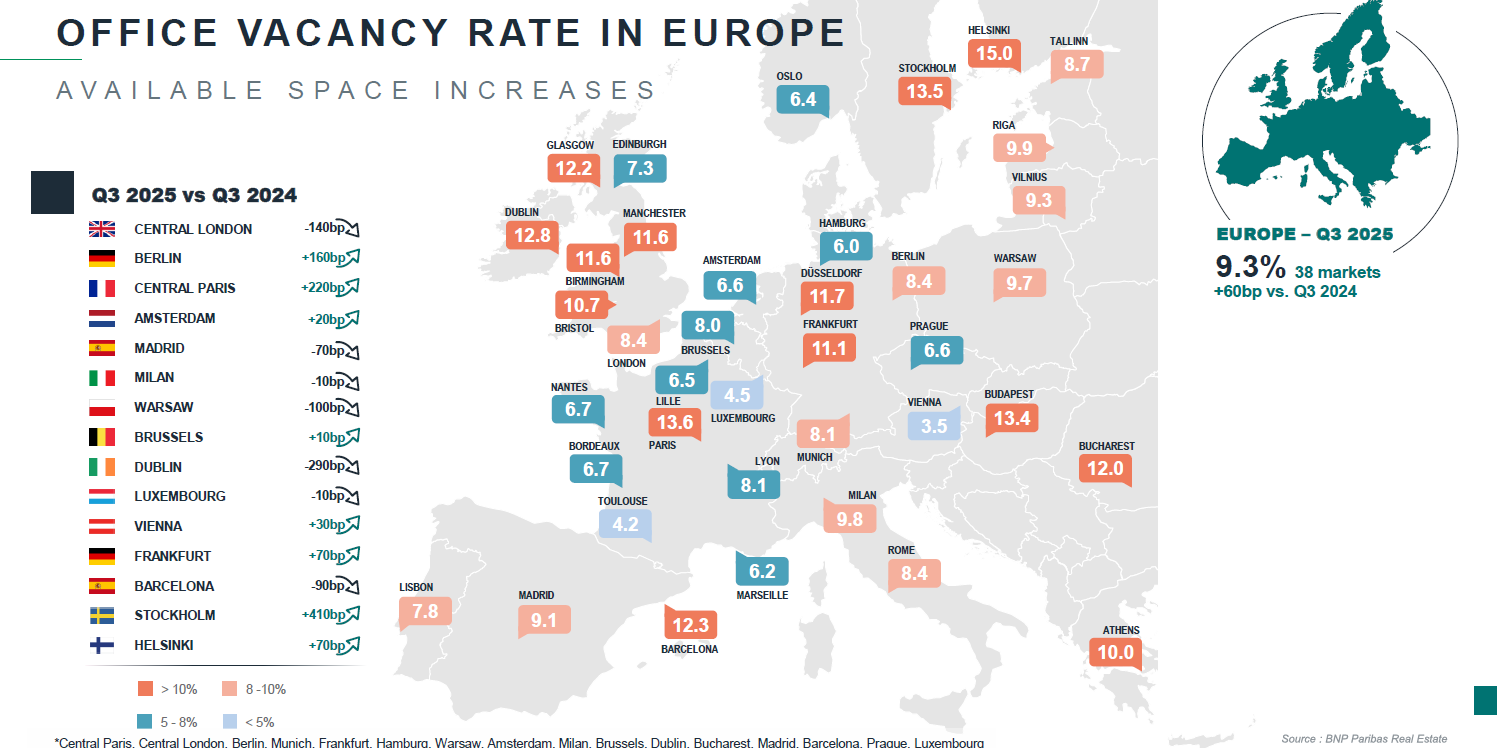

Vacancy: a growing gap between central and outlying markets

The average office vacancy rate in Europe stood at 9.3% at the end of September (+60bp compared to Q3 2024). Despite the widespread increase due to a growing mismatch between supply and demand, situations vary greatly across locations: supply is limited in central districts, particularly for modern buildings, whereas the vacancy rate has risen substantially in outlying districts and for second-hand assets.

This gap has been widening since 2022. The average vacancy rate in the CBDs stood at 5.4% at the end of September, up +20 basis points over the same period, vs. 10.9% in secondary markets (+80bp). The biggest disparities are in Barcelona, Paris and Brussels: in Barcelona, the vacancy rate in the CBD is 2.1%, while it is almost 14% in secondary neighbourhoods. The variations are smaller in German markets, where availability is more consistent across sub-markets.

With construction slowed by economic uncertainty and rising vacancy rates, completions are expected to fall in the coming months. This should allow some of the supply to be absorbed, especially if it meets occupiers' requirements in terms of location, quality and price.

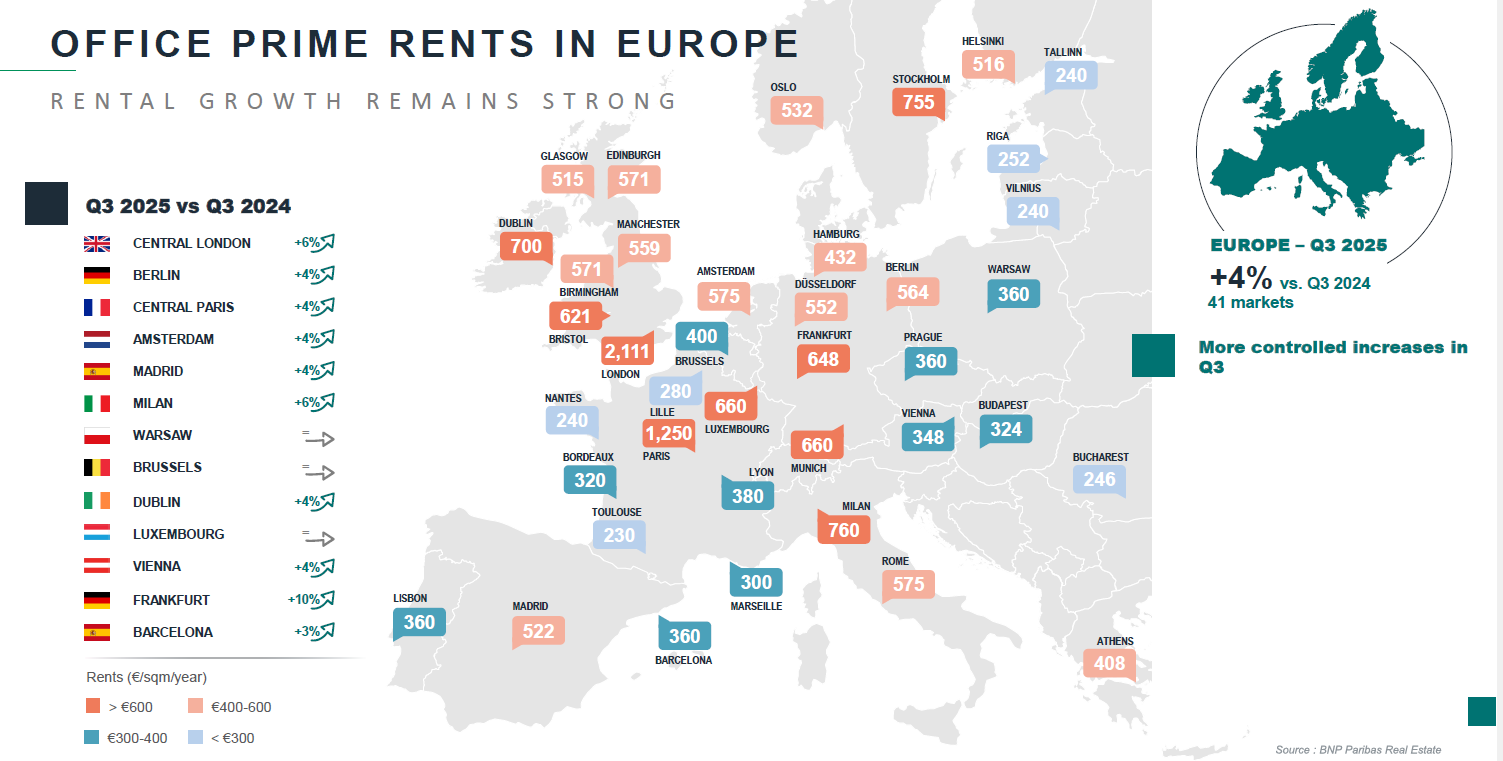

Widespread increases in prime rents

Occupier demand for central, high-quality assets is still pushing up prime rents in most European cities. Tight supply is exacerbating the trend.

The biggest year-on-year increases have been in Frankfurt (+10%), Milan (-6%) and Central London (+6%). For the first time, rent for an office in London topped € 2,000 /sqm. On average, prime rents increased by +4.1% compared to Q3 2024 (across some forty markets in Europe).

“The office market is becoming more segmented according to the age and quality of the stock. And a growing number of companies – particularly in banking, telecoms, automotive and aerospace – are requiring staff to come into the office more, supporting demand for prime locations”, remarks Etienne Prongué.

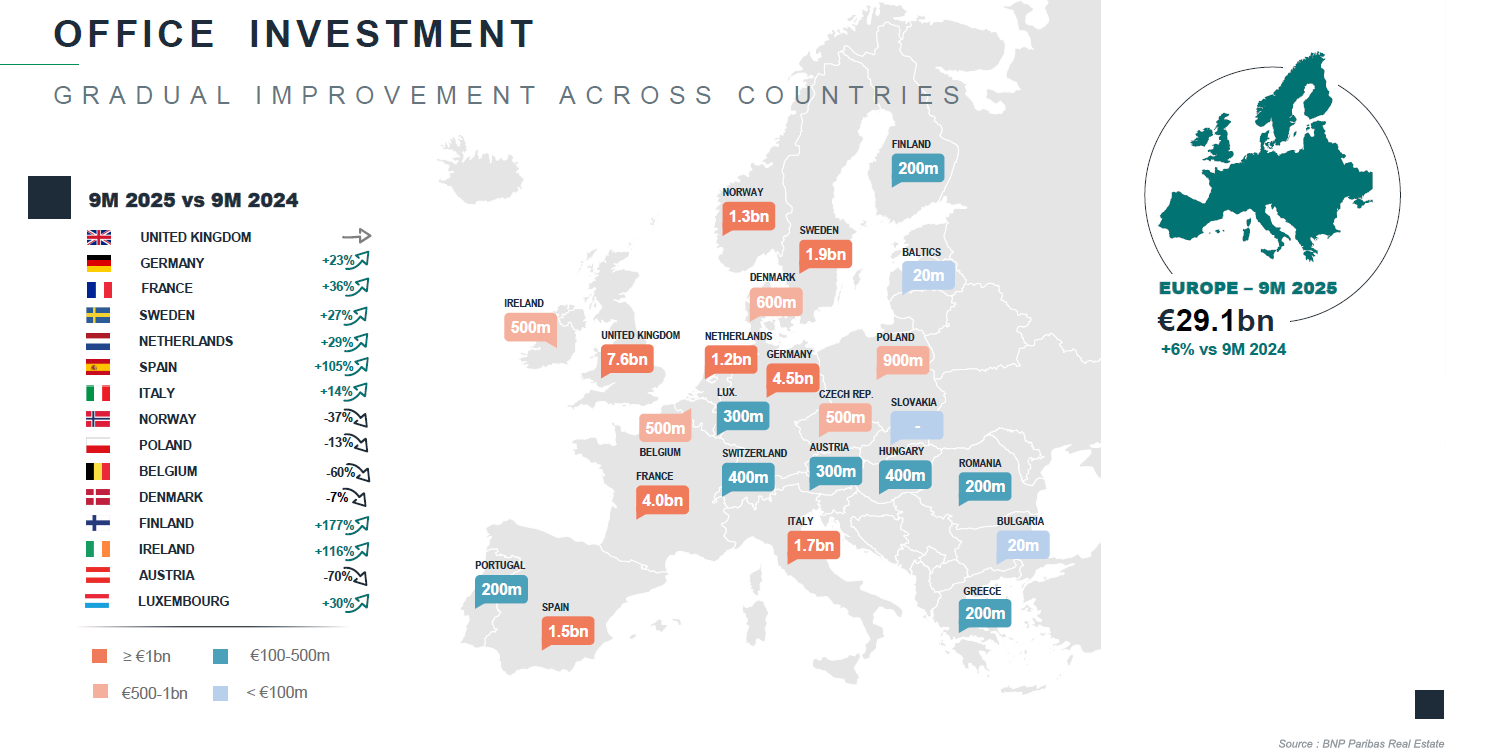

Investment on the rise again

Investment in European commercial real estate over the first nine months of 2025 came in at € 113.2bn, up 5% compared to the same period of last year. Growth over 12 rolling months was +19% to € 167.8bn.

Investment in the office segment continues to rise as investors gradually regain confidence. The sector has shown encouraging growth of 6% since the beginning of 2025, up to around € 30bn, underpinned by major deals in key markets, particularly in the UK, France and Germany (the “Upper West” building in southeast Berlin in Q1, the Deutsche Bank HQ in London in Q1 and the Solstys building in Paris CBD in Q3).

Where there has been growth, it is often double-digit: investment in France, the United Kingdom and Germany grew by around 13%, totalling € 16bn. It jumped 105% in Spain to € 1.7bn, back in line with its five-year average. There was also strong growth in the Netherlands (+29%) and Italy (+14%), with each attracting over € 1bn.

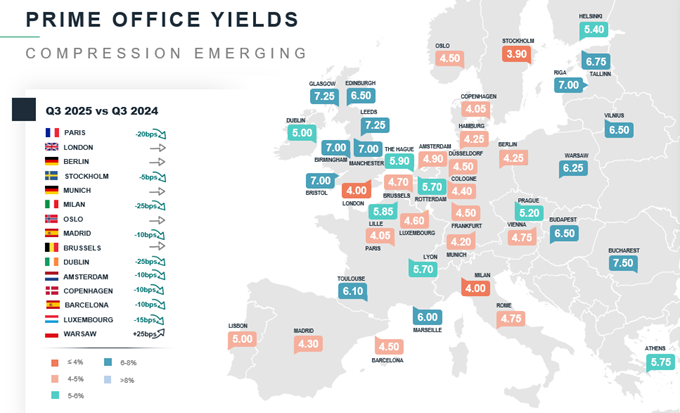

Prime office yields levelling off

With inflation now having stabilised at just over 2% (2.1% in the eurozone at the end of October) and economic prospects generally brightening, albeit still uncertain, the European Central Bank appears to have completed its monetary easing cycle. The deposit rate has been reduced from 3.75% to 2% since June 2024, bringing an end to the repricing phase that so deeply affected real estate markets from mid-2022.

For office markets in general, prime yields have been gradually falling for the past year. However, local trends still vary. Offices in the most central districts have seen their values stabilise over the past several months, while the capital value of those in secondary areas continues to adjust.

“The first signs of yields narrowing since late 2024 were confirmed in Q3 2025, with prime yields in Paris, London and Milan now at lows of around 4%. This trend confirms the growing selectiveness of investors, who prefer premium assets in more liquid and dynamic markets," concludes Etienne Prongué.

- Amira TAHIROVIC / Nolwenn CHAMPAULT