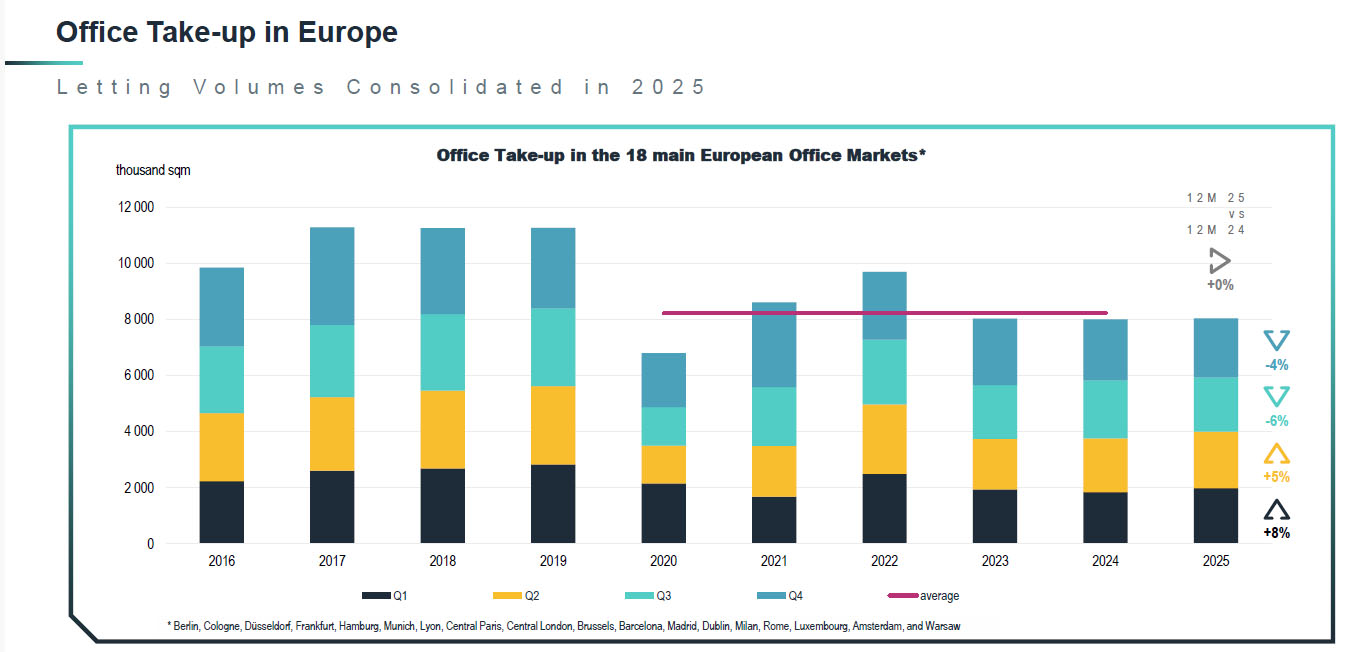

Take-up of European offices in 2025 was stable overall, in line with 2023 and 2024, providing further evidence that the five-year average is the new post-pandemic benchmark. Market momentum remains driven by central locations and high-quality assets, while polarisation continues to intensify across both occupier and investment markets, with the latter showing a clear rebound. As interest rates stabilise, the resumption of major deals suggests that investor confidence in Europe’s main markets is gradually being restored.

Stable take-up in 2025, in line with 2023 and 2024

After a promising H1, lettings in Europe slowed in H2 2025, with a -6% decline in Q3 followed by -4% in Q4. Total take-up for 2025 exceeded 8 million sqm across the 18 leading European markets*.

“This result is broadly in line with the previous two years and close to the five-year average, which is now emerging as the new post-pandemic benchmark. Activity remains strong in central business districts, while secondary locations are facing mounting challenges”, says Etienne Prongue, Head of International Investment Group (IIG) de BNP Paribas Real Estate.

Some markets performed well in 2025, starting with Frankfurt, where take-up surged by +54% year-on-year to 611,000 sqm — its highest level since 2019 and 31% above its five-year average. This outstanding performance was driven by exceptional transactions, particularly in the financial and banking sectors, including Commerzbank (73,000 sqm in Q1), KPMG (33,400 sqm in Q2) and ING-DiBa (32,400 sqm in Q1).

London also enjoyed significant growth (up +11% vs 2024), underpinned by lively submarkets such as King’s Cross (+35%) and Southbank (+16%). Luxembourg and Dublin, typically more volatile due to their smaller size, also performed well in 2025, posting increases of +34% and +14% respectively.

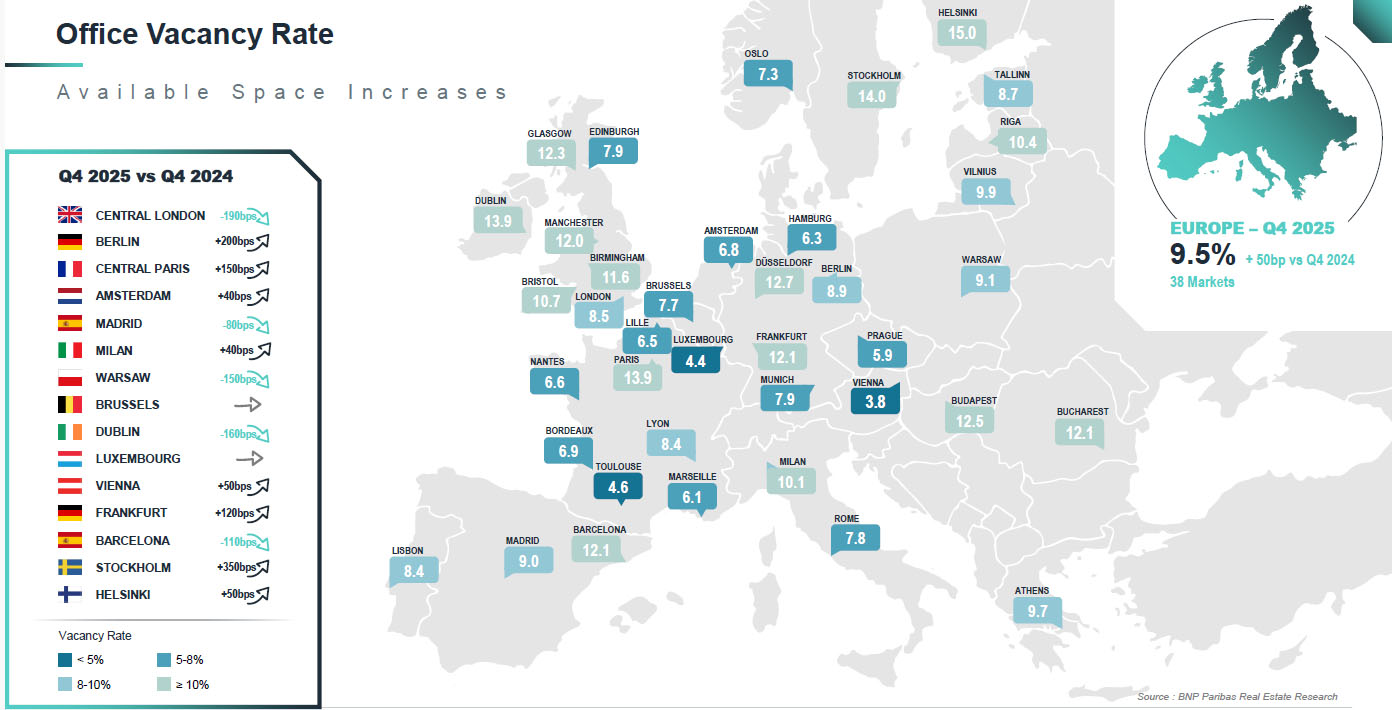

Growing supply with strong disparities between locations

The overall vacancy rate in Europe stood at 9.5% at the end of 2025, up 50 basis points year-on-year. Although vacancy has risen generally due to a growing mismatch between supply and demand, the trends vary greatly depending on location. Central districts still have limited availability, particularly for recently completed buildings, while vacancy rates are rising sharply in outlying districts and for second-hand assets.

The average CBD vacancy rate stood at 5.6% at end 2025, compared with 11.1% in secondary markets. This gap, which has been widening since 2020, highlights the growing dichotomy within the market. The most pronounced disparities are in Barcelona, Paris and Brussels. In Barcelona, for instance, the vacancy rate in the CBD stands at 1.6%, compared with over 12% in secondary districts.

“Hybrid working patterns and the renewed emphasis on meeting with colleagues in the office continue to drive occupier demand for buildings located in established central districts. Accessibility remains just as important as building quality. While modern space is available outside city centres, it is often less well connected,” explains Etienne Prongue.

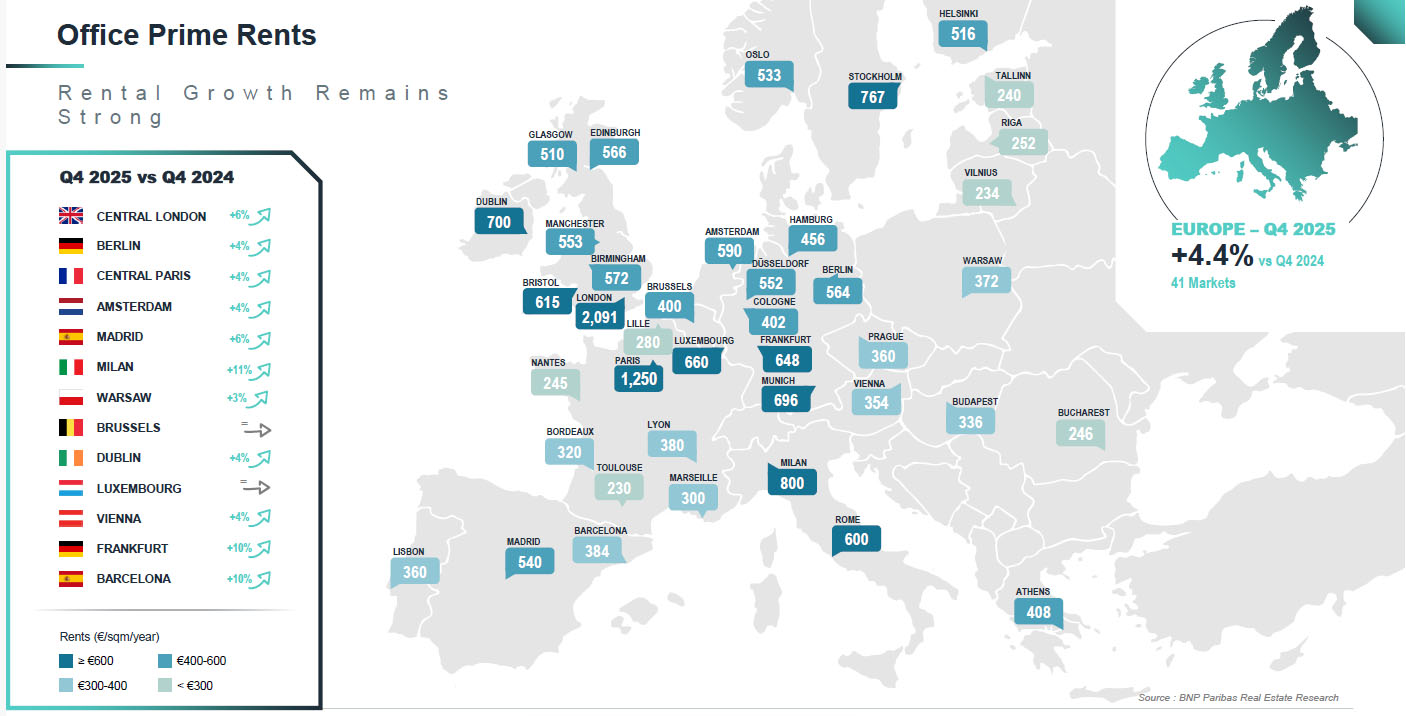

Prime rents continue to rise

Prime office rents continued to rise in most European cities, supported by the ongoing shortage of new high-quality space.

Southern European markets stood out in particular, with strong rental growth in Milan (+11%), Barcelona (+10%), Madrid (+6%) and Rome (+4%). On average, prime rents increased by +4.4% in 2025 across around forty European markets.

“Despite this continued upward trend, occupiers’ real estate strategies are increasingly geared to attracting talent and keeping it, rather than solely minimising occupancy costs. The scarcity of modern buildings in central locations is prompting some occupiers to consider more affordable outlying districts when rental discounts compared with CBDs are significant, provided accessibility and quality criteria are met,” adds Etienne Prongue.

Investment regaining momentum

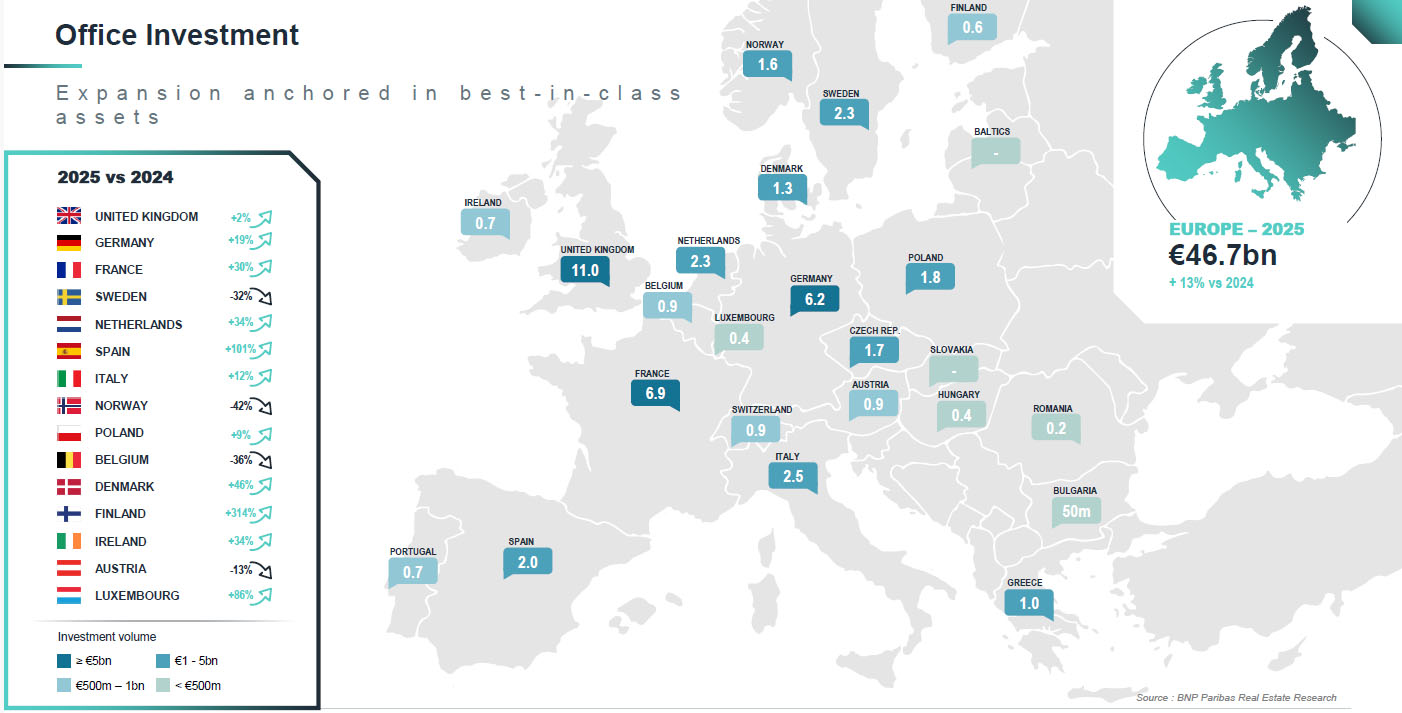

In 2025, commercial real estate confirmed its recovery, with nearly € 177bn invested, up +9% compared with 2024. This growth reflects the return of investors to more targeted and selective strategies.

“The office market harnessed this return to emerge as the best-performing asset class of the year. Spurred by improved visibility and continued demand for high-quality assets, office investment rose by +13% year-on-year, reaching € 47bn in 2025. This momentum was underpinned by the return of large-scale transactions in Europe’s main capital cities,” specifies Etienne Prongue.

A highlight in Q4 was the sale of the landmark “Can of Ham” tower (30,000 sqm) in London, as well as the sale of a 40,000 sqm building on Avenue Kléber in Paris for more than € 700m.

The recovery was observed across Europe. France and Germany posted strong growth of +30% and +19% respectively, while the UK continued to stabilise (+2%). Spain stood out with a sharp acceleration, as investment doubled year-on-year to € 2bn. The Netherlands (+34%) and Italy (+12%) also confirmed this upward trend, reflecting a more favourable investment climate and a measure of restored confidence in the office segment.

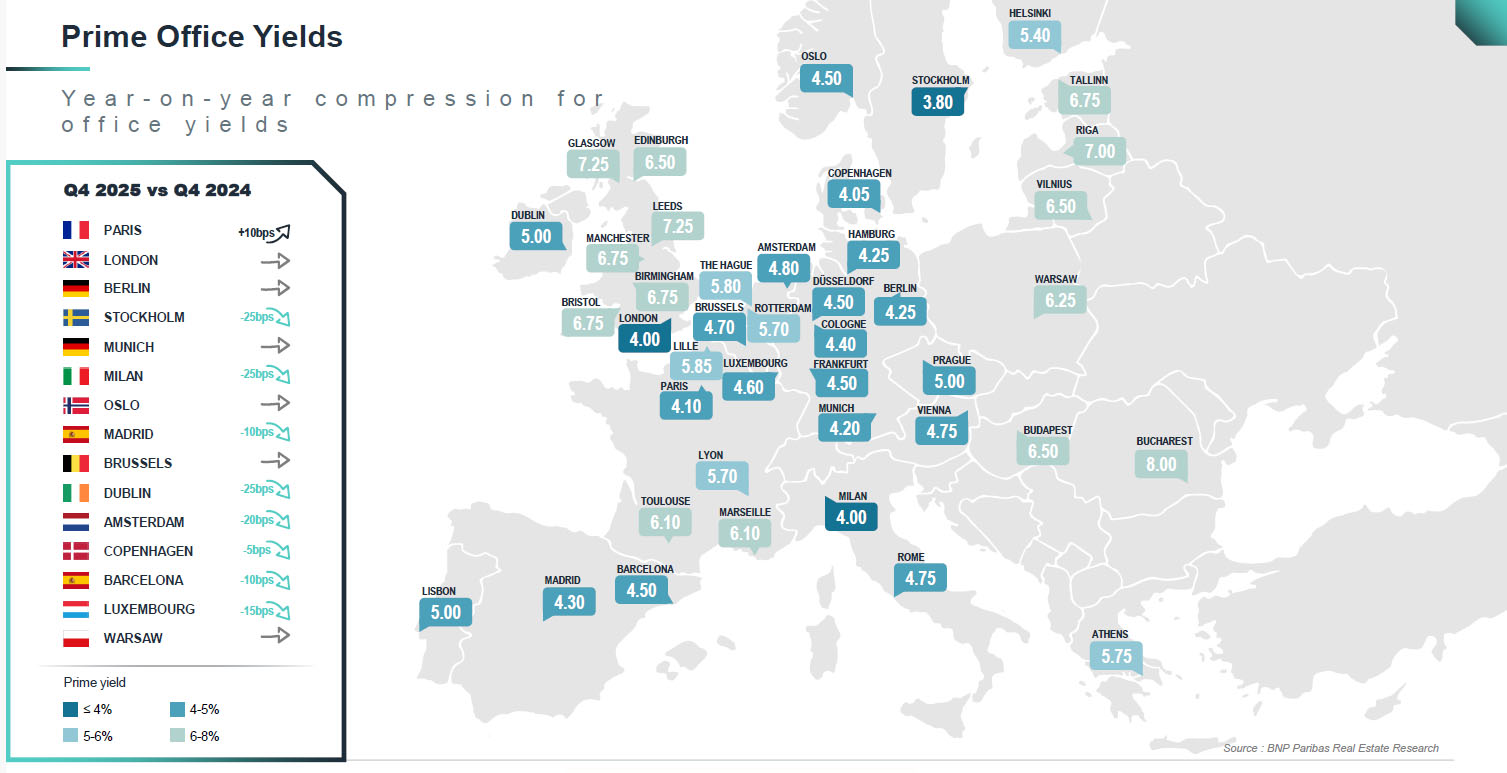

Prime yields stabilise, with contraction expected

The narrowing of yields that began at the end of 2024 continued unevenly across cities, resulting in overall stability in H2 2025 at the European level. This stabilisation comes amid improved visibility for investors, with inflation under control at around 2%. While the European Central Bank has stabilised its key rate, further monetary easing by the Bank of England is expected to improve borrowing conditions and facilitate deal completion.

Recent quarters have confirmed the ongoing polarisation in the office market. In the most sought-after districts of the major cities, capital values remain stable, while prices for secondary assets continue to adjust, illustrating the persistent divergence in local trends.

“As seen in London and Paris, investor appetite is clearly returning to Europe’s major cities, supported by improving liquidity conditions. We expect a more pronounced recovery in transactions in the first half of 2026 in the UK, France and Germany. Strong demand for core assets should continue to exert downward pressure on prime yields,” concludes Etienne Prongue.