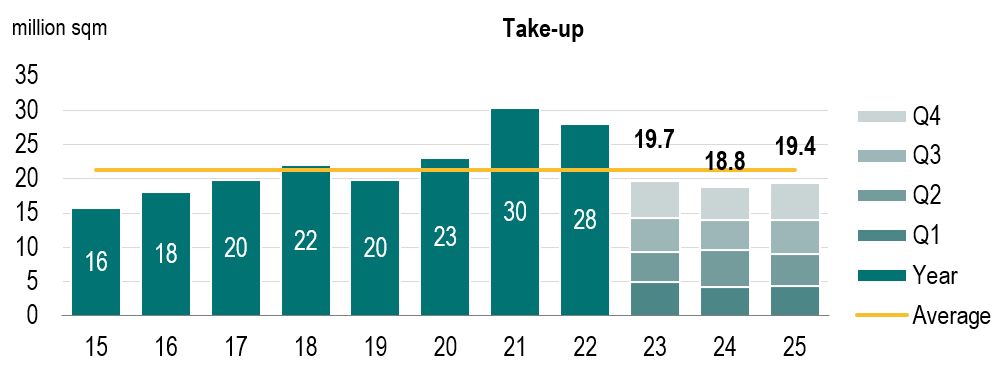

Occupier markets remain resilient despite a challenging context

The year 2025 was mixed, with highly contrasting situations from one country to another. Economic conditions and geopolitical uncertainties prompted companies to postpone their real estate plans in a number of European markets.

“Nevertheless, several structural trends clearly emerged at the European level, including the return of large transactions, with a marked increase in deals ranging from 20,000 to 40,000 sqm. We also observe strong disparities in vacancy rates, ranging from 2% to 11% depending on the region. As for rents, they continue to rise, fuelled by limited availability in highly constrained markets such as Barcelona, Milan and Prague,” explains Craig Maguire, Head of European Logistics at BNP Paribas Real Estate.

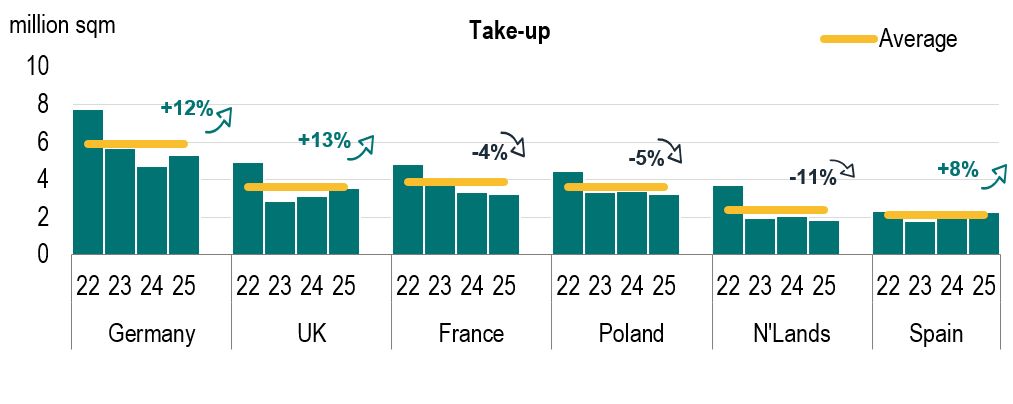

Behind this resilience, significant contrasts persist, directly linked to local market fundamentals:

- United Kingdom: particularly strong activity in the Midlands (Birmingham), accounting for 40% of all transactions, with robust demand from healthcare and defence sectors.

- Germany: transactions above 20,000 sqm increased by +30%, mainly driven by logistics providers working for e-commerce players.

- France: activity declined by –4%, impacted by economic and political uncertainties.

- Spain: supported by +2.9% GDP growth in 2025, the market was close to its record 2022 level.

- Netherlands: overall decline in volumes due to land scarcity and administrative constraints; for the first time, second-hand supply exceeded new-build stock.

- Poland: after a low start to the year, take-up rose steadily in H2 and the vacancy rate decreased slightly to 7.4% in Q4 2025.

At the European level, the largest transactions were recorded in France and the United Kingdom (all above 100,000 sqm), including two Amazon deals (Chartres and Beauvais) and a 120,000 sqm scheme for Marks & Spencer in northern England.

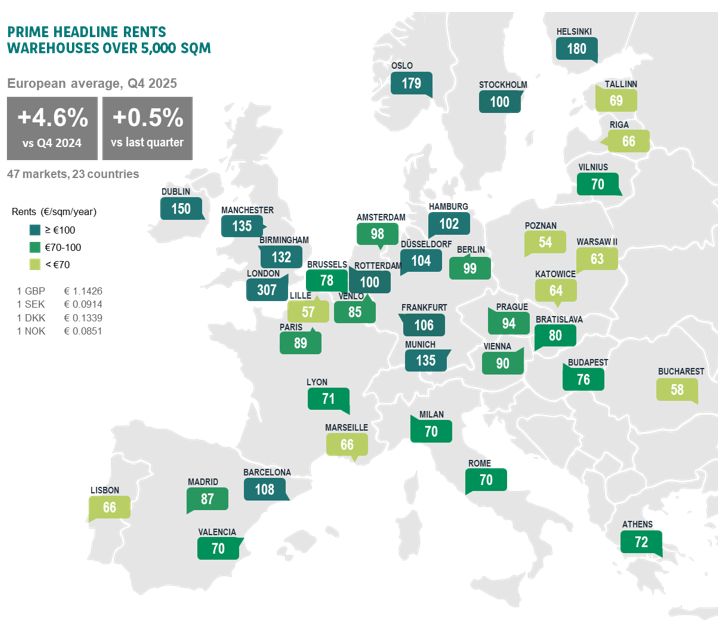

Rental market recovery: prime rents continue to rise

In 2025, logistics rents increased by 4.5% on average across Europe. This sustained growth is driven by:

- Limited land availability,

- A very low level of speculative developments,

- Rising construction costs and the overall upgrading of warehouse specifications.

This upward trend is expected to continue in 2026, although at a more moderate pace than in recent years.

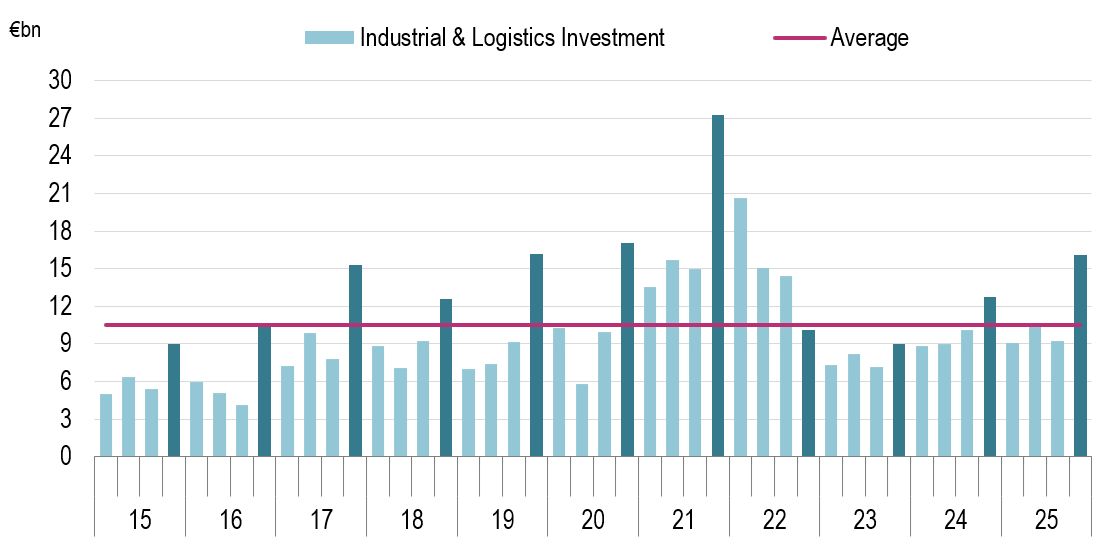

Investment market: a confirmed recovery

With nearly €45bn invested in 2025, the industrial and logistics investment market has returned to pre-crisis levels, supported by an average +11% growth across Europe.

“This recovery is underpinned by a more stable financial environment, better-controlled inflation and renewed investor interest in logistics assets, which now account for one quarter of total European real estate investment, on par with office assets. However, performance remains uneven across the continent, with significant disparities between markets,”

notes Craig Maguire.

As a result, the German and UK markets account for nearly 50% of the total investment volumes. The latter, which has been particularly dynamic, represents one third of all European investments on its own. Along with Sweden, these two markets benefited from large portfolio disposals that boosted volumes. In Germany, activity was more measured over the year, although the second half recorded a notable acceleration, particularly driven by portfolio sales. In Spain, a solid macroeconomic environment continues to support market activity.

Return of large-deals and pan-European joint ventures

2025 was characterised by the return of large-scale transactions in the European logistics investment market. Among the most notable deals:

- LondonMetric acquired Urban Logistics’ UK portfolio for €1.4bn.

- Tritax Big Box purchased an industrial portfolio from Blackstone worth €1.2bn.

- Segro acquired a 370,000 sqm portfolio from Tritax Eurobox, located in Germany and the Netherlands.

Several pan-European joint ventures also contributed to market momentum, reflecting growing international investor appetite - including the partnership between AustralianSuper and Oxford Properties, as well as the joint venture between AREIM and VGP.

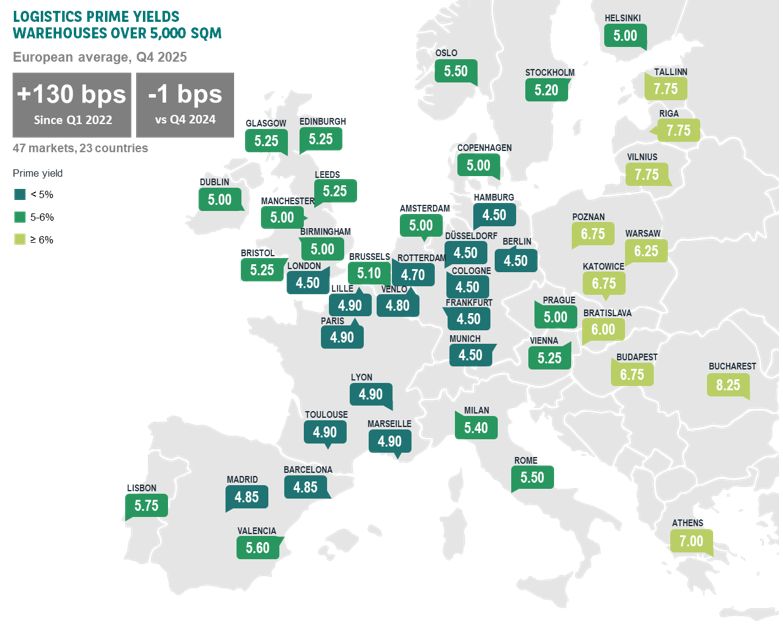

Prime yields expected to stabilise in 2026

In 2025, prime logistics yields tightened across major European economies, ranging between 4.5% in Germany and 5.4% in Italy. Higher-than-expected long-term interest rates led to a slight increase in yields in both France and Germany toward the end of the year.

“Looking ahead to 2026, we expect a period of stabilisation, with steady yields and a moderate increase in capital values, underpinned by continued rental growth,” concludes Craig Maguire.

*France, Poland, Germany, Netherlands, Spain, United Kingdom