Investment market: retail real estate demonstrates resilience

Over the past 12 months, commercial real estate investment in Europe has increased by 10%, despite a more subdued first quarter (-7% compared to Q1 2025). In this context, the retail sector shows a stabilisation in invested volumes year-on-year, while the hotel sector recorded a slight decline of 2% in commitments. Office and logistics stood out with growth of 11% and 7% respectively over the last 12 months.

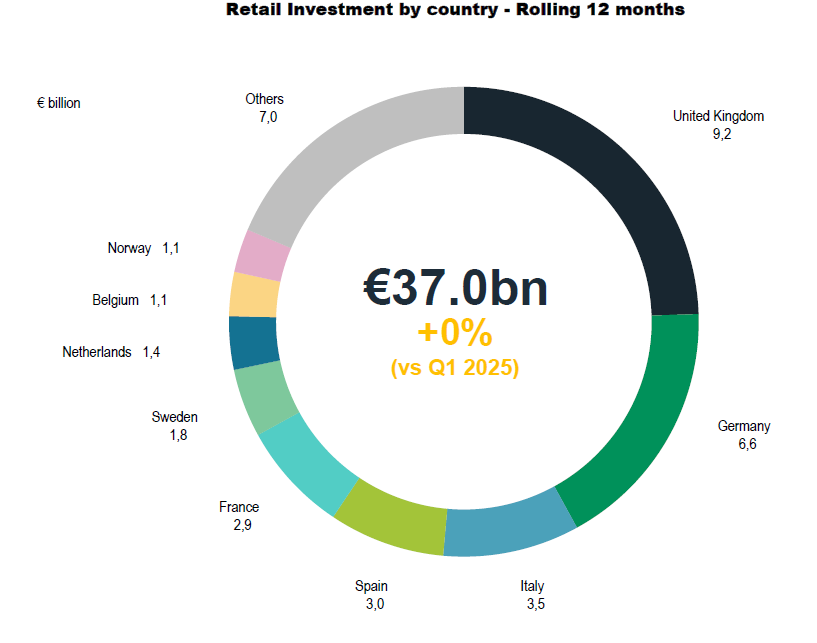

Retail remains the third-largest sector by investment share in commercial real estate, with €37 billion in Q1 2026, representing 20% of total volumes (compared to 15% in Q1 2022, the lowest point over the past 10 years). The sector ranks behind office (26%) and logistics (24%), while hotels account for 11% of invested volumes.

While the United Kingdom, Germany and France have historically attracted the majority of retail real estate investment in Europe, new dynamics have emerged over the past 12 months. Germany recorded a 17% rebound in investment volumes, while the United Kingdom saw a year-on-year decline of 16%, and France dropped by 30%. At the same time, Italy and Spain moved up the ranking, with investment volumes increasing by 11% and 43% respectively year-on-year, driven by strong interest in the shopping centre segment. Sweden (+75%), the Netherlands (+97%) and Belgium (+131%) also performed strongly, with sustained activity levels in recent quarters.

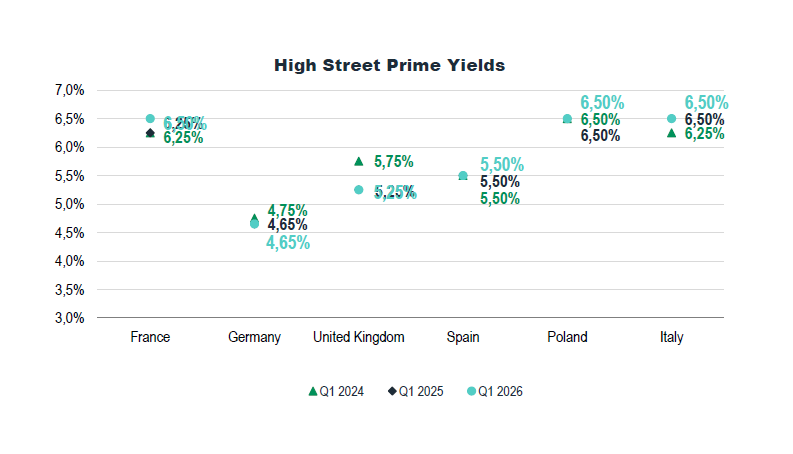

Across the various retail real estate segments, performance remains mixed, highlighting disparities between asset classes and an evolving market landscape. High street transactions declined significantly (-25%) compared to last year, with €7.5 billion invested across the main European countries*. This adjustment reflects the reality of a mature and increasingly polarised market, where yields remain compressed in prime locations.

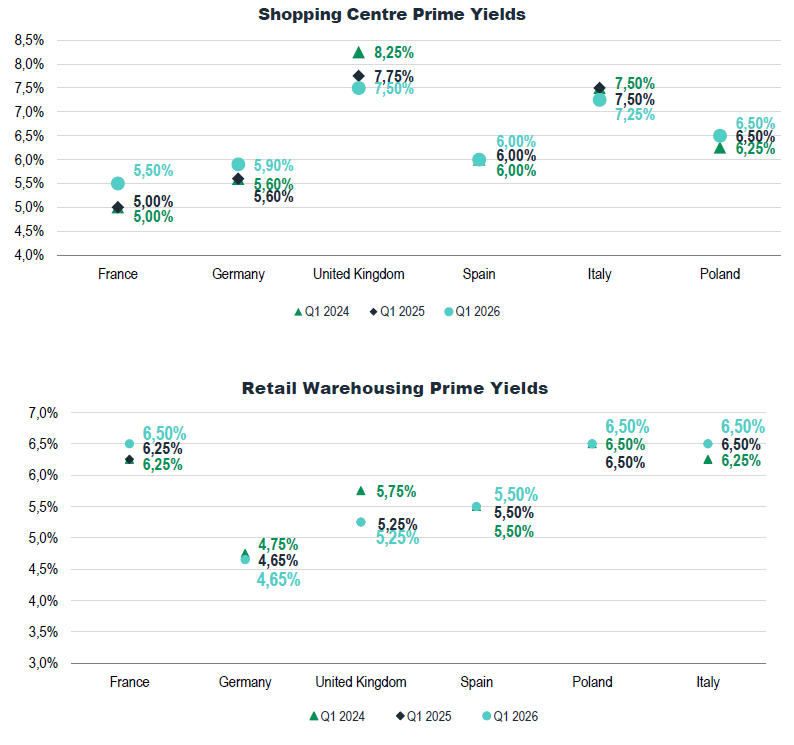

Across major European retail markets, shopping centres clearly stand out, recording strong growth (+26%) with €8.9 billion invested over the past twelve months, highlighting renewed investor interest in this asset class. This trend is driven by a higher risk premium compared to other retail segments, notably high street and out-of-town retail, as well as solid operational performance from shopping centre operators, both in terms of tenant turnover and rental growth. In an inflationary environment likely to weigh on real estate yields, the attractive yield levels offered by shopping centres should continue to support investor appetite for this asset class. Several significant shopping centre transactions were completed over the past 12 months, including Islazul in Madrid (€340 million), Palladium in Prague (€700 million) and Orio Center in Bergamo (€450 million).

Finally, out-of-town retail investment volumes across major European countries reached €9.7 billion over the past twelve months, representing the largest share of invested capital in European retail, despite a 9% year-on-year decline. This segment, characterised by low vacancy rates and continued retailer demand, offers investors stable rental income with a lower entry price.

An attractive risk premium for retail parks and shopping centres

“In a context of increasing selectivity, shopping centres and retail parks continue to offer investors a more attractive risk-return profile than other commercial real estate segments,” says Patrick Delcol, Head of European Retail at BNP Paribas Real Estate.

Initial yield decompression was observed in Q1 2026 following a prolonged period of stabilisation, particularly in the shopping centre segment in France (+50 bps) and Germany (+30 bps), while a 25 basis point compression was recorded in Italy and the United Kingdom. In Spain, the increase in shopping centre transactions in recent quarters suggests a positive outlook and potential yield compression. Out-of-town retail yields remained broadly stable in Q1 2026, with the exception of France (+25 bps).

In contrast, high street results remain mixed, with stable yields in Munich and Paris, and tightening observed in Madrid, London and Milan over three years, as the availability of prime assets in these locations remains scarce and difficult to access.

Measured outlook for retail investment

“Despite increasing uncertainty linked to the economic and geopolitical environment, the European retail sector continues to benefit from solid fundamentals that should support resilient investment levels in 2026,” according to Patrick Delcol.

Several sector indicators point to a positive perception of the retail segment. According to Eurostat, consumer confidence improved at the start of the year compared with levels recorded in Q4 2025, reflecting more favourable household expectations regarding their future financial situation. Retail sales saw a slight decline at the beginning of the year, but the decrease remains limited and does not signal a break in trend.

Furthermore, gradual market improvement is also reflected in the narrowing gap between sellers’ expectations and buyers’ pricing, indicating better alignment of market perceptions. This normalisation remains fragile, particularly in the United Kingdom, where inflation outlooks remain more sensitive. At the European level, the ongoing conflict in the Middle East also represents a risk factor, potentially impacting supply chains and procurement costs before indirectly affecting retail activity.

*The six main European markets: Germany, Spain, France, Italy, Poland and the United Kingdom