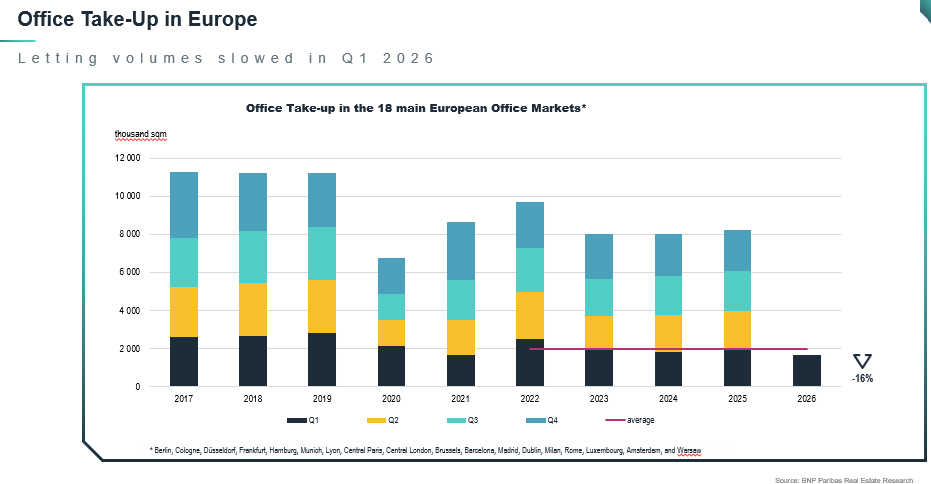

Leasing activity slows in Q1 2026

In the first quarter of 2026, leasing activity across Europe declined by 16%. Total take-up reached 1.67 million sqm across the 18 main European markets*, significantly below the five-year average (-16%). This contraction is primarily due to a drop in transactions above 5,000 sqm across many markets.

In an uncertain economic and financial environment, occupiers are taking a more cautious stance, with a growing preference for smaller spaces and higher-quality buildings.

Take-up declined in Paris and London (-23% and -15% respectively). The six main German markets followed a similar trend, with an overall decrease of 12%, although performances vary between cities. Munich stood out, with take-up reaching 172,000 sqm in Q1 (+26% year-on-year), its highest quarterly level since 2022, supported by three transactions above 20,000 sqm. Berlin also performed strongly, with 146,000 sqm transacted, up 42% year-on-year.

Elsewhere in Europe, trends remained mixed: Milan and Madrid recorded significant declines (-36% and -25%), while Barcelona (+34%), Dublin (+21%), Rome (+11%) and Brussels (+11%) posted growth, highlighting a heterogeneous recovery across markets.

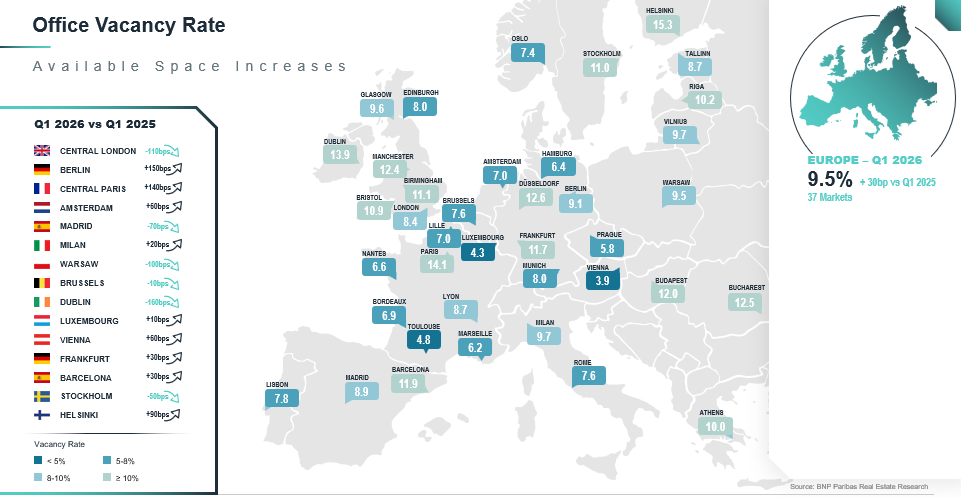

Rising supply further reinforces market polarization

Office supply continued to increase across Europe, albeit unevenly. At the end of March 2026, the average vacancy rate reached 9.5%, up 30 basis points year-on-year, despite limited new deliveries.

This trend reflects a growing imbalance between supply and demand and masks significant disparities between locations. Central business districts (CBDs) continue to benefit from constrained supply, particularly for modern, high-quality buildings, while vacancy rates are rising more sharply in peripheral areas and in older stock.

Average vacancy rates stand at 5.6% in CBDs, compared with 11.2% in secondary markets. This widening gap highlights increasing market polarisation and confirms occupiers’ preference for central locations offering strong transport accessibility.

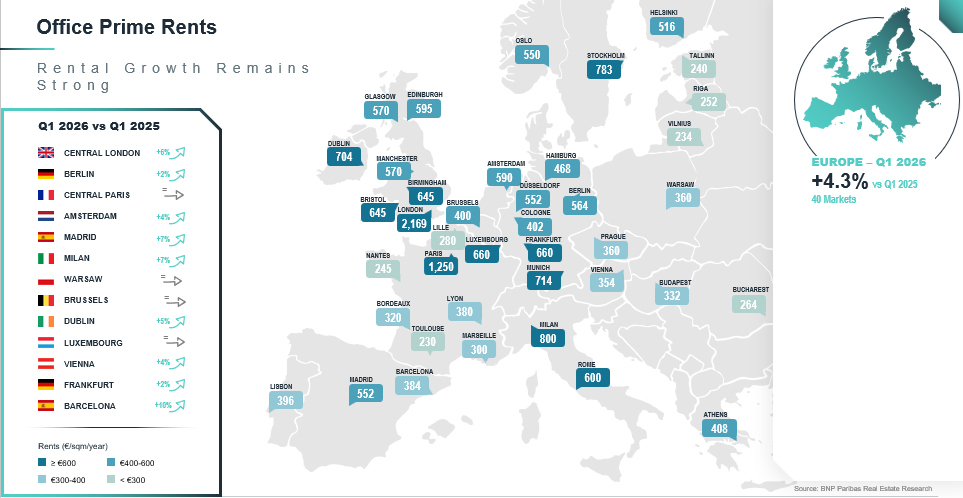

Prime rents continue to rise, but momentum may moderate

Prime office rents continued to increase in most major European cities, supported by the limited availability of new space in central locations.

Southern European markets stand out, with significant increases in Barcelona (+10%), Madrid and Milan (+7%), and Rome (+4.5%). Over a 12-month period, London also recorded a notable increase (+6%).

However, Q1 2026 data suggests that rental growth may start to slow in several markets. Faced with high rental levels, some occupiers are increasingly considering secondary locations, provided they offer both accessibility and quality, which could help ease pressure on prime rents.

Investors adopt a wait-and-see approach amid uncertainty

In a context of renewed macroeconomic uncertainty (particularly regarding energy markets) inflationary pressures may re-emerge, while growth prospects in Europe are being revised downward. Against this backdrop, the real estate market remains resilient but has entered a phase of cautious observation.

While investors are adopting a more selective approach in the short term, market fundamentals remain solid, and demand for high-quality assets continues to support activity.

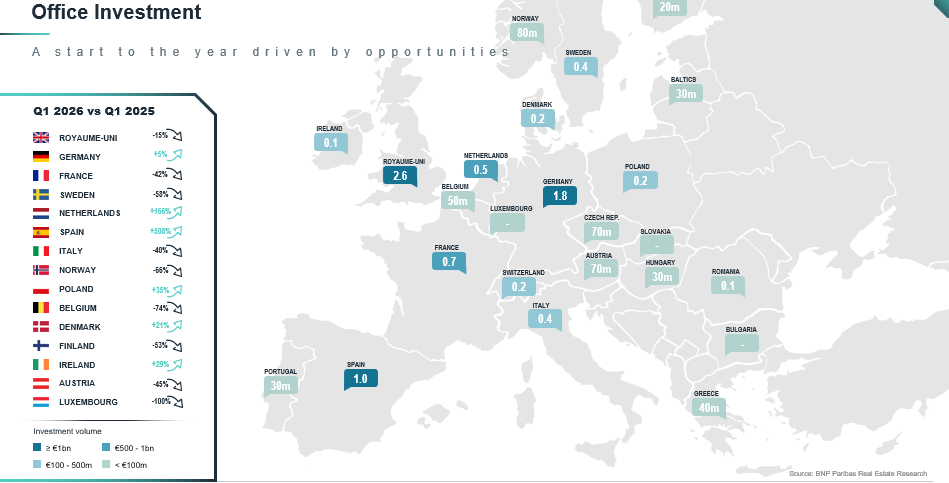

In Q1 2026, more than €36 billion was invested across Europe, representing a limited decrease of 7% year-on-year. On a rolling 12-month basis, volumes are up by 10%, in line with the momentum observed at the end of 2025. The slowdown at the start of the year reflects a pause rather than a market downturn.

The office sector mirrors this trend, with investment volumes declining by 13% to approximately €9 billion. This moderation reflects both a return to more normal activity levels after a strong end to 2025 and varied trends across markets. Cities such as Amsterdam and Madrid have shown relative resilience, maintaining solid levels of activity.

Contrasting dynamics across European markets

Market performances vary significantly across countries:

- France recorded a sharp decline (-42%) following a strong 2025, although Paris remains highly attractive and continues to concentrate most transactions.

- The UK saw a more moderate correction (-15%), with London maintaining its position as Europe’s leading investment market.

- Germany stood out positively, with investment volumes rising by 5%, supported by a more favourable market sentiment.

Peripheral markets gained momentum: the Netherlands (+166%) and Spain (more than €1 billion invested, fivefold increase year-on-year) illustrate the strong return of investors, while Ireland confirmed its recovery.

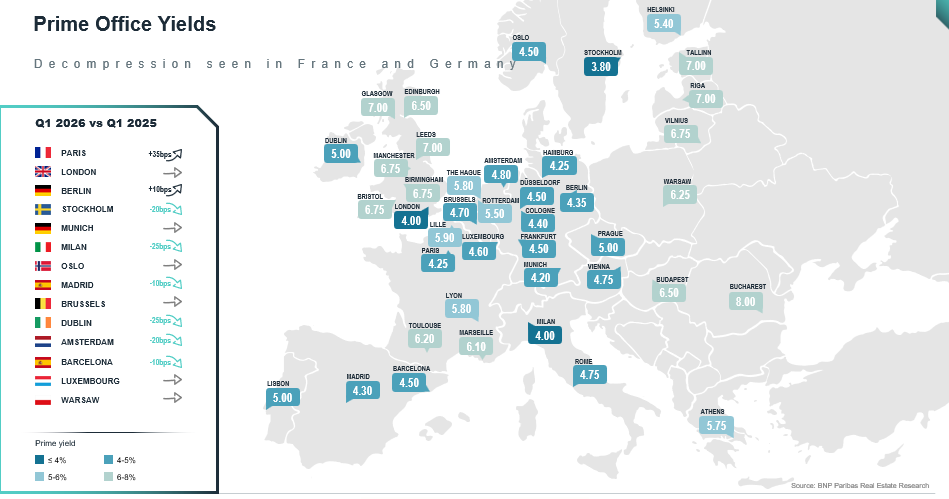

Yield adjustments remain limited despite financial uncertainty

Central banks are operating in an increasingly uncertain environment, with renewed inflationary pressures linked to geopolitical tensions, raising the prospect of further interest rate hikes.

In this context, real estate yields have remained broadly stable, although there are signs of slight upward pressure in some markets, notably in Paris (4.25%) and Berlin (4.35%).

“Markets have already largely priced in adjustments in valuations in a context of tighter financing conditions. While current uncertainties may still trigger temporary fluctuations in yields, these adjustments should remain limited in both scale and duration,” said Etienne Prongué, Head of International Investment Group (IIG) at BNP Paribas Real Estate.

At the same time, increased investor selectivity continues to shape the market, with a clear preference for core assets in the most liquid markets. Prime rental growth remains a supporting factor, helping to mitigate the impact of potential further yield adjustments.